Exhibit 1

Putting Shareholders First: The Case for a New Era at Mack-Cali May 2020

Exhibit 1

Putting Shareholders First: The Case for a New Era at Mack-Cali May 2020

Disclaimer This presentation and any of the information contained herein (this “Presentation”) is for discussion and general informational purposes only and is not complete. Under no circumstances is this Presentation intended to be, nor should it be construed as advice or a recommendation to enter into or conclude any transaction or buy or sell any security (whether on the terms shown herein or otherwise). This Presentation should not be construed as legal, tax, investment, financial or other advice. Additionally, this Presentation should not be construed as an offer to buy any investment in any fund managed by Bow Street LLC (“Bow Street”) or its affiliates. All investments involve risk, including the risk of total loss. This Presentation is not an advertisement. The purpose of this Presentation is to communicate Bow Street’s views regarding the companies discussed herein, including Mack-Cali Realty Corporation (“CLI” or the “Company”) . In making this Presentation available for distribution, Bow Street is not acting as an investment adviser with respect to any recipient of this Presentation. Any mention within this Presentation of Bow Street’s research process is incidental to the presentation of Bow Street’s views regarding the companies described herein. The views contained in this Presentation represent the opinions of Bow Street as of the date hereof. Bow Street reserves the right to change any of its opinions expressed herein at any time, but is under no obligation to update the data, information or opinions contained herein. The information contained in this Presentation may not contain all of the information required in order to evaluate the value of the companies discussed in this Presentation. The views expressed in this Presentation are based on publicly available information, including information derived or obtained from filings made with the Securities and Exchange Commission and other regulatory authorities and from third parties. Bow Street recognizes that there may be nonpublic or other information in the possession of the companies discussed herein that could lead these companies and others to disagree with Bow Street’s conclusions. Bow Street has not sought or obtained consent from any third party to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties. Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein. No agreement, arrangement, commitment or understanding exists or shall be deemed to exist between or among Bow Street and any third party or parties by virtue of furnishing this Presentation. None of Bow Street, its affiliates, its or their representatives, agents or associated companies or any other person makes any express or implied representation or warranty as to the reliability, accuracy or completeness of the information contained in this Presentation, or in any other written or oral communication transmitted or made available to the recipient. Bow Street, its affiliates and its and their representatives, agents and associated companies expressly disclaim any and all liability based, in whole or in part, on such information, errors therein or omissions therefrom. The analyses provided herein may include certain forward-looking statements, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the companies discussed in this Presentation, access to capital markets, market conditions and the values of assets and liabilities, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” “plan,” and similar expressions are generally intended to identify such forward-looking statements. Such statements, estimates, and projections reflect Bow Street’s various assumptions concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies. Thus, actual results may vary materially from the estimates and projected results contained herein. No representations, express or implied, are made as to the accuracy or completeness of such statements, estimates or projections or with respect to any other materials herein and Bow Street disclaims any liability with respect thereto. In addition, Bow Street will not undertake and specifically disclaims any obligation to disclose the results of any revisions that may be made to any projected results or forward-looking statements in this Presentation to reflect events or circumstances after the date of such projected results or statements or to reflect the occurrence of anticipated or unanticipated events. Clients and accounts managed by Bow Street (the “Bow Street Clients”) may beneficially own, and/or have an economic interest in, shares of certain of the companies discussed in this Presentation and as a result, Bow Street and its clients have an economic interest in the forward-looking statements, estimates and projections discussed above and their impact on the companies discussed in this Presentation. The Bow Street Clients are in the business of trading – buying and selling – securities, and may trade in the securities of the companies discussed in this Presentation. You should also assume that the Bow Street Clients may from time to time sell all or a portion of their holdings of one or more of the companies in open market transactions or otherwise (including via short sales), buy additional shares (in open market or privately negotiated transactions or otherwise), or trade in options, puts, calls, swaps or other derivative instruments relating to some or all of such shares, regardless of the views expressed in this Presentation. Bow Street reserves the right to change its intentions with respect to its investments in the companies discussed in this Presentation and take any actions with respect to investments in such companies as it may deem appropriate, and disclaims any obligation to notify the market or any other party of any such changes or actions. All registered or unregistered service marks, trademarks and trade names referred to in this Presentation are the property of their respective owners, and Bow Street’s use herein does not imply an affiliation with, or endorsement by, the owners of these service marks, trademarks and trade names.

A Message to Our Fellow Shareholders § We are once again seeking your support to make changes at Mack-Cali – the Company we collectively own. As shareholders, we have all endured many years of underperformance and disappointment § No matter what management or the Legacy Board members tell you, Mack-Cali’s current predicament was not inevitable; our Company is in a precarious state owing to incompetent management, poor strategic decision making, and a Legacy Board of Directors that has served itself over shareholders ,§ Throughout our ownership of Mack-Cali – particularly over the last twelve months – we have witnessed unconscionable and unprecedented violations of corporate governance: management and the Legacy Board of Directors cannot be trusted to protect and further shareholder interests § To be clear: given the current environment (and in direct contradiction to Mack-Cali’s assertions), we are not advocating for a sale of the Company; we are, however, advocating for an independent and high integrity Board of Directors § These are challenging times – a competent, trustworthy CEO overseen by independent fiduciaries with a clear, strong moral compass has never been more important § We are nominating four additional talented, trustworthy, shareholder-focused individuals to the Company’s Board, so that we can finally usher in a new era at Mack-Cali. These new Board members will be independent, representing all shareholders § If you would like to speak with us or any of these nominees with thoughts, suggestions, or questions, please contact us at CLIShareholders@bowstreetllc.com § We thank you for your trust and your support – The Bow Street Team

“When seeking directors, CEOs don’t look for pit bulls. It’s the cocker spaniel that gets taken home.” - Warren Buffett, 2020(1)

Table of Contents 1) Executive Summary 2) Are Shareholders Better Off Than They Were 5-Years Ago? A Clear-eyed Assessment of Management’s Tenure 3) A Legacy of Broken Corporate Governance 4) The Path Forward: Restoring Oversight and Accountability 5) Appendix: In Management’s Own Words – A Compendium of Broken Promises

Executive Summary

Putting Shareholders First: A New Era at Mack-Cali Since its 1994 IPO, Mack-Cali (“CLI”, or the “Company”) has perennially disappointed shareholders. Over the last five years management and the Legacy Directors(1) have perpetuated this value destruction; as a result, Mack-Cali is now in a financially precarious position and lacks a coherent long-term strategy The Legacy Board’s strategy has not delivered results for shareholders… • Mack-Cali shareholders are now entering the fifth year of Mr. DeMarco’s “Waterfront Strategy,” a vision that combines commercial (office) and residential assets along the Jersey City coast • This strategy fails to coherently address Mack-Cali’s fundamental structural issues: a) high leverage, b) diverse asset mix, c) large development pipeline, and d) expensive joint ventures • During a period of significant Net Asset Value (NAV) growth across the real estate industry, Mack-Cali shares have underperformed all relevant metrics: NAV is flat, debt is up, cash flow is down. Shares have significantly underperformed peers over nearly any time period dating back to the Company’s 1994 IPO …overseen by entrenched Legacy Board that advances its own interests at shareholders’ expense • The Legacy Directors on Mack-Cali’s Board have proven poor fiduciaries for shareholders. Their actions (or lack thereof) are a reflection of a culture that prioritizes the interests of the Company’s founder and management over those of shareholders Wide-ranging, comprehensive change is required to save Mack-Cali

Bow Street: Who We Are and Why We Are Here (Again) Bow Street LLC owns ~4.9% of Mack-Cali’s outstanding shares and is advocating for change on behalf of all shareholders at the 2020 Annual Meeting • Bow Street LLC is a New-York based investment manager founded in 2011 that partners with institutional investors and family offices globally to invest opportunistically across idiosyncratic markets and situations – This proxy submission is only the second since our Firm’s founding; our first proxy submission occurred last year, also at Mack-Cali—we are not activists – We own assets in both public and private markets, and have extensive real estate experience • In 2019, 4 independent directors nominated by Bow Street were elected to CLI’s Board – over 80% of shareholders voted for Bow Street’s proxy card; but as a minority, these directors were marginalized and prevented from fulfilling their roles by CLI’s management and Legacy Directors • While we had no expectations of engaging in another proxy contest, we now believe CLI’s poor governance culture must be completely uprooted for the Company to finally thrive. As such, we have returned with the goal of bringing objectivity and independence back to the CLI boardroom • Our capital is long-dated, and our investment time-horizon is significant; we have one goal – to maximize long-term value for all Mack-Cali shareholders We believe the Legacy Board has failed Mack-Cali shareholders; new leadership is essential to determining the right strategic path forward

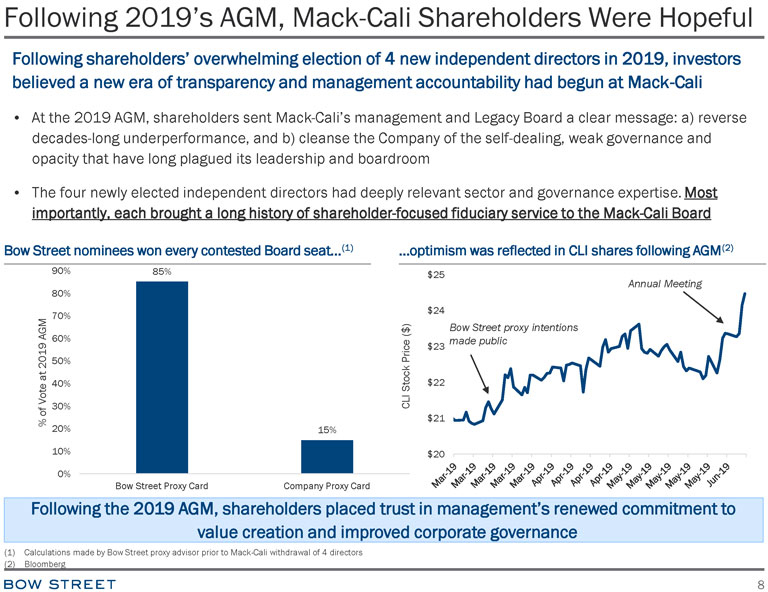

Following 2019’s AGM, Mack-Cali Shareholders Were Hopeful Following shareholders’ overwhelming election of 4 new independent directors in 2019, investors believed a new era of transparency and management accountability had begun at Mack-Cali • At the 2019 AGM, shareholders sent Mack-Cali’s management and Legacy Board a clear message: a) reverse decades-long underperformance, and b) cleanse the Company of the self-dealing, weak governance and opacity that have long plagued its leadership and boardroom • The four newly elected independent directors had deeply relevant sector and governance expertise. Most importantly, each brought a long history of shareholder-focused fiduciary service to the Mack-Cali Board Bow Street nominees won every contested Board seat…(1) …optimism was reflected in CLI shares following AGM(2) Following the 2019 AGM, shareholders placed trust in management’s renewed commitment to value creation and improved corporate governance

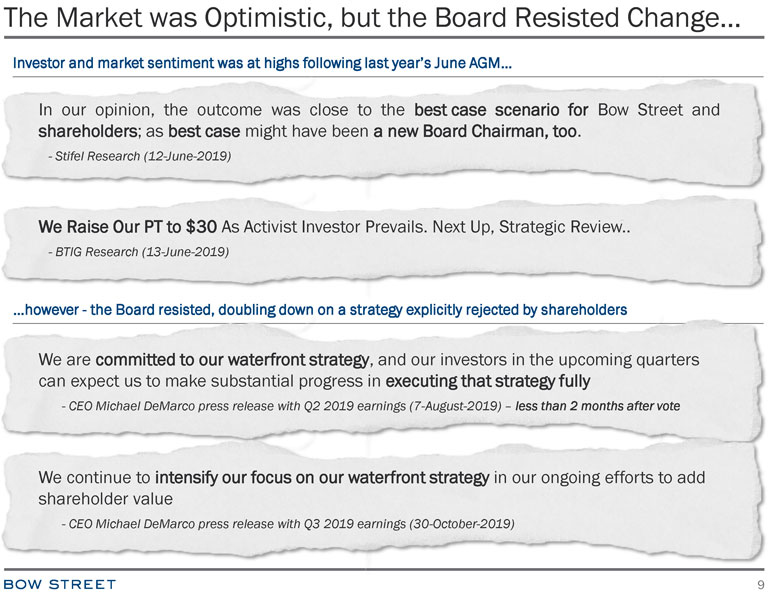

The Market was Optimistic, but the Board Resisted Change… Investor and market sentiment was at highs following last year’s June AGM… In our opinion, the outcome was close to the best case scenario for Bow Street and shareholders; as best case might have been a new Board Chairman, too. - Stifel Research (12-June-2019) We Raise Our PT to $30 As Activist Investor Prevails. Next Up, Strategic Review.. - BTIG Research (13-June-2019) …however—the Board resisted, doubling down on a strategy explicitly rejected by shareholders We are committed to our waterfront strategy, and our investors in the upcoming quarters can expect us to make substantial progress in executing that strategy fully - CEO Michael DeMarco press release with Q2 2019 earnings (7-August-2019) – less than 2 months after vote We continue to intensify our focus on our waterfront strategy in our ongoing efforts to add shareholder value - CEO Michael DeMarco press release with Q3 2019 earnings (30-October-2019)

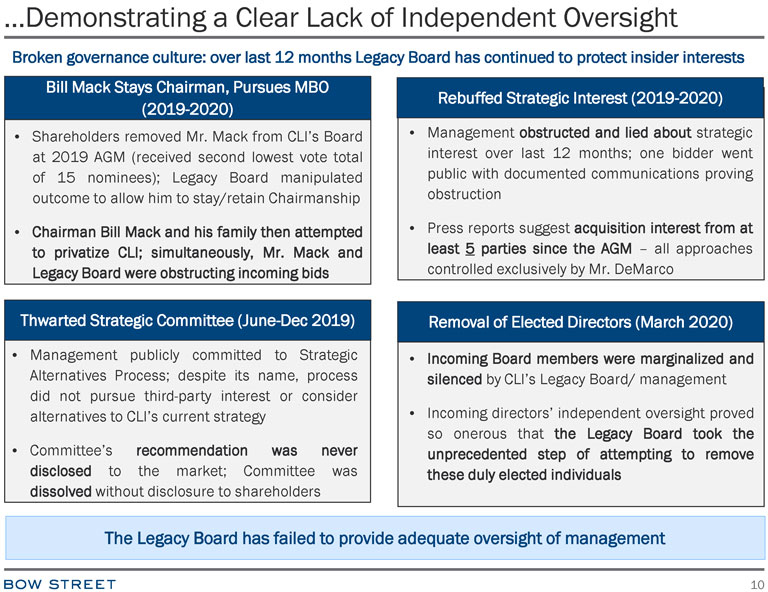

Demonstrating a Clear Lack of Independent Oversight Broken governance culture: over last 12 months Legacy Board has continued to protect insider interests Bill Mack Stays Chairman, Pursues MBO (2019-2020) • Shareholders removed Mr. Mack from CLI’s Board at 2019 AGM (received second lowest vote total of 15 nominees); Legacy Board manipulated outcome to allow him to stay/retain Chairmanship • Chairman Bill Mack and his family then attempted to privatize CLI; simultaneously, Mr. Mack and Legacy Board were obstructing incoming bids Rebuffed Strategic Interest (2019-2020) • Management obstructed and lied about strategic interest over last 12 months; one bidder went public with documented communications proving obstruction • Press reports suggest acquisition interest from at least 5 parties since the AGM – all approaches controlled exclusively by Mr. DeMarco Thwarted Strategic Committee (June-Dec 2019) • Management publicly committed to Strategic Alternatives Process; despite its name, process did not pursue third-party interest or consider alternatives to CLI’s current strategy • Committee’s recommendation was never disclosed to the market; Committee was dissolved without disclosure to shareholders Removal of Elected Directors (March 2020) • Incoming Board members were marginalized and silenced by CLI’s Legacy Board/ management • Incoming directors’ independent oversight proved so onerous that the Legacy Board took the unprecedented step of attempting to remove these duly elected individuals The Legacy Board has failed to provide adequate oversight of management

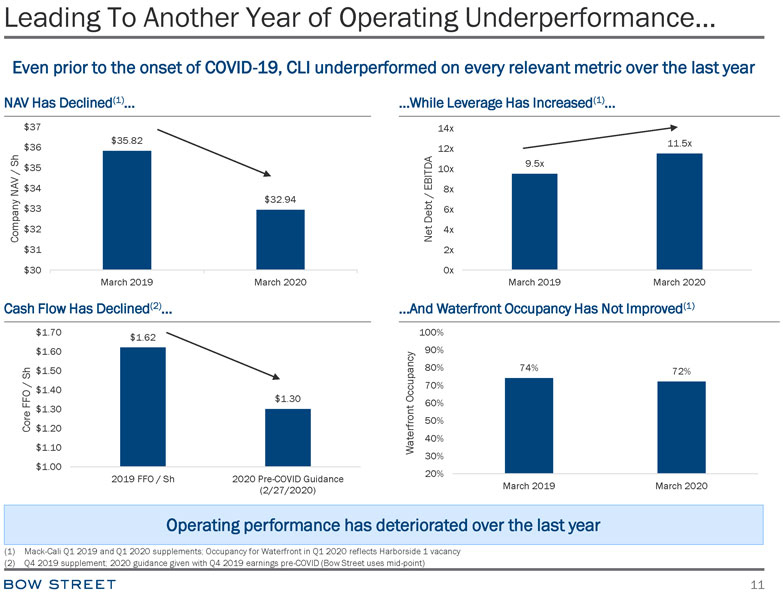

Leading To Another Year of Operating Underperformance… Even prior to the onset of COVID-19, CLI underperformed on every relevant metric over the last year Operating performance has deteriorated over the last year

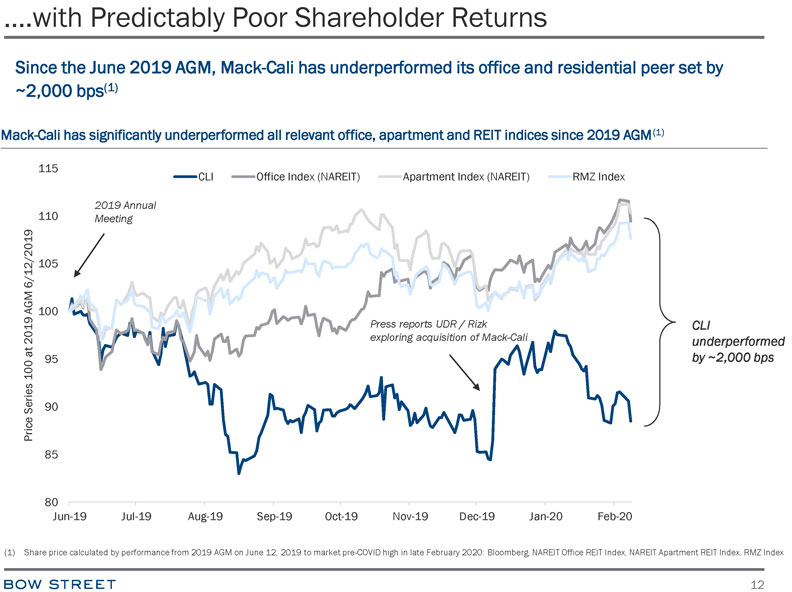

….with Predictably Poor Shareholder Returns Since the June 2019 AGM, Mack-Cali has underperformed its office and residential peer set by ~2,000 bps(1) Mack-Cali has significantly underperformed all relevant office, apartment and REIT indices since 2019 AGM(1) Share price calculated by performance from 2019 AGM on June 12, 2019 to market pre-COVID high in late February 2020; Bloomberg, NAREIT Office REIT Index, NAREIT Apartment REIT Index, RMZ Index

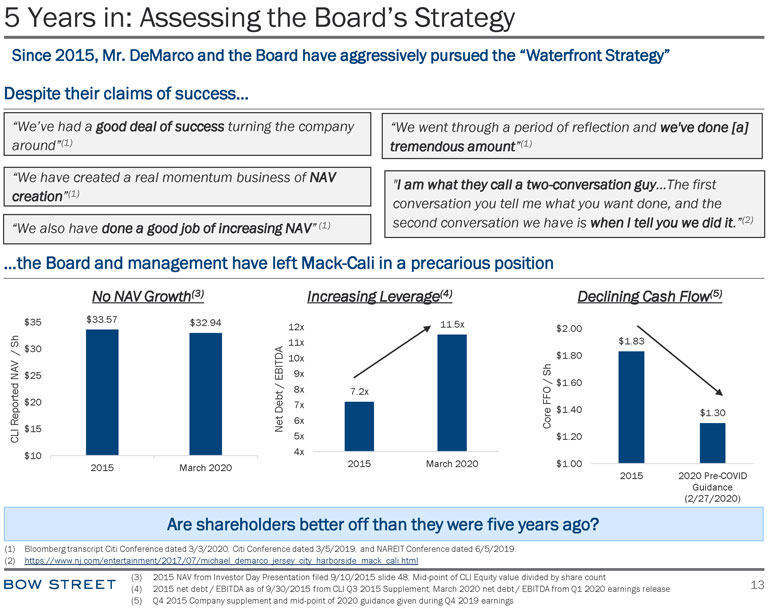

5 Years in: Assessing the Board’s Strategy Since 2015, Mr. DeMarco and the Board have aggressively pursued the “Waterfront Strategy” Despite their claims of success… “We’ve had a good deal of success turning the company “We went through a period of reflection and we’ve done [a] around”(1) tremendous amount”(1) “We have created a real momentum business of NAV “I am what they call a two-conversation guy…The first creation” (1) conversation you tell me what you want done, and the second conversation we have is when I tell you we did it.” (2) “We also have done a good job of increasing NAV” (1) …the Board and management have left Mack-Cali in a precarious position No NAV Growth(3) Increasing Leverage(4) Declining Cash Flow(5) Are shareholders better off than they were five years ago?

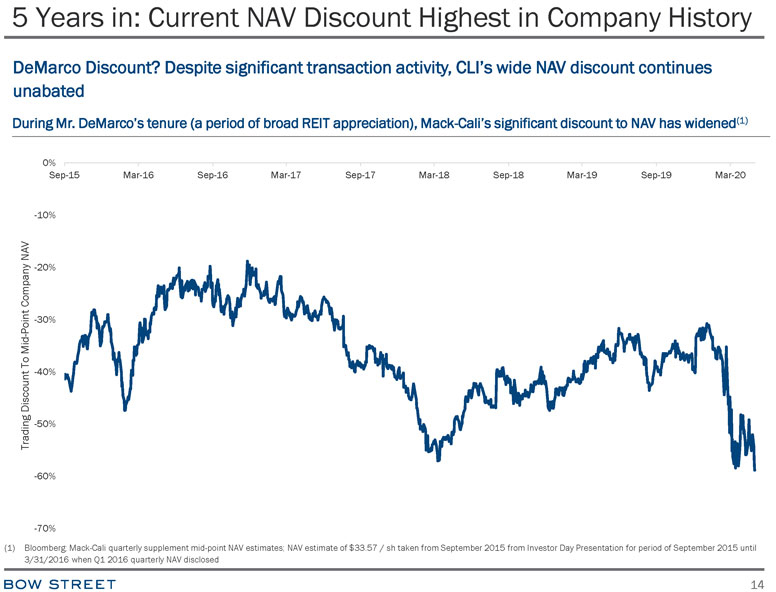

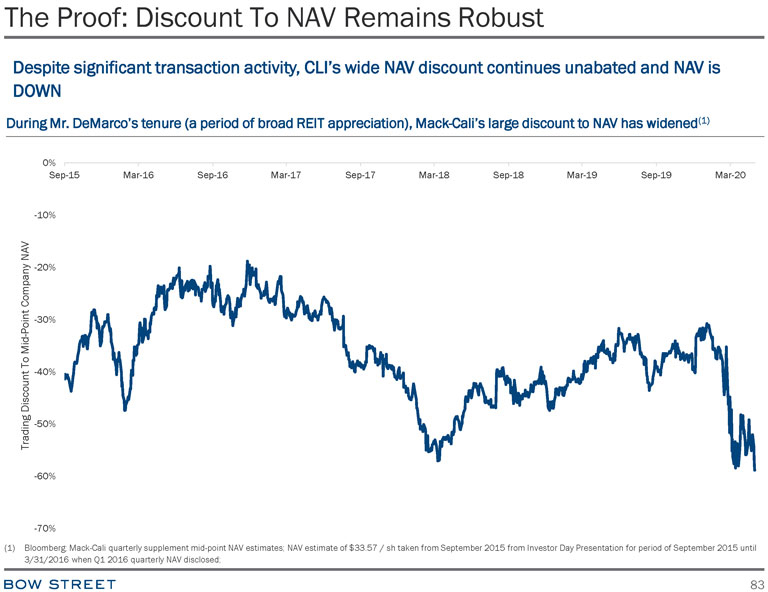

5 Years in: Current NAV Discount Highest in Company History DeMarco Discount? Despite significant transaction activity, CLI’s wide NAV discount continues unabated During Mr. DeMarco’s tenure (a period of broad REIT appreciation), Mack-Cali’s significant discount to NAV has widened(1)

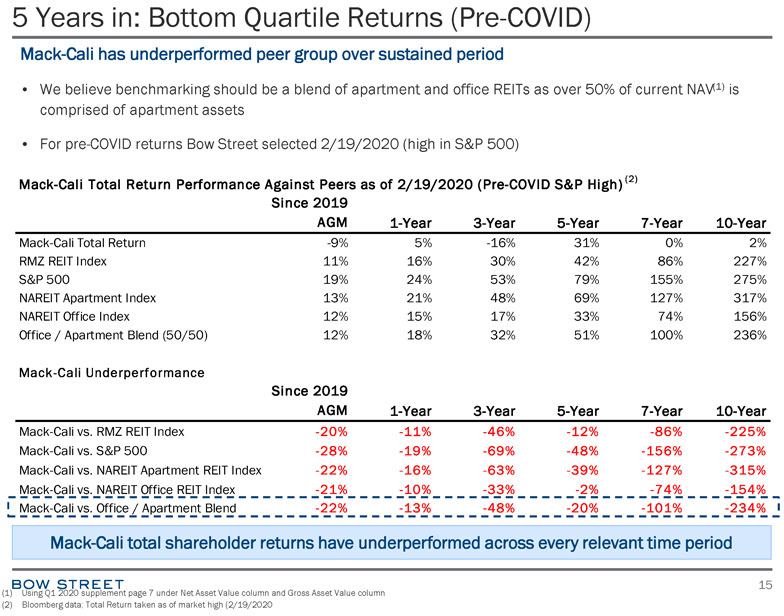

5 Years in: Bottom Quartile Returns (Pre-COVID) Mack-Cali has underperformed peer group over sustained period • We believe benchmarking should be a blend of apartment and office REITs as over 50% of current NAV(1) is comprised of apartment assets • For pre-COVID returns Bow Street selected 2/19/2020 (high in S&P 500) Mack-Cali Total Return Performance Against Peers as of 2/19/2020 (Pre-COVID S&P High) (2) Since 2019 AGM 1-Year 3-Year 5-Year 7-Year 10-Year Mack-Cali Total Return -9% 5% -16% 31% 0% 2% RMZ REIT Index 11% 16% 30% 42% 86% 227% S&P 500 19% 24% 53% 79% 155% 275% NAREIT Apartment Index 13% 21% 48% 69% 127% 317% NAREIT Office Index 12% 15% 17% 33% 74% 156% Office / Apartment Blend (50/50) 12% 18% 32% 51% 100% 236% Mack-Cali Underperformance Since 2019 AGM 1-Year 3-Year 5-Year 7-Year 10-Year Mack-Cali vs. RMZ REIT Index -20% -11% -46% -12% -86% -225% Mack-Cali vs. S&P 500 -28% -19% -69% -48% -156% -273% Mack-Cali vs. NAREIT Apartment REIT Index -22% -16% -63% -39% -127% -315% Mack-Cali vs. NAREIT Office REIT Index -21% -10% -33% -2% -74% -154% Mack-Cali vs. Office / Apartment Blend -22% -13% -48% -20% -101% -234% Mack-Cali total shareholder returns have underperformed across every relevant time period

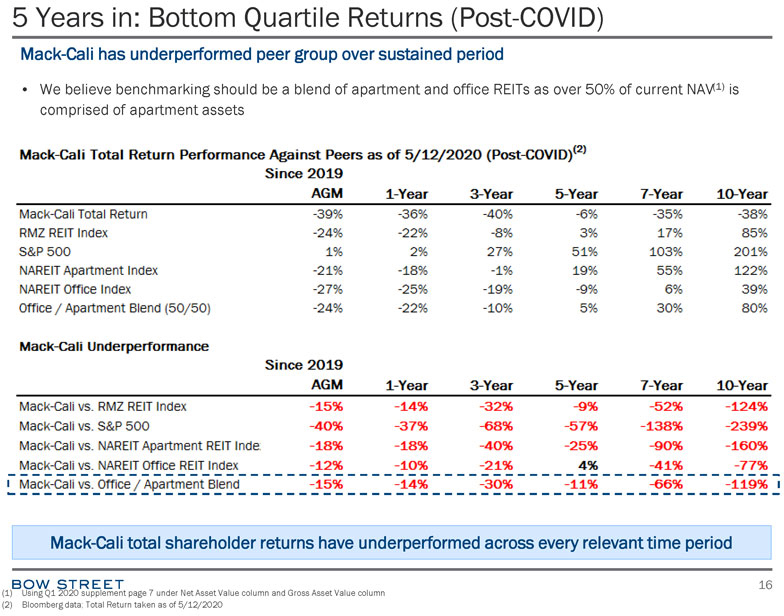

Mack-Cali total shareholder returns have underperformed across every relevant time period 5 Years in: Bottom Quartile Returns (Post-COVID) Mack-Cali has underperformed peer group over sustained period • We believe benchmarking should be a blend of apartment and office REITs as over 50% of current NAV(1) is comprised of apartment assets

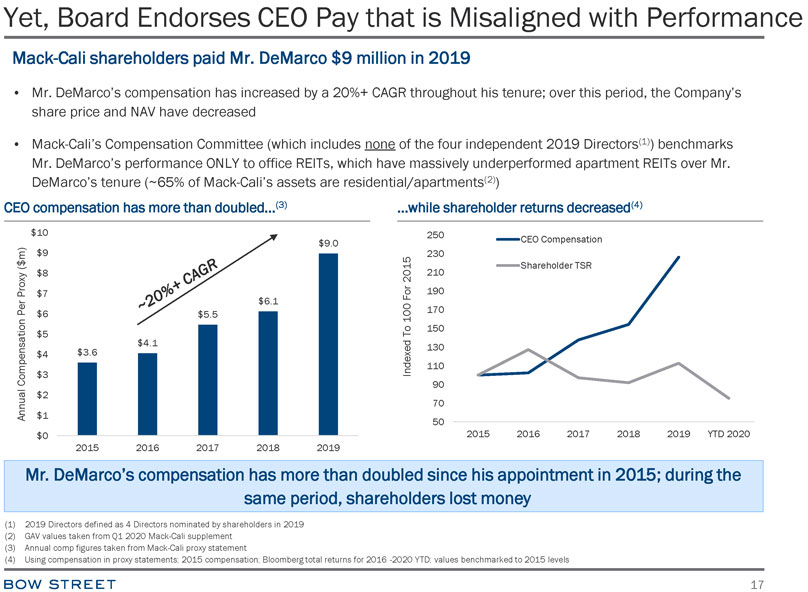

Yet, Board Endorses CEO Pay that is Misaligned with Performance Mack-Cali shareholders paid Mr. DeMarco $9 million in 2019 • Mr. DeMarco’s compensation has increased by a 20%+ CAGR throughout his tenure; over this period, the Company’s share price and NAV have decreased • Mack-Cali’s Compensation Committee (which includes none of the four independent 2019 Directors(1)) benchmarks Mr. DeMarco’s performance ONLY to office REITs, which have massively underperformed apartment REITs over Mr. DeMarco’s tenure (~65% of Mack-Cali’s assets are residential/apartments (2) ) CEO compensation has more than doubled… (3) …while shareholder returns decreased (4) Mr. DeMarco’s compensation has more than doubled since his appointment in 2015; during the same period, shareholders lost money (1) 2019 Directors defined as 4 Directors nominated by shareholders in 2019 (2) GAV values taken from Q1 2020 Mack-Cali supplement (3) Annual comp figures taken from Mack-Cali proxy statement

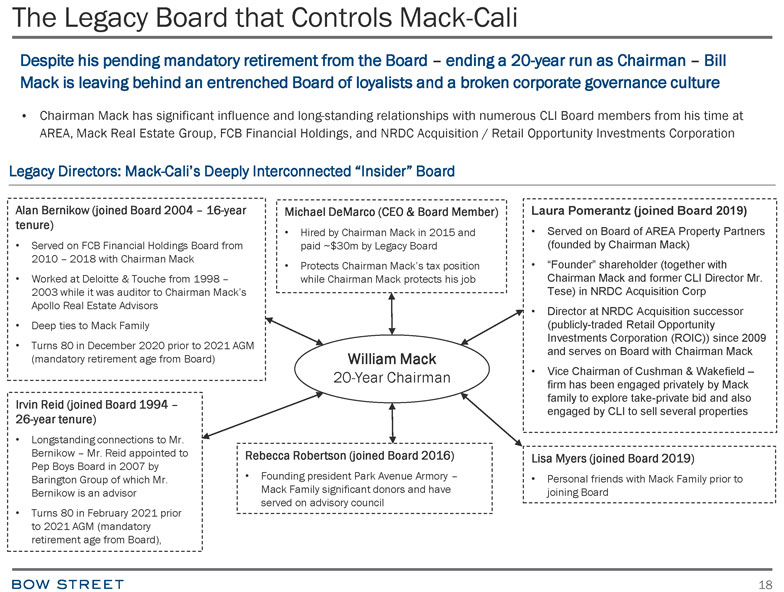

The Legacy Board that Controls Mack-Cali Despite his pending mandatory retirement from the Board – ending

a 20-year run as Chairman – Bill Mack is leaving behind an entrenched Board of loyalists and a broken corporate governance culture • Chairman Mack has significant influence and long-standing

relationships with numerous CLI Board members from his time at AREA, Mack Real Estate Group, FCB Financial Holdings, and NRDC Acquisition / Retail Opportunity Investments Corporation

Legacy Directors: Mack-Cali’s Deeply Interconnected “Insider” Board Alan Bernikow (joined Board 2004 – 16-year tenure)

• Served on FCB Financial Holdings Board from 2010 – 2018 with Chairman Mack • Worked at Deloitte & Touche from 1998 – 2003 while it was auditor to Chairman Mack’s Apollo Real Estate Advisors • Deep ties to

Mack Family • Turns 80 in December 2020 prior to 2021 AGM (mandatory retirement age from Board) Michael DeMarco (CEO & Board Member) • Hired by Chairman Mack in 2015 and paid ~$30m by Legacy Board • Protects Chairman

Mack’s tax position while Chairman Mack protects his job Laura Pomerantz (joined Board 2019) • Served on Board of AREA Property Partners (founded by Chairman Mack) • “Founder” shareholder (together with Chairman Mack and

former CLI Director Mr. Tese) in NRDC Acquisition Corp • Director at NRDC Acquisition successor (publicly-traded Retail Opportunity Investments Corporation (ROIC)) since 2009 and serves on Board with Chairman Mack • Vice Chairman of

Cushman & Wakefield –firm has been engaged privately by Mack family to explore take-private bid and also engaged by CLI to sell several properties William Mack 20-Year Chairman Irvin Reid (joined

Board 1994 – 26-year tenure) • Longstanding connections to Mr. Bernikow – Mr. Reid appointed to Pep Boys Board in 2007 by Barington Group of which Mr. Bernikow is an advisor

• Turns 80 in February 2021 prior to 2021 AGM (mandatory retirement age from Board), Rebecca Robertson (joined Board 2016) • Founding president Park Avenue Armory –Mack Family significant donors and have served on advisory council

Lisa Myers (joined Board 2019) • Personal friends with Mack Family prior to joining Board

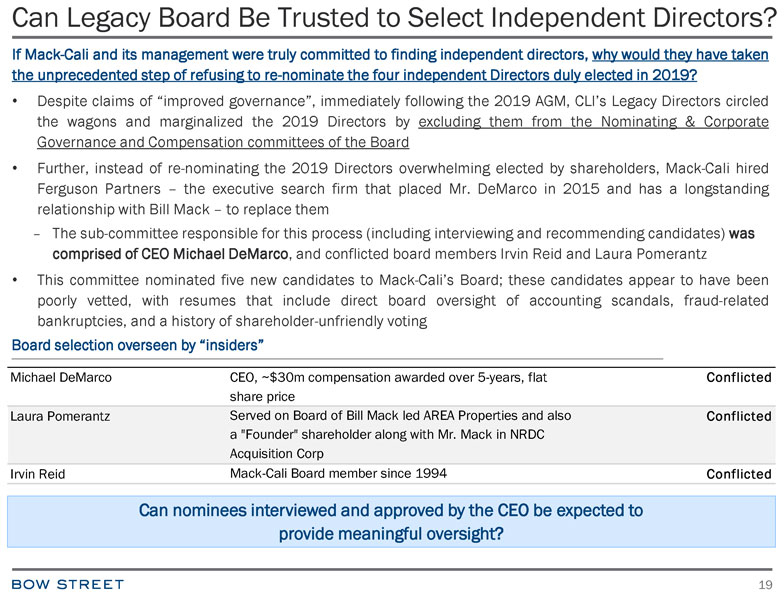

Can Legacy Board Be Trusted to Select Independent Directors? If Mack-Cali and its management were truly committed to finding independent directors, why would they have taken the unprecedented step of refusing to re-nominate the four independent Directors duly elected in 2019? • Despite claims of “improved governance”, immediately following the 2019 AGM, CLI’s Legacy Directors circled the wagons and marginalized the 2019 Directors by excluding them from the Nominating & Corporate Governance and Compensation committees of the Board • Further, instead of re-nominating the 2019 Directors overwhelming elected by shareholders, Mack-Cali hired Ferguson Partners – the executive search firm that placed Mr. DeMarco in 2015 and has a longstanding relationship with Bill Mack – to replace them – The sub-committee responsible for this process (including interviewing and recommending candidates) was comprised of CEO Michael DeMarco, and conflicted board members Irvin Reid and Laura Pomerantz • This committee nominated five new candidates to Mack-Cali’s Board; these candidates appear to have been poorly vetted, with resumes that include direct board oversight of accounting scandals, fraud-related bankruptcies, and a history of shareholder-unfriendly voting Board selection overseen by “insiders” Michael DeMarco CEO, ~$30m compensation awarded over 5-years, flat Conflicted share price Laura Pomerantz Served on Board of Bill Mack led AREA Properties and also Conflicted a “Founder” shareholder along with Mr. Mack in NRDC Acquisition Corp Irvin Reid Mack-Cali Board member since 1994 Conflicted Can nominees interviewed and approved by the CEO be expected to provide meaningful oversight?

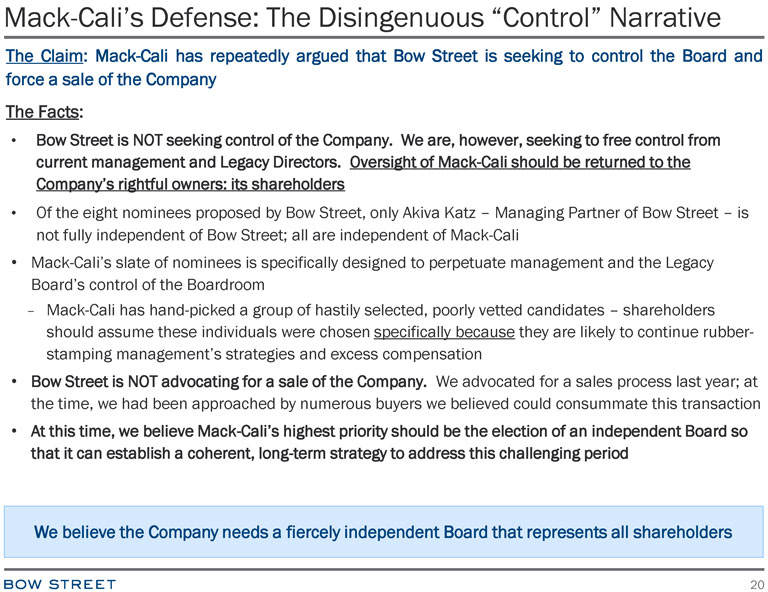

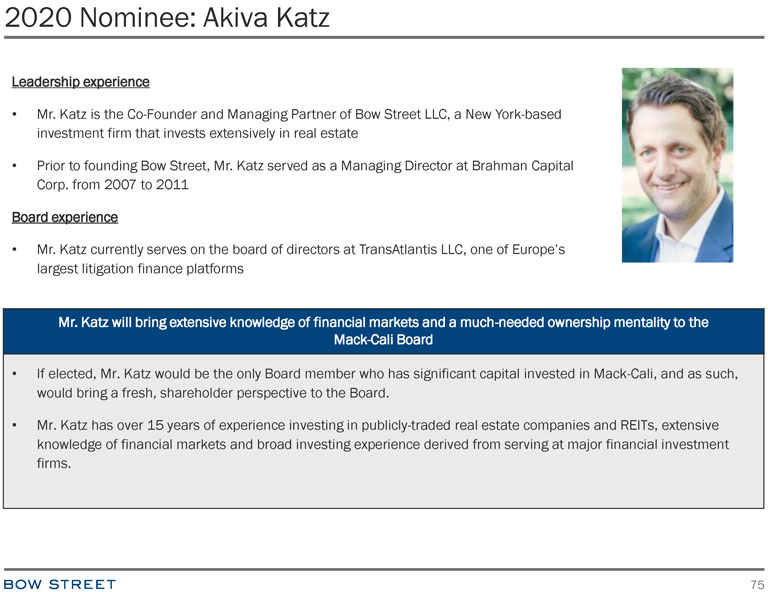

Mack-Cali’s Defense: The Disingenuous “Control” Narrative The Claim: Mack-Cali has repeatedly argued that Bow Street is seeking to control the Board and force a sale of the Company The Facts: • Bow Street is NOT seeking control of the Company. We are, however, seeking to free control from current management and Legacy Directors. Oversight of Mack-Cali should be returned to the Company’s rightful owners: its shareholders • Of the eight nominees proposed by Bow Street, only Akiva Katz – Managing Partner of Bow Street – is not fully independent of Bow Street; all are independent of Mack-Cali • Mack-Cali’s slate of nominees is specifically designed to perpetuate management and the Legacy Board’s control of the Boardroom – Mack-Cali has hand-picked a group of hastily selected, poorly vetted candidates – shareholders should assume these individuals were chosen specifically because they are likely to continue rubber-stamping management’s strategies and excess compensation • Bow Street is NOT advocating for a sale of the Company. We advocated for a sales process last year; at the time, we had been approached by numerous buyers we believed could consummate this transaction • At this time, we believe Mack-Cali’s highest priority should be the election of an independent Board so that it can establish a coherent, long-term strategy to address this challenging period We believe the Company needs a fiercely independent Board that represents all shareholders

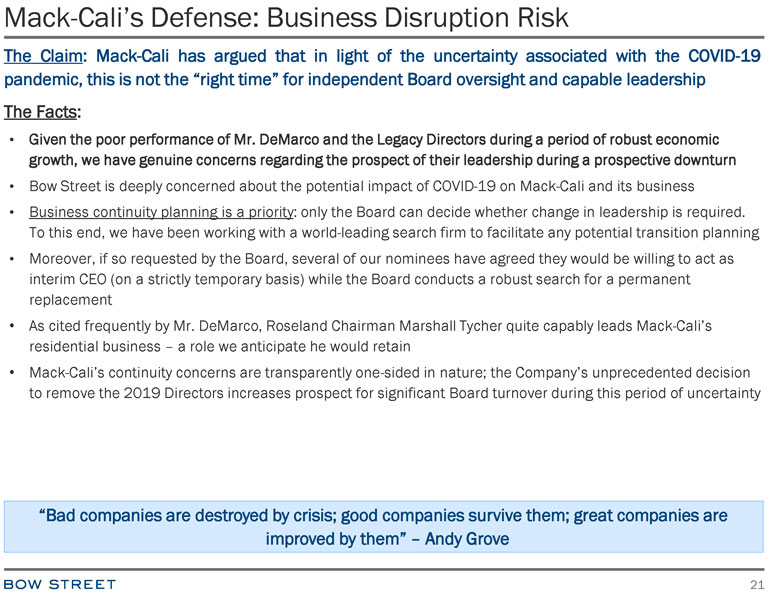

Mack-Cali’s Defense: Business Disruption Risk The Claim: Mack-Cali has argued that in light of the uncertainty associated with the COVID-19 pandemic, this is not the “right time” for independent Board oversight and capable leadership The Facts: • Given the poor performance of Mr. DeMarco and the Legacy Directors during a period of robust economic growth, we have genuine concerns regarding the prospect of their leadership during a prospective downturn • Bow Street is deeply concerned about the potential impact of COVID-19 on Mack-Cali and its business • Business continuity planning is a priority: only the Board can decide whether change in leadership is required. To this end, we have been working with a world-leading search firm to facilitate any potential transition planning • Moreover, if so requested by the Board, several of our nominees have agreed they would be willing to act as interim CEO (on a strictly temporary basis) while the Board conducts a robust search for a permanent replacement • As cited frequently by Mr. DeMarco, Roseland Chairman Marshall Tycher quite capably leads Mack-Cali’s residential business – a role we anticipate he would retain • Mack-Cali’s continuity concerns are transparently one-sided in nature; the Company’s unprecedented decision to remove the 2019 Directors increases prospect for significant Board turnover during this period of uncertainty “Bad companies are destroyed by crisis; good companies survive them; great companies are improved by them” – Andy Grove

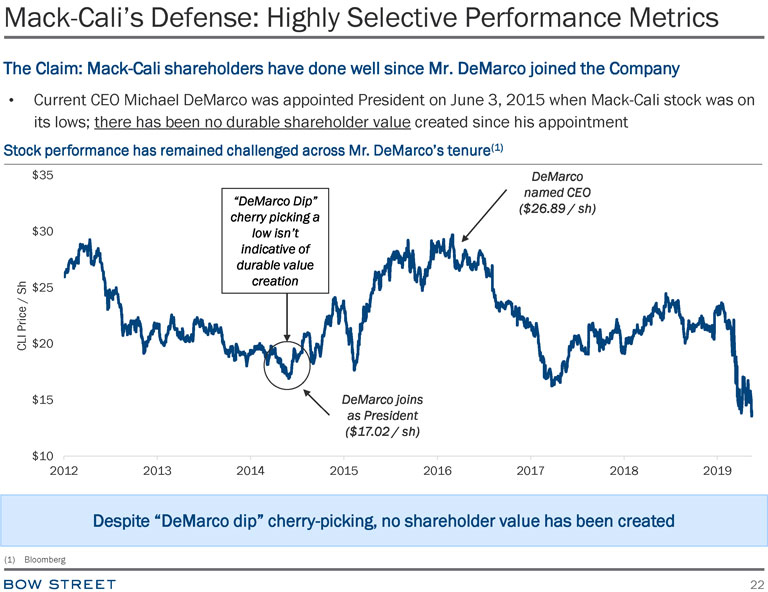

Mack-Cali’s Defense: Highly Selective Performance Metrics The Claim: Mack-Cali shareholders have done well since Mr. DeMarco joined the Company • Current CEO Michael DeMarco was appointed President on June 3, 2015 when Mack-Cali stock was on its lows; there has been no durable shareholder value created since his appointment Stock performance has remained challenged across Mr. DeMarco’s tenure(1) Despite “DeMarco dip” cherry-picking, no shareholder value has been created

A New Era At Mack-Cali: The Path Forward A new, independent Board is required to create a coherent strategy for long-term value realization • Despite its strong collection of assets, it is clear that the current strategy has failed to either grow NAV or close the discount to NAV. We believe that in order to trade in line with peers, Mack-Cali must start looking a lot more like its peers 1) High Integrity Leadership – Mack-Cali’s current culture is toxic, benefitting management and the Legacy Directors over all other stakeholders 2) Simplify Residential Platform – Residential platform should be restructured to prepare for an eventual separation of the business 3) Restructure Office Portfolio – Reposition office portfolio by selling sub-institutional suburban properties and investing in Harborside properties 4) Focus on Delivering Promised Leverage Reductions – CLI cannot expect to close the discount to its peer group while its leverage is 2x peers 5) Genuine Receptivity (as Opposed to Hostility) to Prospective Sale Proposals – Periodic assessments of capital markets to evaluate larger transactions for crystalizing shareholder value 6) Strong Independent Board and Oversight – Strategy directly overseen by strong and independent Board which holds management accountable Meaningful Board change is needed to break with CLI’s legacy of underperformance

Are Shareholders Better Off Than They Were 5-Years Ago? A Clear-eyed Assessment Of Management’s Tenure

“Our first responsibility and our chief goal is to close the gap between what we perceive our NAV to be and what our share price is…We’ll do whatever it takes to make NAV a reality as opposed to a possibility” - Michael DeMarco’s first earnings call with Mack-Cali 7/22/2015, when NAV was $33/share and CLI share price was $20.27 (current NAV remains $33/share, current CLI share price $13.71)

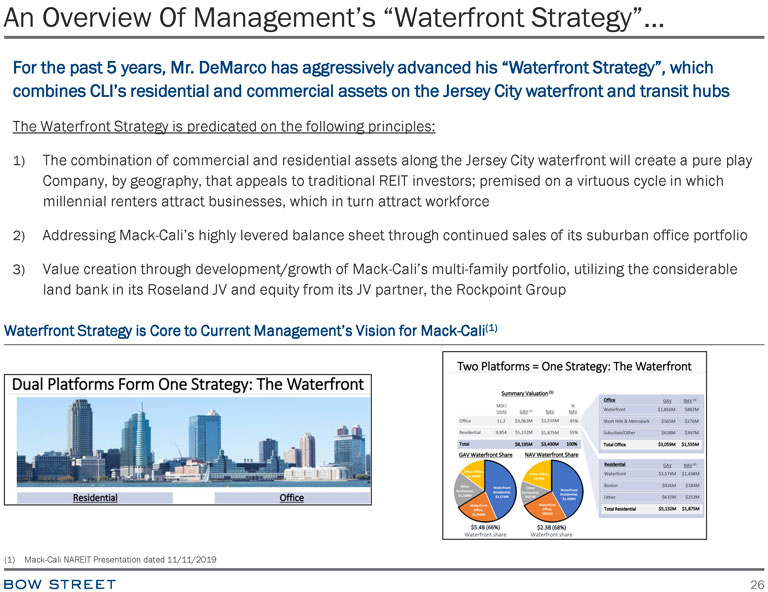

An Overview Of Management’s “Waterfront Strategy”… For the past 5 years, Mr. DeMarco has aggressively advanced his “Waterfront Strategy”, which combines CLI’s residential and commercial assets on the Jersey City waterfront and transit hubs The Waterfront Strategy is predicated on the following principles: 1) The combination of commercial and residential assets along the Jersey City waterfront will create a pure play Company, by geography, that appeals to traditional REIT investors; premised on a virtuous cycle in which millennial renters attract businesses, which in turn attract workforce 2) Addressing Mack-Cali’s highly levered balance sheet through continued sales of its suburban office portfolio 3) Value creation through development/growth of Mack-Cali’s multi-family portfolio, utilizing the considerable land bank in its Roseland JV and equity from its JV partner, the Rockpoint Group Waterfront Strategy is Core to Current Management’s Vision for Mack-Cali(1)

…that was Ill-Conceived from the Start Waterfront Strategy failed to consider inherent constraints/preferences of traditional REIT investors 1) High leverage: management’s strategy is capital intensive, emphasizing prospective growth over cash flow; now at an industry high 11.5x EBITDA, leverage is a fundamental concern for institutional investors and research analysts 2) Dividend sustainability: asset sales and commensurate cash flow dilution threatened sustainability of Mack- Cali’s dividend – traditional REIT investors don’t like prospective dividend-cuts 3) Structure/asset mix not conducive to public markets: – Diversified REITs trade at widest discounts to NAV – For many years, REITs with assets across diverse asset classes have underperformed– these tend to trade at “lowest common denominator” multiples – REIT investors consistently penalize geographic concentration – REITs focused on a single geography tend to underperform; with a focus on Jersey City (population: 300K), this issue is amplified at Mack-Cali – Excess development exposure – REIT investors are highly sensitive to the percentage of asset value comprised of development assets as land does not produce cash-flow and has a highly volatile valuation profile; at Mack-Cali, this was an industry high ~23%(1) – successful REITs carefully manage development exposure (if any) 4) Joint ventures and preferred structures add complexity, obfuscate value: Public REIT investors strongly dislike large JV/ preferred equity structures; through Mack-Cali’s Rockpoint JV, Mr. DeMarco has consistently ceded value in the Company’s most valuable assets. JV viewed as an impediment by prospective acquirors Five years into this strategy, NAV is flat and CLI has – unsurprisingly – failed to close NAV discount

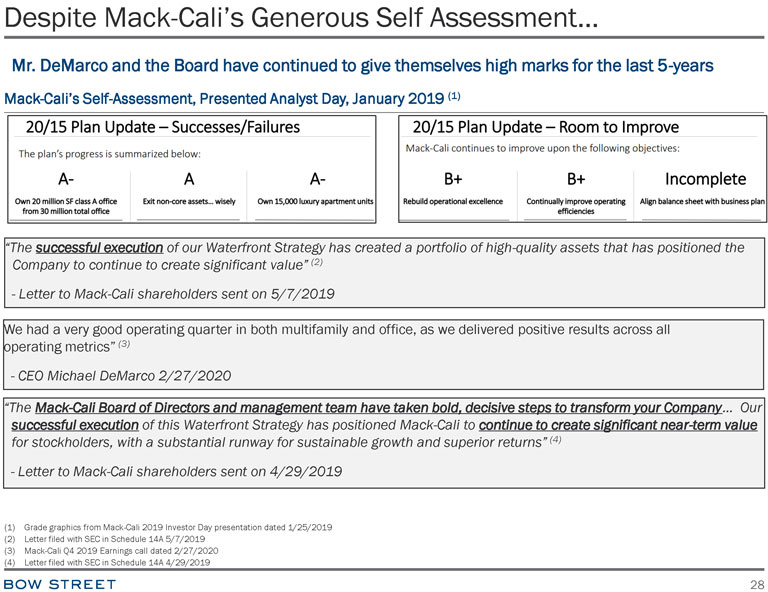

Despite Mack-Cali’s Generous Self Assessment… Mr. DeMarco and the Board have continued to give themselves high marks for the last 5-years Mack-Cali’s Self-Assessment, Presented Analyst Day, January 2019 (1) “The successful execution of our Waterfront Strategy has created a portfolio of high-quality assets that has positioned the Company to continue to create significant value”(2) - Letter to Mack-Cali shareholders sent on 5/7/2019 We had a very good operating quarter in both multifamily and office, as we delivered positive results across all operating metrics”(3) - CEO Michael DeMarco 2/27/2020 “The Mack-Cali Board of Directors and management team have taken bold, decisive steps to transform your Company… Our successful execution of this Waterfront Strategy has positioned Mack-Cali to continue to create significant near-term value for stockholders, with a substantial runway for sustainable growth and superior returns”(4) - Letter to Mack-Cali shareholders sent on 4/29/2019 (1) Grade graphics from Mack-Cali 2019 Investor Day presentation dated 1/25/2019 (2) Letter filed with SEC in Schedule 14A 5/7/2019 (3) Mack-Cali Q4 2019 Earnings call dated 2/27/2020

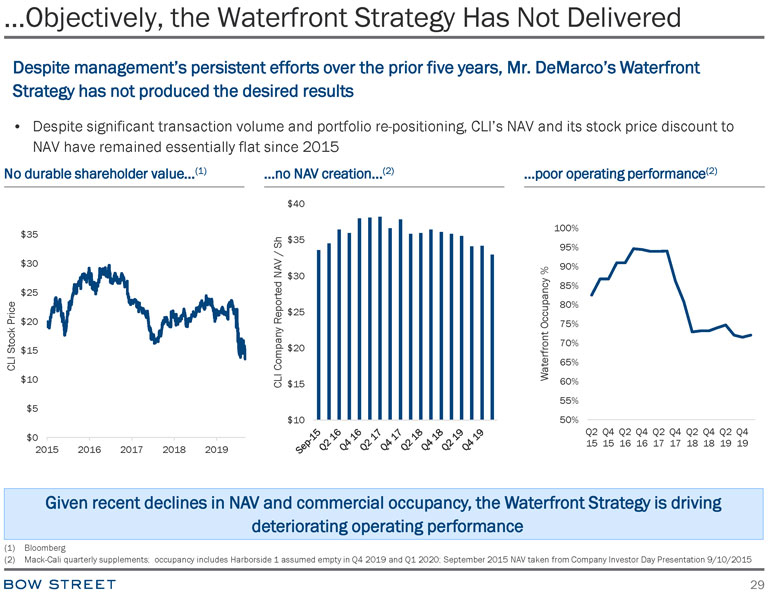

…Objectively, the Waterfront Strategy Has Not Delivered Despite management’s persistent efforts over the prior five years, Mr. DeMarco’s Waterfront Strategy has not produced the desired results • Despite significant transaction volume and portfolio re-positioning, CLI’s NAV and its stock price discount to NAV have remained essentially flat since 2015 No durable shareholder value…(1) …no NAV creation…(2) …poor operating performance(2) Given recent declines in NAV and commercial occupancy, the Waterfront Strategy is driving deteriorating operating performance

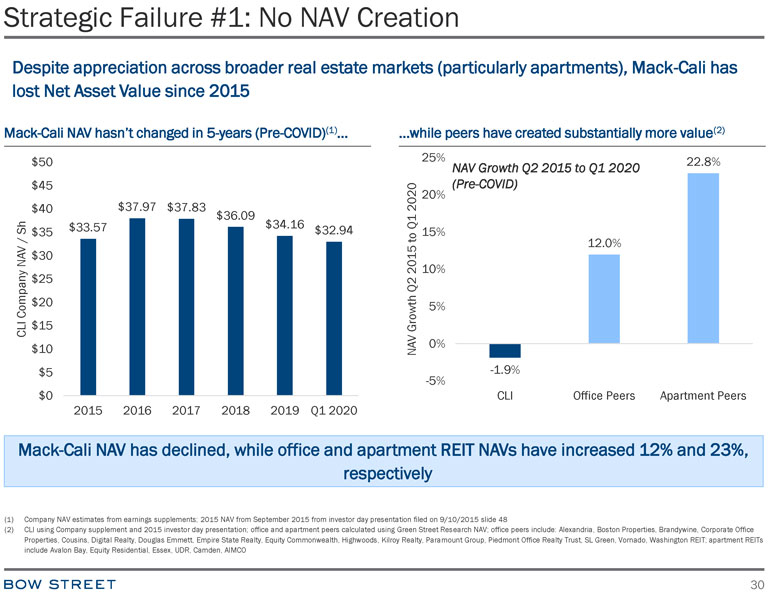

Strategic Failure #1: No NAV Creation Despite appreciation across broader real estate markets (particularly apartments), Mack-Cali has lost Net Asset Value since 2015 Mack-Cali NAV hasn’t changed in 5-years (Pre-COVID)(1)… …while peers have created substantially more value(2) Mack-Cali NAV has declined, while office and apartment REIT NAVs have increased 12% and 23%, respectively (1) Company NAV estimates from earnings supplements; 2015 NAV from September 2015 from investor day presentation filed on 9/10/2015 slide 48 (2) CLI using Company supplement and 2015 investor day presentation; office and apartment peers calculated using Green Street Research NAV; office peers include: Alexandria, Boston Properties, Brandywine, Corporate Office Properties, Cousins, Digital Realty, Douglas Emmett, Empire State Realty, Equity Commonwealth, Highwoods, Kilroy Realty, Paramount Group, Piedmont Office Realty Trust, SL Green, Vornado, Washington REIT; apartment REITs include Avalon Bay, Equity Residential, Essex, UDR, Camden, AIMCO

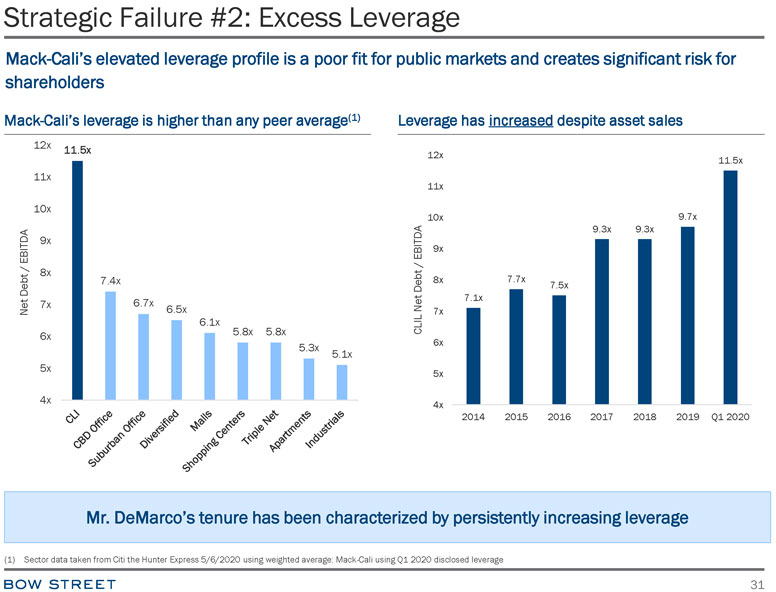

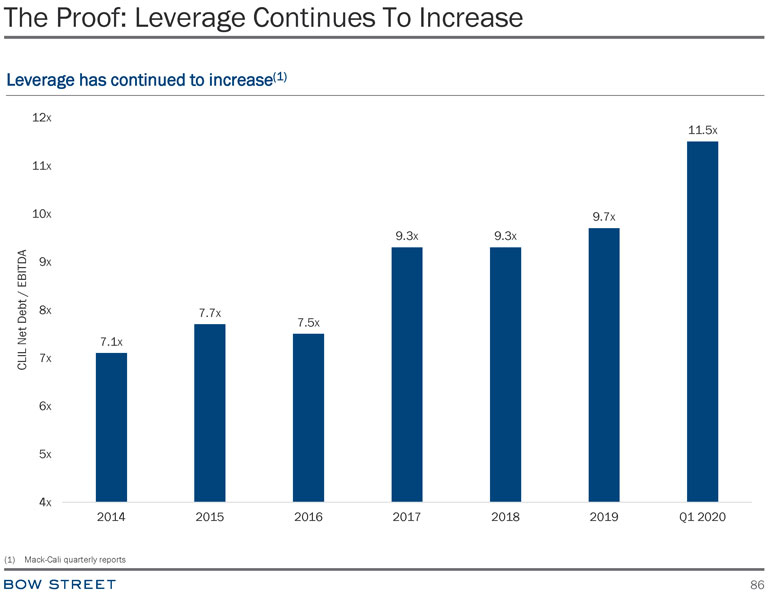

Strategic Failure #2: Excess Leverage Mack-Cali’s elevated leverage profile is a poor fit for public markets and creates significant risk for shareholders Mack-Cali’s leverage is higher than any peer average(1) Leverage has increased despite asset sales Mr. DeMarco’s tenure has been characterized by persistently increasing leverage

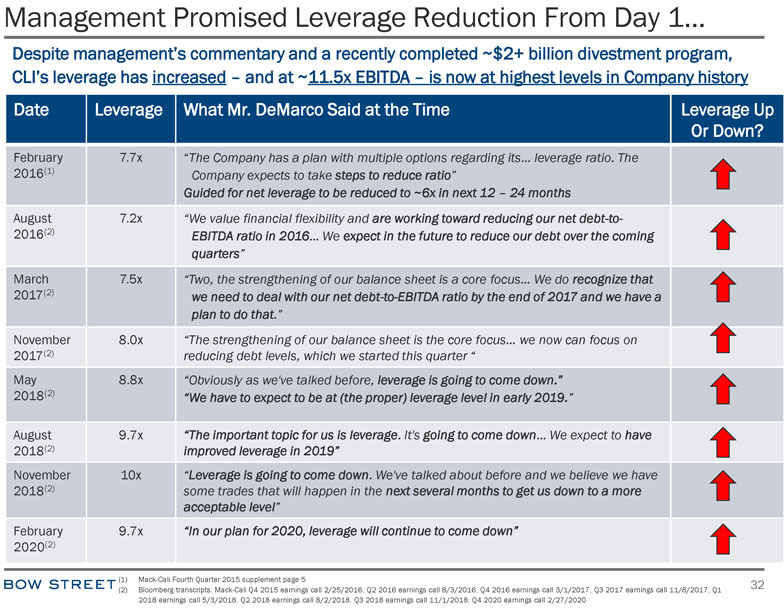

Management Promised Leverage Reduction From Day 1… Despite management’s commentary and a recently completed ~$2+ billion divestment program, CLI’s leverage has increased – and at ~11.5x EBITDA – is now at highest levels in Company history Date Leverage What Mr. DeMarco Said at the Time Leverage Up Or Down? February 7.7x “The Company has a plan with multiple options regarding its… leverage ratio. The 2016(1) Company expects to take steps to reduce ratio” Guided for net leverage to be reduced to ~6x in next 12 – 24 months August 7.2x “We value financial flexibility and are working toward reducing our net debt-to- 2016 (2) EBITDA ratio in 2016… We expect in the future to reduce our debt over the coming quarters” March 7.5x “Two, the strengthening of our balance sheet is a core focus… We do recognize that 2017(2) we need to deal with our net debt-to-EBITDA ratio by the end of 2017 and we have a plan to do that.” November 8.0x “The strengthening of our balance sheet is the core focus… we now can focus on 2017(2) reducing debt levels, which we started this quarter “ May 8.8x “Obviously as we’ve talked before, leverage is going to come down.” 2018(2) “We have to expect to be at (the proper) leverage level in early 2019.” August 9.7x “The important topic for us is leverage. It’s going to come down… We expect to have 2018(2) improved leverage in 2019” November 10x “Leverage is going to come down. We’ve talked about before and we believe we have 2018 (2) some trades that will happen in the next several months to get us down to a more acceptable level” February 9.7x “In our plan for 2020, leverage will continue to come down” 2020(2)

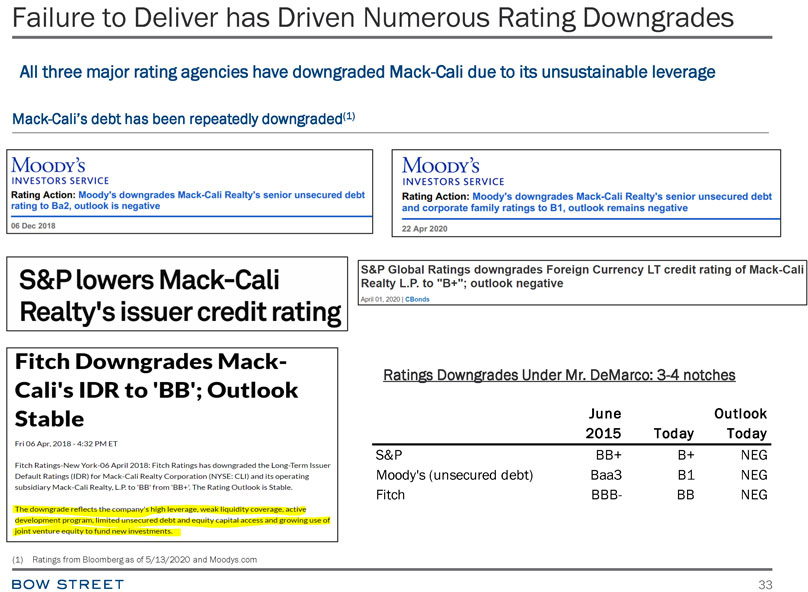

Failure to Deliver has Driven Numerous Rating Downgrades All three major rating agencies have downgraded Mack-Cali due to its unsustainable leverage Mack-Cali’s debt has been repeatedly downgraded(1) Ratings Downgrades Under Mr. DeMarco: 3-4 notches June Outlook 2015 Today Today S&P BB+ B+ NEG Moody’s (unsecured debt) Baa3 B1 NEG Fitch BBB- BB NEG

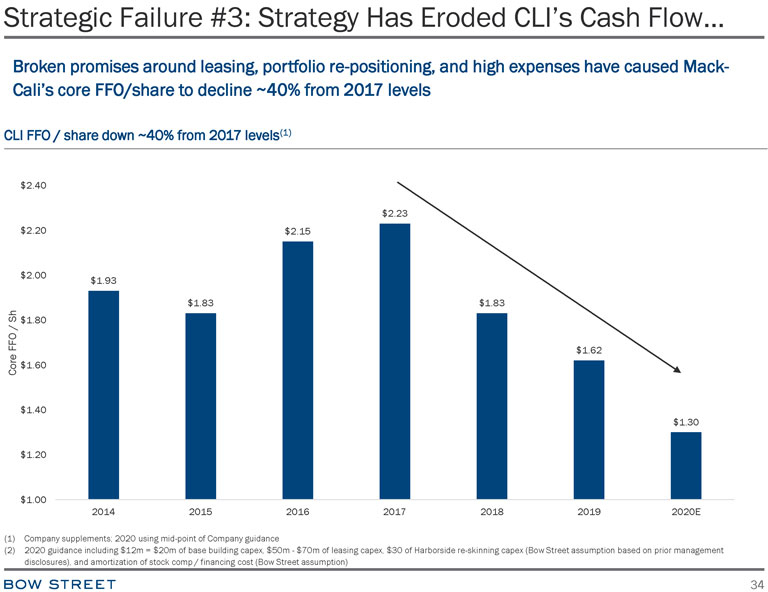

Strategic Failure #3: Strategy Has Eroded CLI’s Cash Flow… Broken promises around leasing, portfolio re-positioning, and high expenses have caused Mack- Cali’s core FFO/share to decline ~40% from 2017 levels CLI FFO / share down ~40% from 2017 levels(1)

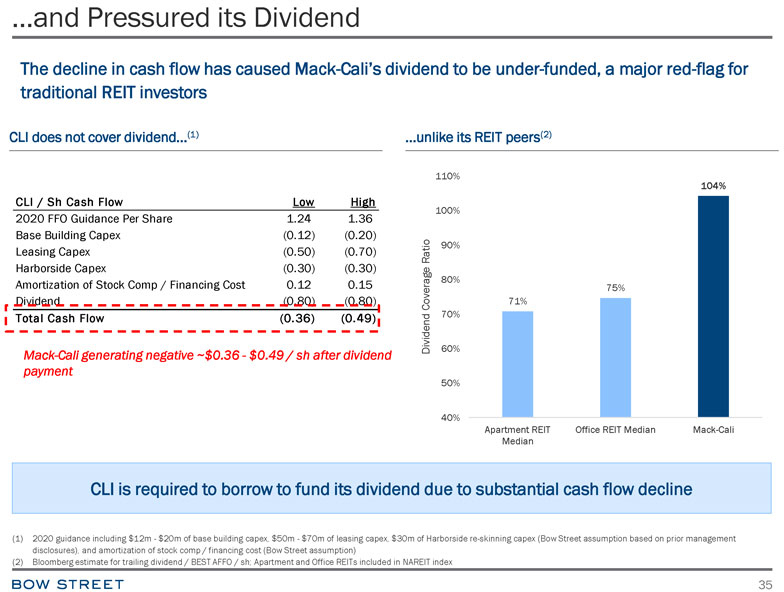

…and Pressured its Dividend The decline in cash flow has caused Mack-Cali’s dividend to be under-funded, a major red-flag for traditional REIT investors CLI does not cover dividend…(1) …unlike its REIT peers(2) CLI / Sh Cash Flow Low High 2020 FFO Guidance Per Share 1.24 1.36 Base Building Capex (0.12) (0.20) Leasing Capex (0.50) (0.70) Harborside Capex (0.30) (0.30) Amortization of Stock Comp / Financing Cost 0.12 0.15 Dividend (0.80) (0.80) Total Cash Flow (0.36) (0.49) Mack-Cali generating negative ~$0.36—$0.49 / sh after dividend payment CLI is required to borrow to fund its dividend due to substantial cash flow decline (1) 2020 guidance including $12m—$20m of base building capex, $50m—$70m of leasing capex, $30m of Harborside re-skinning capex (Bow Street assumption based on prior management disclosures), and amortization of stock comp / financing cost (Bow Street assumption)

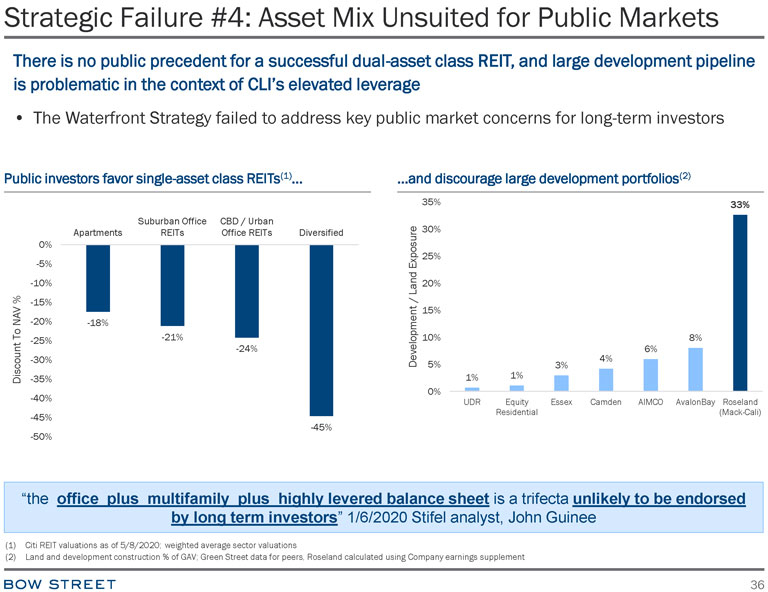

Strategic Failure #4: Asset Mix Unsuited for Public Markets There is no public precedent for a successful dual-asset class REIT, and large development pipeline is problematic in the context of CLI’s elevated leverage • The Waterfront Strategy failed to address key public market concerns for long-term investors Public investors favor single-asset class REITs(1)… …and discourage large development portfolios(2) “the office plus multifamily plus highly levered balance sheet is a trifecta unlikely to be endorsed by long term investors” 1/6/2020 Stifel analyst, John Guinee (1) Citi REIT valuations as of 5/8/2020; weighted average sector valuations

Strategic Failure #5: Mack-Cali’s JVs are Deceivingly Dilutive By using complex preferred equity from Rockpoint Group to finance its residential development, Mack-Cali has subordinated its shareholders and created a poison pill against future strategic transactions • Given Mack-Cali’s cash-flow constraints, management and the Board chose to pursue alternative financing to execute on residential development; regularly touted by management as an attractive source of capital, private equity is actually the most expensive form of capital. These joint-ventures transfer CLI’s most valuable assets away from public shareholders with no control premium – Structurally Unfavorable—JV deal entails preferred hurdles, subordinating CLI shareholders – Deleterious to Valuation—Public markets apply significant discounts to JV structures and cash flow – Structures Discourage Prospective Acquirors—Private buyers strongly prefer 100% ownership Mack-Cali’s Rockpoint JV prevents shareholders from fully realizing the benefits of its residential development platform

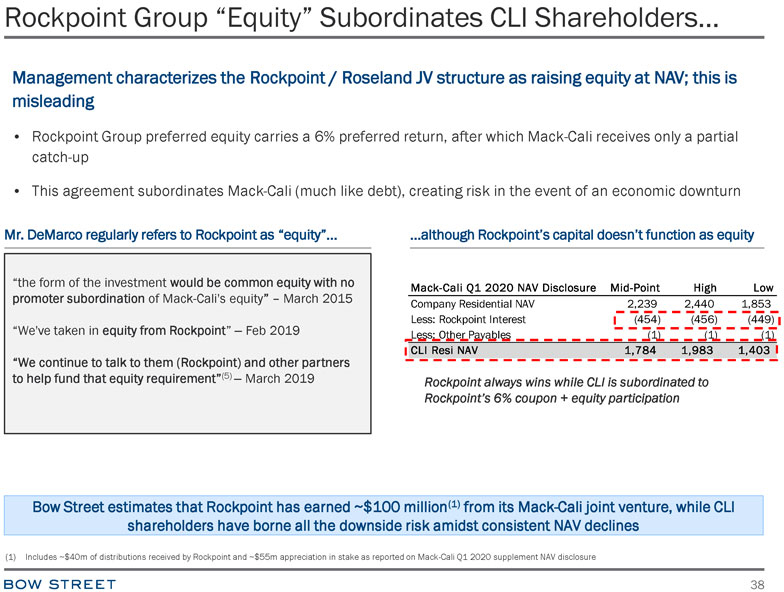

Rockpoint Group “Equity” Subordinates CLI Shareholders… Management characterizes the Rockpoint / Roseland JV structure as raising equity at NAV; this is misleading • Rockpoint Group preferred equity carries a 6% preferred return, after which Mack-Cali receives only a partial catch-up • This agreement subordinates Mack-Cali (much like debt), creating risk in the event of an economic downturn Mr. DeMarco regularly refers to Rockpoint as “equity”… …although Rockpoint’s capital doesn’t function as equity “the form of the investment would be common equity with no Mack-Cali Q1 2020 NAV Disclosure Mid-Point High Low promoter subordination of Mack-Cali’s equity” – March 2015 Company Residential NAV 2,239 2,440 1,853 “We’ve taken in equity from Rockpoint” – Feb 2019 Less: Rockpoint Interest (454) (456) (449) Less: Other Payables (1) (1) (1) CLI Resi NAV 1,784 1,983 1,403 “We continue to talk to them (Rockpoint) and other partners to help fund that equity requirement” (5) – March 2019 Rockpoint always wins while CLI is subordinated to Rockpoint’s 6% coupon + equity participation Bow Street estimates that Rockpoint has earned ~$100 million(1) from its Mack-Cali joint venture, while CLI shareholders have borne all the downside risk amidst consistent NAV declines

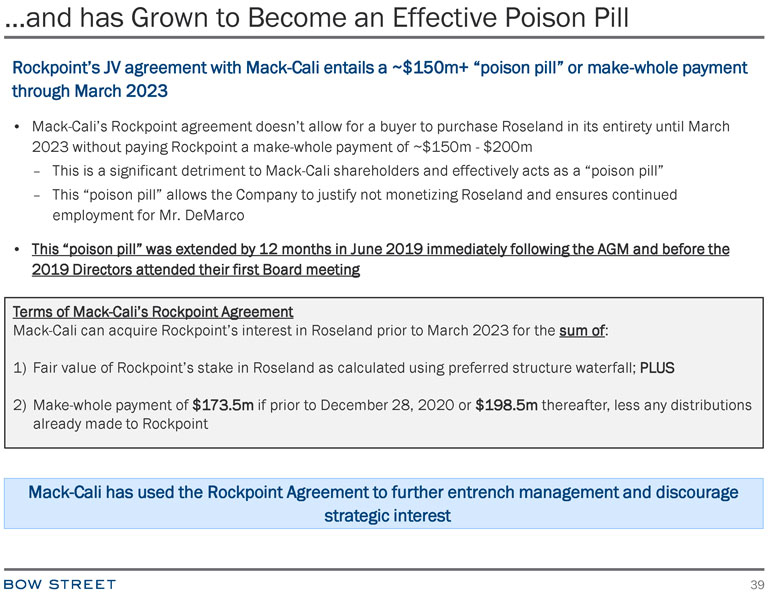

…and has Grown to Become an Effective Poison Pill Rockpoint’s JV agreement with Mack-Cali entails a ~$150m+ “poison pill” or make-whole payment through March 2023 • Mack-Cali’s Rockpoint agreement doesn’t allow for a buyer to purchase Roseland in its entirety until March 2023 without paying Rockpoint a make-whole payment of ~$150m—$200m – This is a significant detriment to Mack-Cali shareholders and effectively acts as a “poison pill” – This “poison pill” allows the Company to justify not monetizing Roseland and ensures continued employment for Mr. DeMarco • This “poison pill” was extended by 12 months in June 2019 immediately following the AGM and before the 2019 Directors attended their first Board meeting Terms of Mack-Cali’s Rockpoint Agreement Mack-Cali can acquire Rockpoint’s interest in Roseland prior to March 2023 for the sum of: 1) Fair value of Rockpoint’s stake in Roseland as calculated using preferred structure waterfall; PLUS 2) Make-whole payment of $173.5m if prior to December 28, 2020 or $198.5m thereafter, less any distributions already made to Rockpoint Mack-Cali has used the Rockpoint Agreement to further entrench management and discourage strategic interest

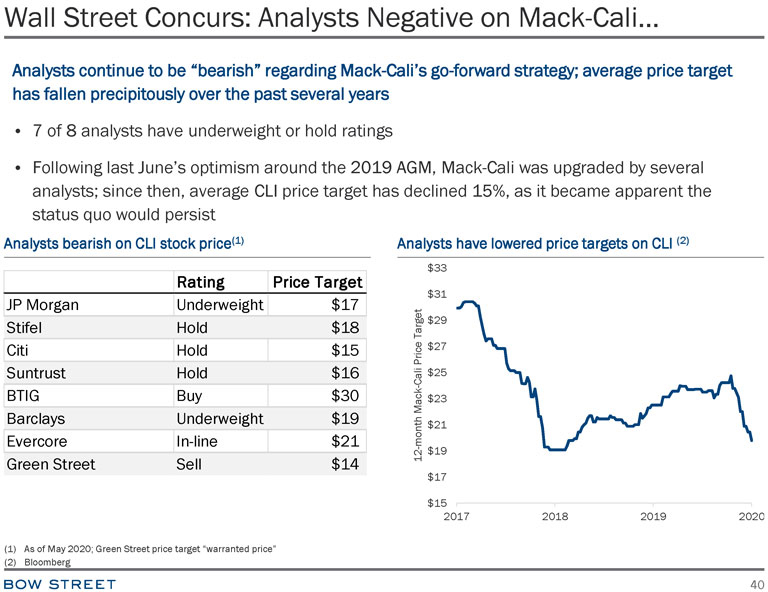

Wall Street Concurs: Analysts Negative on Mack-Cali… Analysts continue to be “bearish” regarding Mack-Cali’s go-forward strategy; average price target has fallen precipitously over the past several years • 7 of 8 analysts have underweight or hold ratings • Following last June’s optimism around the 2019 AGM, Mack-Cali was upgraded by several analysts; since then, average CLI price target has declined 15%, as it became apparent the status quo would persist Analysts bearish on CLI stock price(1) Analysts have lowered price targets on CLI (2) Rating Price Target JP Morgan Underweight $17 Stifel Hold $18 Citi Hold $15 Suntrust Hold $16 BTIG Buy $30 Barclays Underweight $19 Evercore In-line $21 Green Street Sell $14 (1) As of May 2020; Green Street price target “warranted price”

…Concerned About Leverage, Strategy and Execution “Bow Street (activist shareholder) leaned into its view that the legacy board and CEO of CLI should be replaced. Its press release outlined its view of the path forward that included simplifying further, de-leveraging, and reducing development exposure. We agree with all these things” 5/7/2020 “We rate shares of CLI Underweight…We chose a discount rate that is well above the average we use for most REITs due to the inherent risks with CLI’s (1) above-average leverage, (2) leasing risks, (3) ongoing portfolio repositioning, and (4) development exposure” 2/20/2020 “high leverage is here to stay… the office plus multifamily plus highly levered balance sheet is a trifecta unlikely to be endorsed by long term investors” 1/6/2020 “At over 9x net debt/EBITDA, leverage is still too high…the most difficult to understand REIT we cover” 4/8/2020 “(1) leasing activity continued to be light… (2) leverage remains high at almost 10x net debt/EBITDA… (3) dividend maintained at $0.80/sh but overfunded, (4) G&A remains high” 2/26/2020 “Earnings have fallen materially every single quarter for the past two and a half years” 5/6/2020 “We do not believe CLI is an FFO story, but it has also become increasingly difficult to have faith in whatever story it is. Management again pointed to leasing and balance sheet management as the focus for 2020” 2/26/2020

A Legacy of Broken Corporate Governance

Mack-Cali was Built on a Foundation of Weak Governance… At its effective founding in 1997, Mack-Cali’s governance was designed to benefit Chairman Bill Mack and his family; this culture – prioritizing the Board and management over other stakeholders – persists to this day • Mack Family advantaged at common shareholders’ expense – Since inception, Company’s “Mack Agreement” allowed Mack Family disproportionate Board representation and tax protection at shareholders’ expense; Bill Mack’s conflicts went unchecked, as he and his family attained enormous wealth while Mack-Cali shareholders have seen no return on their investment • History of rebuffing strategic interest – Mack-Cali has been repeatedly reported to reject strategic approaches from interested suitors • “Independent” Board in name only – at the time of last year’s proxy contest, 7 of 11 Mack-Cali directors had served for over 15+ years; Bow Street sought to replace four directors with a combined 86 years of service; • History of shareholder unfriendly governance policies – Mack-Cali has long had governance unfriendly policies in place, including requirement of unanimous written consent for shareholder meeting, high threshold required for shareholders to call special meetings, high bar for director removal, and sole power to increase size of board and fill director vacancies

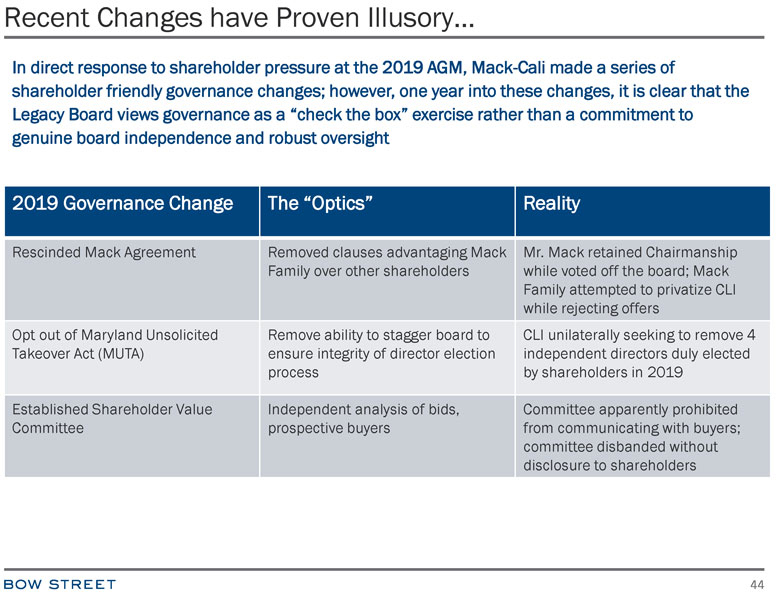

Recent Changes have Proven Illusory… In direct response to shareholder pressure at the 2019 AGM, Mack-Cali made a series of shareholder friendly governance changes; however, one year into these changes, it is clear that the Legacy Board views governance as a “check the box” exercise rather than a commitment to genuine board independence and robust oversight 2019 Governance Change The “Optics” Reality Rescinded Mack Agreement Removed clauses advantaging Mack Mr. Mack retained Chairmanship Family over other shareholders while voted off the board; Mack Family attempted to privatize CLI while rejecting offers Opt out of Maryland Unsolicited Remove ability to stagger board to CLI unilaterally seeking to remove 4 Takeover Act (MUTA) ensure integrity of director election independent directors duly elected process by shareholders in 2019 Established Shareholder Value Independent analysis of bids, Committee apparently prohibited Committee prospective buyers from communicating with buyers; committee disbanded without disclosure to shareholders

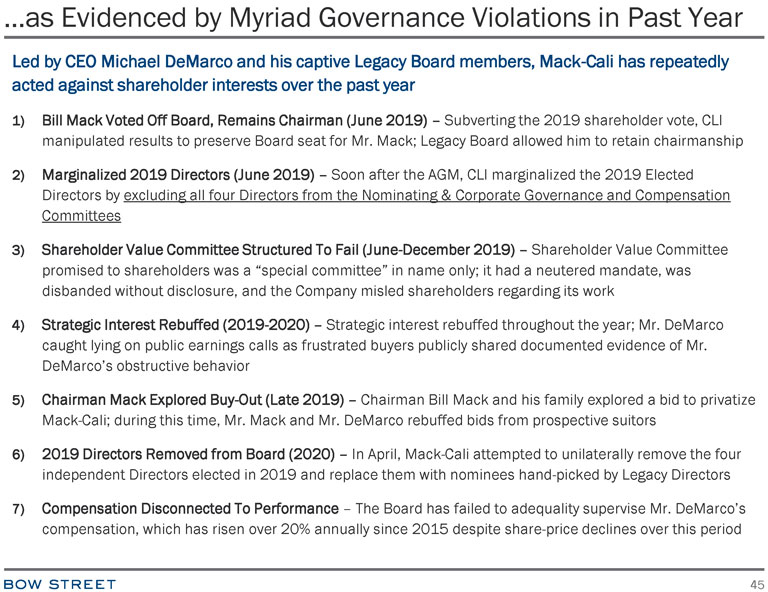

…as Evidenced by Myriad Governance Violations in Past Year Led by CEO Michael DeMarco and his captive Legacy Board members, Mack-Cali has repeatedly acted against shareholder interests over the past year 1) Bill Mack Voted Off Board, Remains Chairman (June 2019) – Subverting the 2019 shareholder vote, CLI manipulated results to preserve Board seat for Mr. Mack; Legacy Board allowed him to retain chairmanship 2) Marginalized 2019 Directors (June 2019) – Soon after the AGM, CLI marginalized the 2019 Elected Directors by excluding all four Directors from the Nominating & Corporate Governance and Compensation Committees 3) Shareholder Value Committee Structured To Fail (June-December 2019) – Shareholder Value Committee promised to shareholders was a “special committee” in name only; it had a neutered mandate, was disbanded without disclosure, and the Company misled shareholders regarding its work 4) Strategic Interest Rebuffed (2019-2020) – Strategic interest rebuffed throughout the year; Mr. DeMarco caught lying on public earnings calls as frustrated buyers publicly shared documented evidence of Mr. DeMarco’s obstructive behavior 5) Chairman Mack Explored Buy-Out (Late 2019) – Chairman Bill Mack and his family explored a bid to privatize Mack-Cali; during this time, Mr. Mack and Mr. DeMarco rebuffed bids from prospective suitors 6) 2019 Directors Removed from Board (2020) – In April, Mack-Cali attempted to unilaterally remove the four independent Directors elected in 2019 and replace them with nominees hand-picked by Legacy Directors 7) Compensation Disconnected To Performance – The Board has failed to adequality supervise Mr. DeMarco’s compensation, which has risen over 20% annually since 2015 despite share-price declines over this period

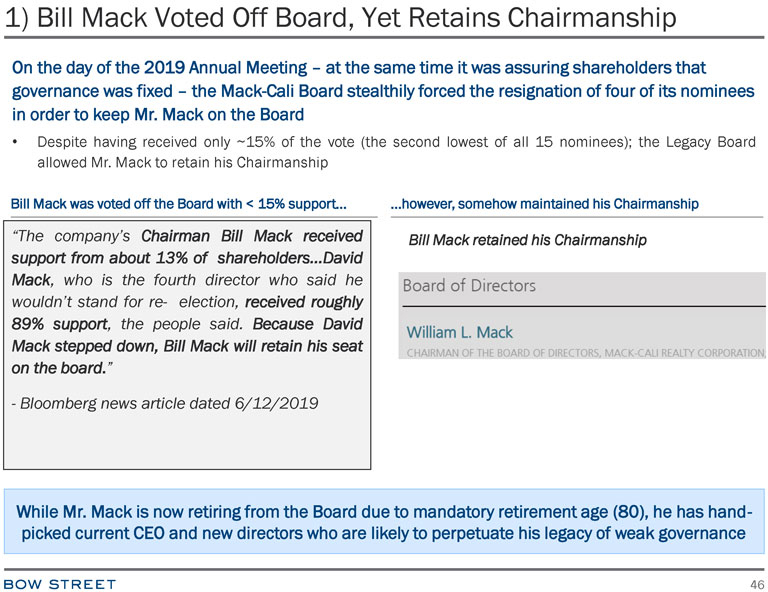

1) Bill Mack Voted Off Board, Yet Retains Chairmanship On the day of the 2019 Annual Meeting – at the same time it was assuring shareholders that governance was fixed – the Mack-Cali Board stealthily forced the resignation of four of its nominees in order to keep Mr. Mack on the Board • Despite having received only ~15% of the vote (the second lowest of all 15 nominees); the Legacy Board allowed Mr. Mack to retain his Chairmanship Bill Mack was voted off the Board with < 15% support… …however, somehow maintained his Chairmanship “The company’s Chairman Bill Mack received Bill Mack retained his Chairmanship support from about 13% of shareholders…David Mack, who is the fourth director who said he wouldn’t stand for re- election, received roughly 89% support, the people said. Because David Mack stepped down, Bill Mack will retain his seat on the board.” - Bloomberg news article dated 6/12/2019 While Mr. Mack is now retiring from the Board due to mandatory retirement age (80), he has hand-picked current CEO and new directors who are likely to perpetuate his legacy of weak governance

2) 2019 Directors: Marginalized by Committee Despite promises of constructive engagement, the Legacy Directors marginalized the 2019 Directors by limiting committee roles and excluding them from key committees such as Nominating & Governance, and Compensation Nominating & Corp. Gov Committee – No 2019 Directors Irvin Reid (Chairperson) – 26 Year Legacy Director Alan Bernikow – 14 Year Legacy Director Laura Pomerantz – Mack family loyalist Rebecca Robertson –Personal ties to Mack family NCG Sub-Committee Director Selection – No 2019 Directors Irvin Reid – 26 Year Legacy Director 2019 Directors had no voice on Laura Pomerantz – Mack family loyalist Michael DeMarco—CEO CEO Chooses own Directors committees that oversaw Board Annual Meeting Committee – No 2019 Directors selection, governance, or compensation All Directors except 2019 Directors Executive Compensation Committee – No 2019 Directors Lisa Myers – (Chairperson) Laura Pomerantz – Mack family loyalist Audit Committee – Four 2019 Directors Irvin Reid – 26 Year Legacy Director Rebecca Robertson – Personal ties to Mack family Alan Bernikow (Chairperson) – 14 Year Legacy Director Alan Batkin – 2019 Director Frederic Cumenal – 2019 Director MaryAnne Gilmartin – 2019 Director Nori Gerado Lietz – 2019 Director Would a Board genuinely interested in independence fail to include all of 2019 Directors on the committees responsible for executive compensation, Board composition and corporate governance?

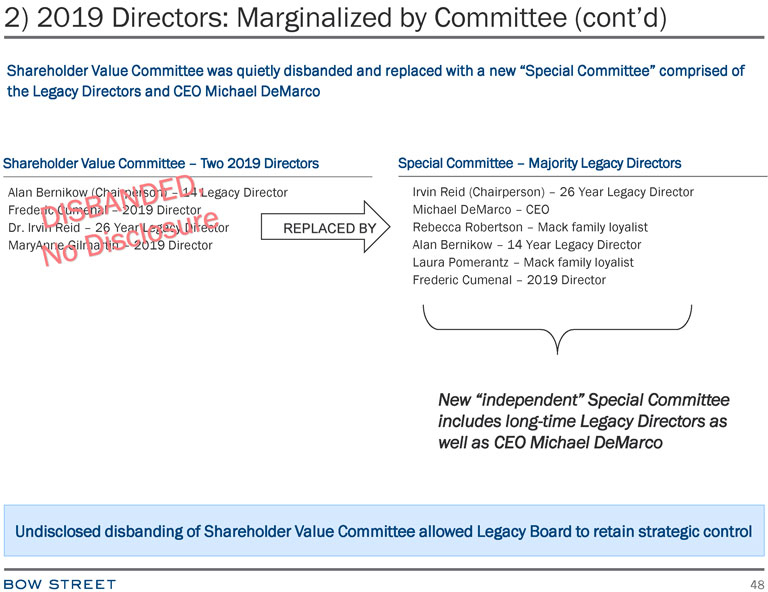

2) 2019 Directors: Marginalized by Committee (cont’d) Shareholder Value Committee was quietly disbanded and replaced with a new “Special Committee” comprised of the Legacy Directors and CEO Michael DeMarco S 2019 Directors Special Committee – Majority Legacy Directors A Director Irvin Reid (Chairperson) – 26 Year Legacy Director Michael DeMarco – CEO D REPLACED BY Rebecca Robertson – Mack family loyalist Alan Bernikow – 14 Year Legacy Director Laura Pomerantz – Mack family loyalist Frederic Cumenal – 2019 Director New “independent” Special Committee includes long-time Legacy Directors as well as CEO Michael DeMarco Undisclosed disbanding of Shareholder Value Committee allowed Legacy Board to retain strategic control

3) Shareholder Value Committee had no Authority… Shareholder Value Committee established by the Legacy Board was designed to fail • Despite broad shareholder support for a robust and transparent strategic alternatives process intended to provide shareholders and the Board with prospective bids for all or part of the Company, the Shareholder Value Committee was expressly prohibited from: 1. Contacting or having any discussions with prospective bidders 2. Having any discussions with Bow Street, even though Bow Street had been approached by numerous buyers expressing an interest in the Company 3. Communicating in any way with shareholders to solicit input regarding the Company’s strategy • Further, despite requests from Bow Street to hear directly from the committee, its conclusions were never released to shareholders • This committee was apparently disbanded with no disclosure to the market, replaced with a committee comprised of Mr. DeMarco and a majority of Directors not nominated by shareholders Why would the Company establish a committee with no chance of actually achieving its stated outcome? • If the committee had been allowed to speak to the same prospective buyers that contacted Bow Street, we believe that they would have been forced to address Wholeco bids in the $24-28/sh range (a premium of 90% to where the Company’s stock is currently trading(1)). Evidently, management determined this was not in Mack-Cali’s best interests Legacy Board mandated that all strategic interest in the Company be directed to Mr. DeMarco, despite his clearly expressed desire and incentive not to sell

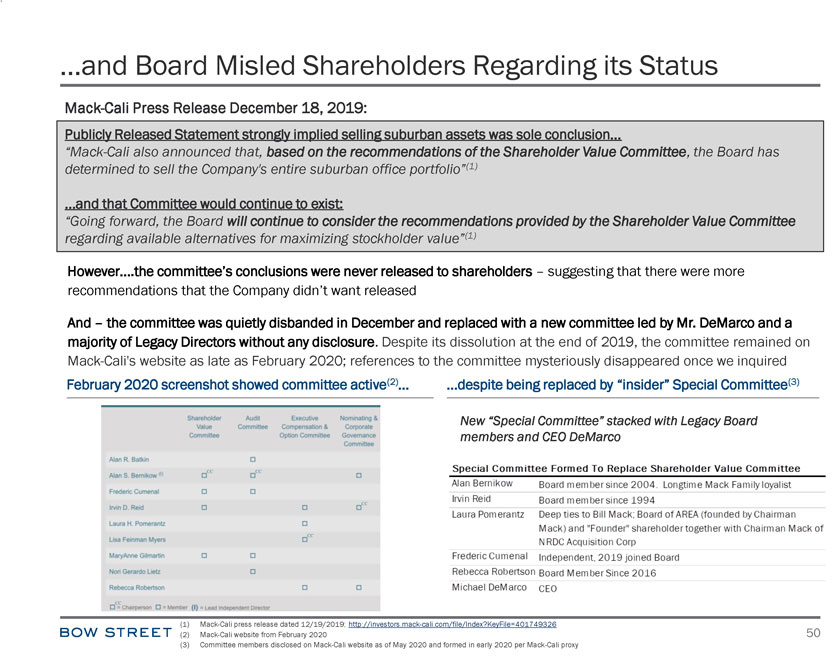

…and Board Misled Shareholders Regarding its Status Mack-Cali Press Release December 18, 2019: Publicly Released Statement strongly implied selling suburban assets was sole conclusion… “Mack-Cali also announced that, based on the recommendations of the Shareholder Value Committee, the Board has determined to sell the Company’s entire suburban office portfolio”(1) …and that Committee would continue to exist: “Going forward, the Board will continue to consider the recommendations provided by the Shareholder Value Committee regarding available alternatives for maximizing stockholder value”(1) However….the committee’s conclusions were never released to shareholders – suggesting that there were more recommendations that the Company didn’t want released And – the committee was quietly disbanded in December and replaced with a new committee led by Mr. DeMarco and a majority of Legacy Directors without any disclosure. Despite its dissolution at the end of 2019, the committee remained on Mack-Cali’s website as late as February 2020; references to the committee mysteriously disappeared once we inquired February 2020 screenshot showed committee active(2)… …despite being replaced by “insider” Special Committee(3) New “Special Committee” stacked with Legacy Board members and CEO DeMarco

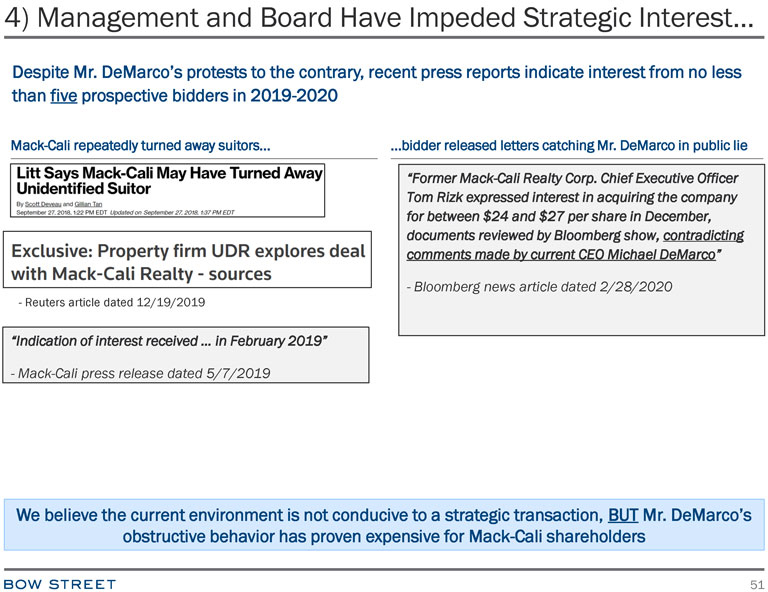

4) Management and Board Have Impeded Strategic Interest… Despite Mr. DeMarco’s protests to the contrary, recent press reports indicate interest from no less than five prospective bidders in 2019-2020 Mack-Cali repeatedly turned away suitors… …bidder released letters catching Mr. DeMarco in public lie “Former Mack-Cali Realty Corp. Chief Executive Officer Tom Rizk expressed interest in acquiring the company for between $24 and $27 per share in December, documents reviewed by Bloomberg show, contradicting comments made by current CEO Michael DeMarco” - Bloomberg news article dated 2/28/2020 - Reuters article dated 12/19/2019 “Indication of interest received … in February 2019” - Mack-Cali press release dated 5/7/2019 We believe the current environment is not conducive to a strategic transaction, BUT Mr. DeMarco’s obstructive behavior has proven expensive for Mack-Cali shareholders

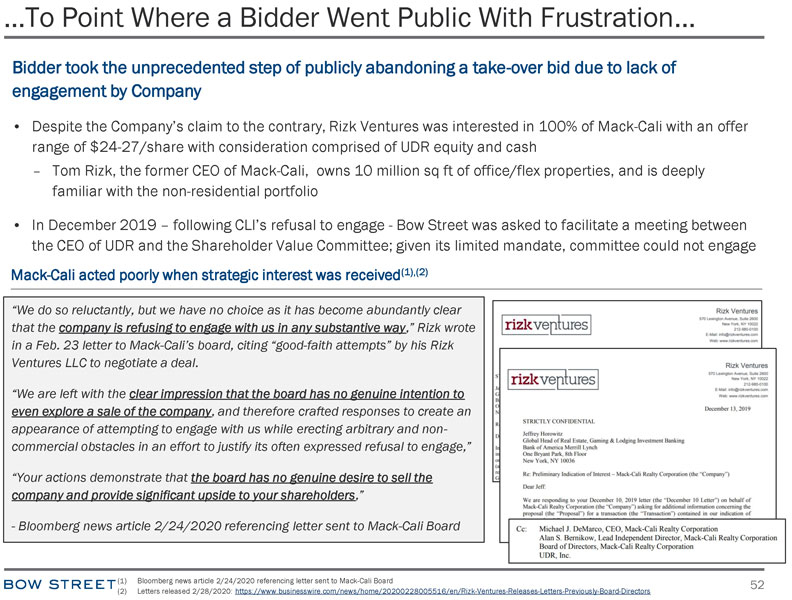

…To Point Where a Bidder Went Public With Frustration… Bidder took the unprecedented step of publicly abandoning a take-over bid due to lack of engagement by Company • Despite the Company’s claim to the contrary, Rizk Ventures was interested in 100% of Mack-Cali with an offer range of $24-27/share with consideration comprised of UDR equity and cash – Tom Rizk, the former CEO of Mack-Cali, owns 10 million sq ft of office/flex properties, and is deeply familiar with the non-residential portfolio • In December 2019 – following CLI’s refusal to engage—Bow Street was asked to facilitate a meeting between the CEO of UDR and the Shareholder Value Committee; given its limited mandate, committee could not engage Mack-Cali acted poorly when strategic interest was received (1),(2) “We do so reluctantly, but we have no choice as it has become abundantly clear that the company is refusing to engage with us in any substantive way,” Rizk wrote in a Feb. 23 letter to Mack-Cali’s board, citing “good-faith attempts” by his Rizk Ventures LLC to negotiate a deal. “We are left with the clear impression that the board has no genuine intention to even explore a sale of the company, and therefore crafted responses to create an appearance of attempting to engage with us while erecting arbitrary and noncommercial obstacles in an effort to justify its often expressed refusal to engage,” “Your actions demonstrate that the board has no genuine desire to sell the company and provide significant upside to your shareholders,” - Bloomberg news article 2/24/2020 referencing letter sent to Mack-Cali Board

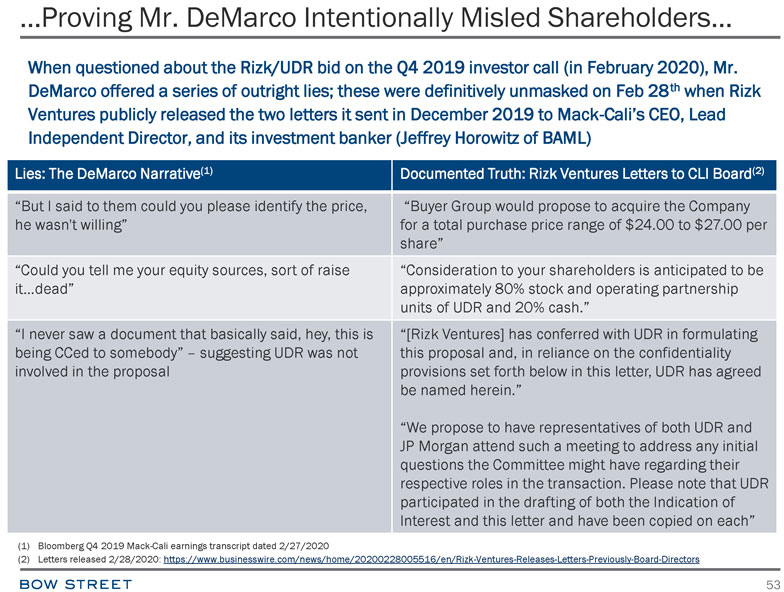

…Proving Mr. DeMarco Intentionally Misled Shareholders… When questioned about the Rizk/UDR bid on the Q4 2019 investor call (in February 2020), Mr. DeMarco offered a series of outright lies; these were definitively unmasked on Feb 28th when Rizk Ventures publicly released the two letters it sent in December 2019 to Mack-Cali’s CEO, Lead Independent Director, and its investment banker (Jeffrey Horowitz of BAML) Lies: The DeMarco Narrative(1) Documented Truth: Rizk Ventures Letters to CLI Board(2) “But I said to them could you please identify the price, “Buyer Group would propose to acquire the Company he wasn’t willing” for a total purchase price range of $24.00 to $27.00 per share” “Could you tell me your equity sources, sort of raise “Consideration to your shareholders is anticipated to be it…dead” approximately 80% stock and operating partnership units of UDR and 20% cash.” “I never saw a document that basically said, hey, this is “[Rizk Ventures] has conferred with UDR in formulating being CCed to somebody” – suggesting UDR was not this proposal and, in reliance on the confidentiality involved in the proposal provisions set forth below in this letter, UDR has agreed be named herein.” “We propose to have representatives of both UDR and JP Morgan attend such a meeting to address any initial questions the Committee might have regarding their respective roles in the transaction. Please note that UDR participated in the drafting of both the Indication of Interest and this letter and have been copied on each”

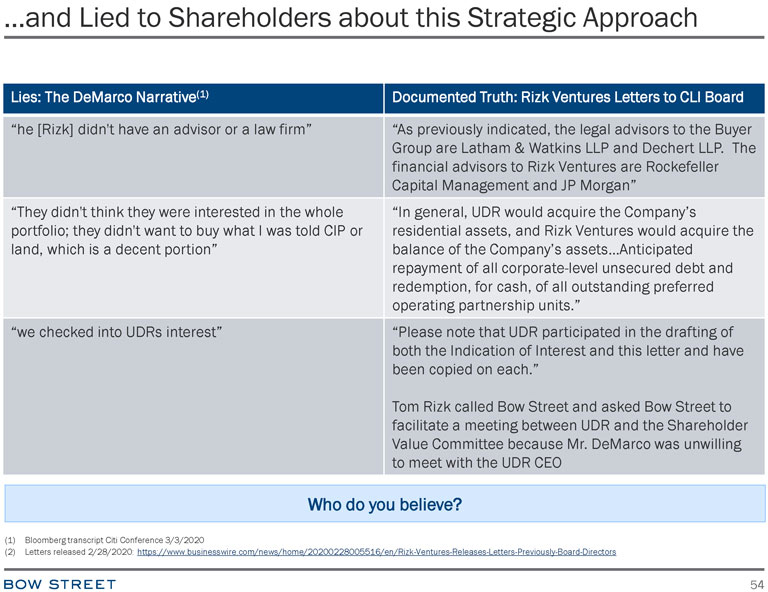

and Lied to Shareholders about this Strategic Approach Lies: The DeMarco Narrative(1) Documented Truth: Rizk Ventures Letters to CLI Board “he [Rizk] didn’t have an advisor or a law firm” “As previously indicated, the legal advisors to the Buyer Group are Latham & Watkins LLP and Dechert LLP. The financial advisors to Rizk Ventures are Rockefeller Capital Management and JP Morgan” “They didn’t think they were interested in the whole “In general, UDR would acquire the Company’s portfolio; they didn’t want to buy what I was told CIP or residential assets, and Rizk Ventures would acquire the land, which is a decent portion” balance of the Company’s assets…Anticipated repayment of all corporate-level unsecured debt and redemption, for cash, of all outstanding preferred operating partnership units.” “we checked into UDRs interest” “Please note that UDR participated in the drafting of both the Indication of Interest and this letter and have been copied on each.” Tom Rizk called Bow Street and asked Bow Street to facilitate a meeting between UDR and the Shareholder Value Committee because Mr. DeMarco was unwilling to meet with the UDR CEO Who do you believe? (1) Bloomberg transcript Citi Conference 3/3/2020 (2) Letters released 2/28/2020: https://www.businesswire.com/news/home/20200228005516/en/Rizk-Ventures-Releases-Letters-Previously-Board-Directors

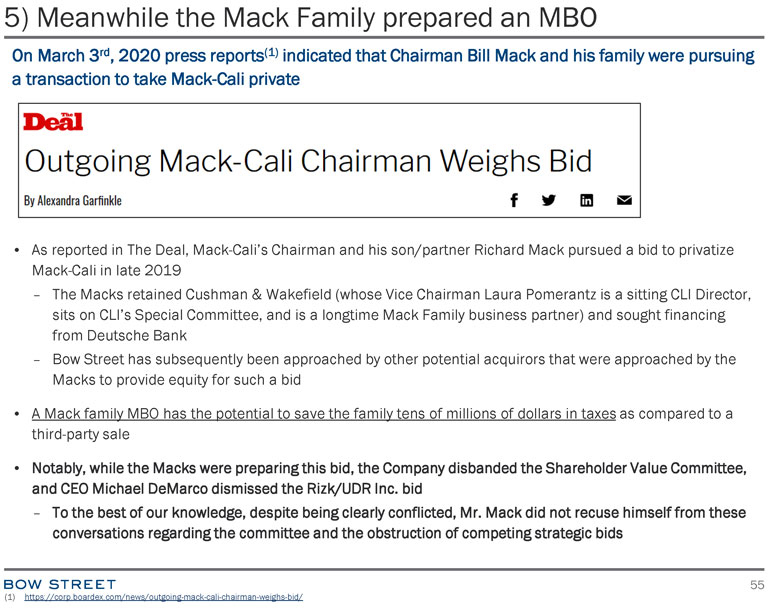

5) Meanwhile the Mack Family prepared an MBO On March 3rd, 2020 press reports(1) indicated that Chairman Bill Mack and his family were pursuing a transaction to take Mack-Cali private • As reported in The Deal, Mack-Cali’s Chairman and his son/partner Richard Mack pursued a bid to privatize Mack-Cali in late 2019 – The Macks retained Cushman & Wakefield (whose Vice Chairman Laura Pomerantz is a sitting CLI Director, sits on CLI’s Special Committee, and is a longtime Mack Family business partner) and sought financing from Deutsche Bank – Bow Street has subsequently been approached by other potential acquirors that were approached by the Macks to provide equity for such a bid • A Mack family MBO has the potential to save the family tens of millions of dollars in taxesas compared to a third-party sale • Notably, while the Macks were preparing this bid, the Company disbanded the Shareholder Value Committee, and CEO Michael DeMarco dismissed the Rizk/UDR Inc. bid – To the best of our knowledge, despite being clearly conflicted, Mr. Mack did not recuse himself from these conversations regarding the committee and the obstruction of competing strategic bids

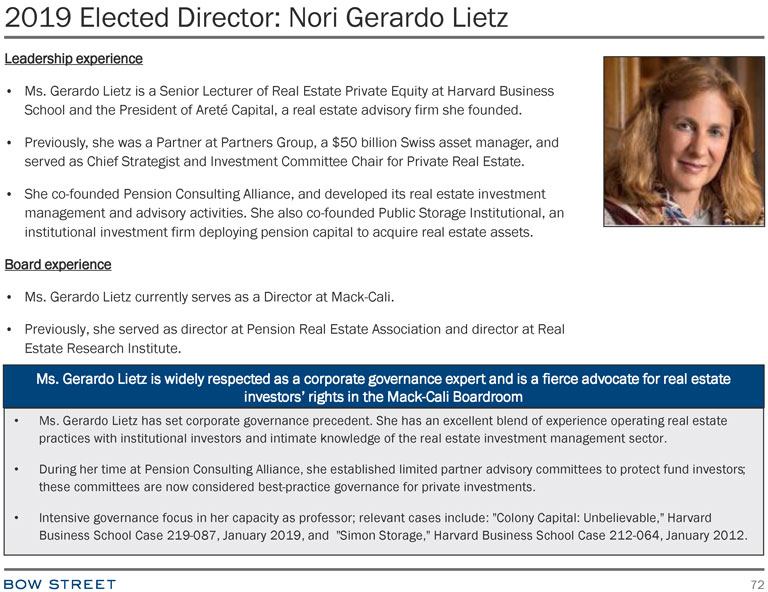

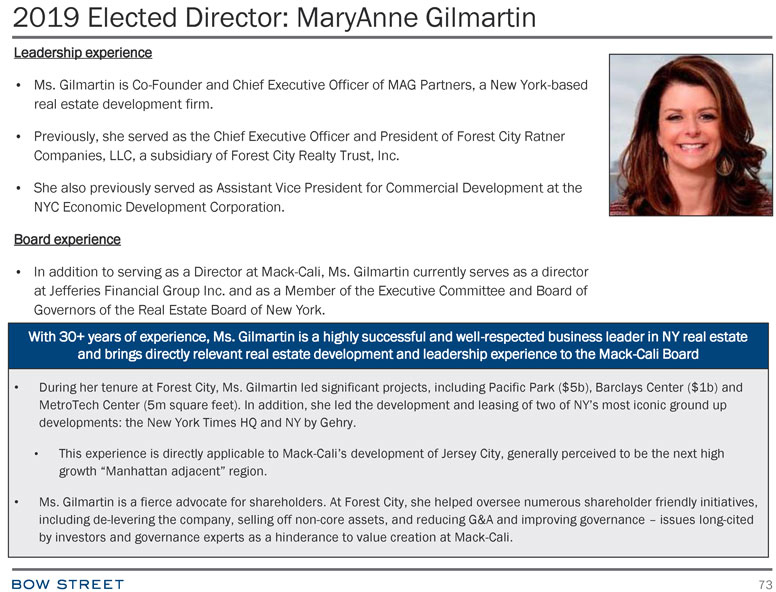

6) 2019 Directors Marginalized, Then Removed Board is Subverting Shareholders’ 2019 vote by refusing to re-nominate four independent 2019 directors • Despite the overwhelming support these directors received at the 2019 AGM, the Company has refused to renominate MaryAnne Gilmartin, Frederic Cumenal, Nori Gerado Lietz and Alan Batkin in 2020 • Bow Street included these directors on its slate due to a concern that the Company would force their resignation (as they did with four directors last year to protect Chairman Bill Mack) in order to protect the Legacy Directors • Mack-Cali established an Annual Meeting Committee, comprised of all its Directors EXCEPT the 2019 Directors listed above in order to exclude them from this process(1) – As disclosed April 6, Bow Street offered to exclude these four nominees from Bow Street’s slate if Mack-Cali committed to allow shareholders to vote on these nominees as part of the Company’s slate – The Company refused to commit not to amend their proxy card at the 11th hour as they did in 2019 In its proxy, Mack-Cali notes that Bow Street rejected a settlement offer: • This “settlement” proposal consisted of an offer to include three of the four 2019 Directors on the Company’s slate, in exchange for Bow Street’s agreement to drop its proxy contest. Specifically, Mack-Cali is attempting to exclude Ms. Nori Gerardo Lietz – a widely recognized expert for corporate governance at Harvard Business School who has committed her professional career to shareholder rights at real estate companies Why would a Company with a stated commitment to best-in-class governance play games with its proxy card and refuse to re-nominate Directors with impeccable corporate credentials?

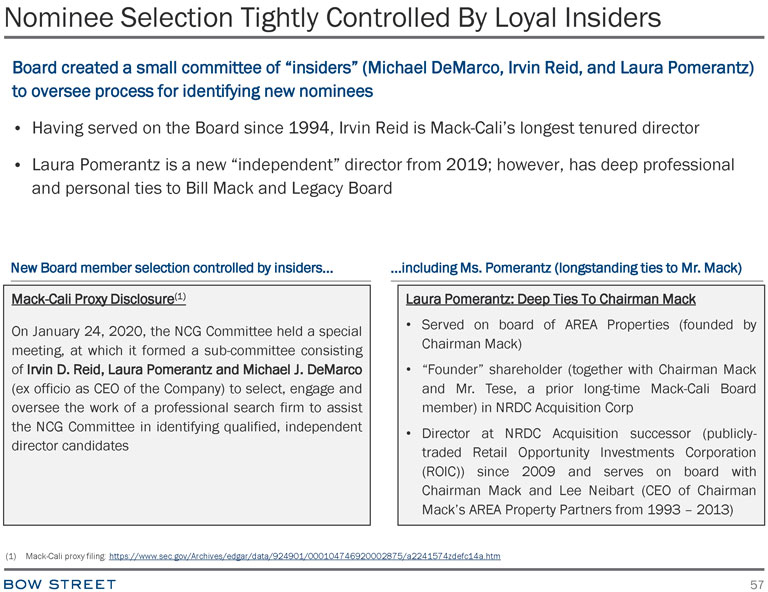

Nominee Selection Tightly Controlled By Loyal Insiders Board created a small committee of “insiders” (Michael DeMarco, Irvin Reid, and Laura Pomerantz) to oversee process for identifying new nominees • Having served on the Board since 1994, Irvin Reid is Mack-Cali’s longest tenured director • Laura Pomerantz is a new “independent” director from 2019; however, has deep professional and personal ties to Bill Mack and Legacy Board New Board member selection controlled by insiders… …including Ms. Pomerantz (longstanding ties to Mr. Mack) Mack-Cali Proxy Disclosure(1) Laura Pomerantz: Deep Ties To Chairman Mack • Served on board of AREA Properties (founded by On January 24, 2020, the NCG Committee held a special Chairman Mack) meeting, at which it formed a sub-committee consisting of Irvin D. Reid, Laura Pomerantz and Michael J. DeMarco • “Founder” shareholder (together with Chairman Mack (ex officio as CEO of the Company) to select, engage and and Mr. Tese, a prior long-time Mack-Cali Board oversee the work of a professional search firm to assist member) in NRDC Acquisition Corp the NCG Committee in identifying qualified, independent • Director at NRDC Acquisition successor (publicly-director candidates traded Retail Opportunity Investments Corporation (ROIC)) since 2009 and serves on board with Chairman Mack and Lee Neibart (CEO of Chairman Mack’s AREA Property Partners from 1993 – 2013) (1) Mack-Cali proxy filing: https://www.sec.gov/Archives/edgar/data/924901/000104746920002875/a2241574zdefc14a.htm

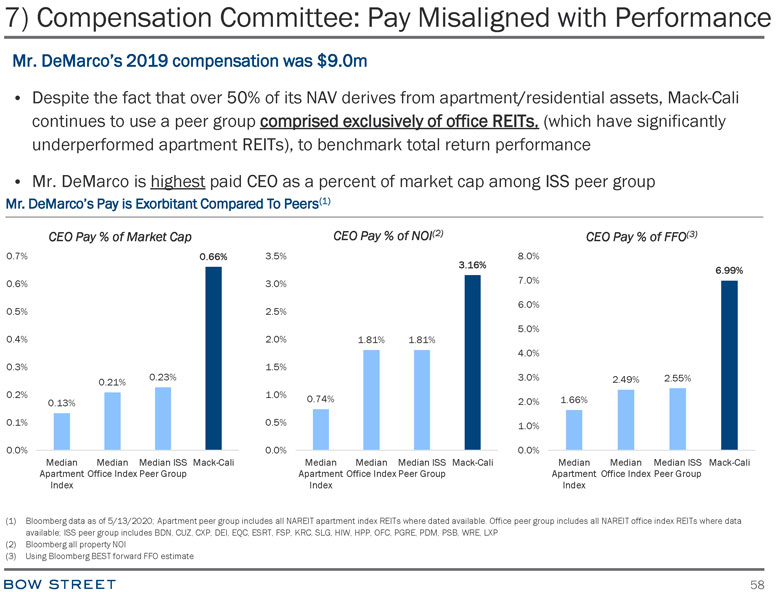

7) Compensation Committee: Pay Misaligned with Performance Mr. DeMarco’s 2019 compensation was $9.0m • Despite the fact that over 50% of its NAV derives from apartment/residential assets, Mack-Cali continues to use a peer group comprised exclusively of office REITs, (which have significantly underperformed apartment REITs), to benchmark total return performance • Mr. DeMarco is highest paid CEO as a percent of market cap among ISS peer group Mr. DeMarco’s Pay is Exorbitant Compared To Peers(1) CEO Pay % of Market Cap CEO Pay % of NOI(2) CEO Pay % of FFO(3) 0.7% 0.66% 3.5% 3.16% 8.0% 6.99% 0.6% 3.0% 7.0% 6.0% 0.5% 2.5% 5.0% 0.4% 2.0% 1.81% 1.81% 4.0% 0.3% 1.5% 0.23% 3.0% 2.49% 2.55% 0.21% 0.2% 1.0% 0.74% 0.13% 2.0% 1.66% 0.1% 0.5% 1.0% 0.0% 0.0% 0.0% Median Median Median ISS Mack-Cali Median Median Median ISS Mack-Cali Median Median Median ISS Mack-Cali Apartment Office Index Peer Group Apartment Office Index Peer Group Apartment Office Index Peer Group Index Index Index (1) Bloomberg data as of 5/13/2020; Apartment peer group includes all NAREIT apartment index REITs where dated available. Office peer group includes all NAREIT office index REITs where data available; ISS peer group includes BDN, CUZ, CXP, DEI, EQC, ESRT, FSP, KRC, SLG, HIW, HPP, OFC, PGRE, PDM, PSB, WRE, LXP (2) Bloomberg all property NOI (3) Using Bloomberg BEST forward FFO estimate

Who Should We Believe? 4 Highly Credentialed Executives… Mack-Cali has accused these four distinguished executives of being bad fiduciaries 1) Alan Batkin (previously Vice Chairman Eton Park, Kissinger Associates) – Mr. Batkin is a renowned business leader with a proven track record of success over nearly twenty-eight years of serving on public company boards, including Pattern Energy Group Inc., Omnicom Group Inc., and Cantel Medical Corporation. Mr. Batkin is the only director on the Board to purchase Mack-Cali shares in the open market 2) Frederic Cumenal (previously CEO of Tiffany & Co.) – Mr. Cumenal has significant operational, brand management and international business experience having served as the CEO of Tiffany & Co., a Fortune 500 Company 3) Nori Gerardo Lietz (Corporate Governance Expert, Senior Lecturer at Harvard Business School) Ms. Gerardo Lietz is a widely respected corporate governance expert and has written extensively on boardroom failings in the real estate sector in her capacity as a Senior Lecturer at Harvard Business School 4) MaryAnne Gilmartin (MAG Partners, Forest City) – Ms. Gilmartin is a highly successful real estate executive, who currently serves as the CEO of her own real estate development firm, MAG Partners. She has served with distinction on the board of Jefferies Financial Group Inc., and ably led major development projects as CEO and President of Forest City Ratner Companies, LLC

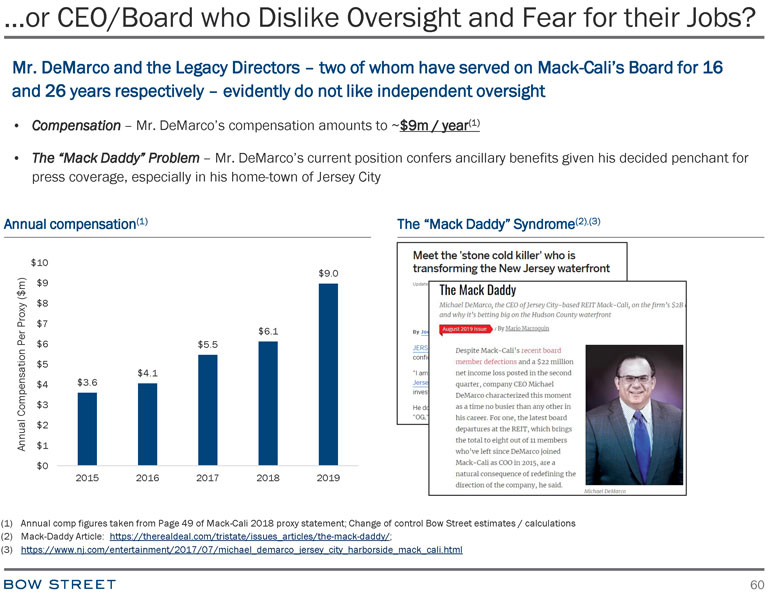

…or CEO/Board who Dislike Oversight and Fear for their Jobs? Mr. DeMarco and the Legacy Directors – two of whom have served on Mack-Cali’s Board for 16 and 26 years respectively – evidently do not like independent oversight • Compensation – Mr. DeMarco’s compensation amounts to ~$9m / year(1) • The “Mack Daddy” Problem – Mr. DeMarco’s current position confers ancillary benefits given his decided penchant for press coverage, especially in his home-town of Jersey City Annual compensation(1) The “Mack Daddy” Syndrome(2),(3) $10 $9 $9.0 $ m) ( $8 Proxy $7 Per $6.1 $6 $5.5 $5 $4.1 $4 $3.6 Compensation $3 nnual $2 A $1 $0 2015 2016 2017 2018 2019 (1) Annual comp figures taken from Page 49 of Mack-Cali 2018 proxy statement; Change of control Bow Street estimates / calculations (2) Mack-Daddy Article: https://therealdeal.com/tristate/issues_articles/the-mack-daddy/; (3) https://www.nj.com/entertainment/2017/07/michael_demarco_jersey_city_harborside_mack_cali.html

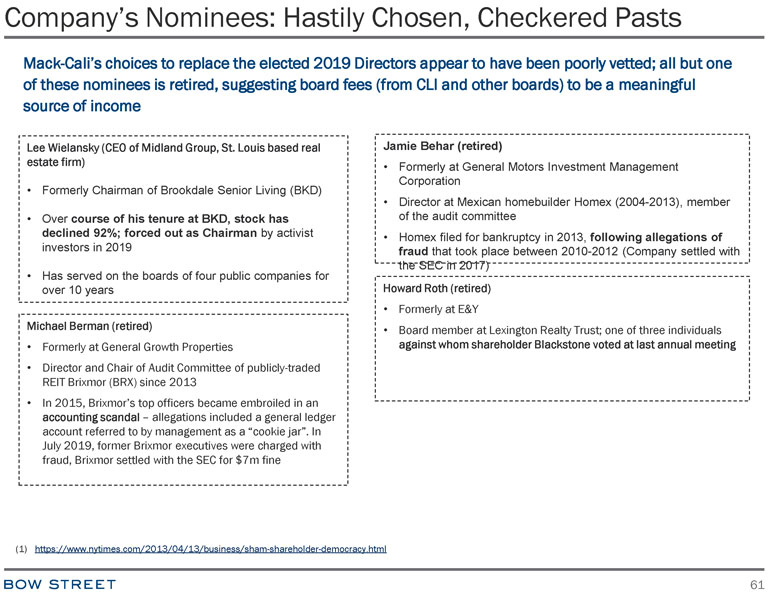

Company’s Nominees: Hastily Chosen, Checkered Pasts Mack-Cali’s choices to replace the elected 2019 Directors appear to have been poorly vetted; all but one of these nominees is retired, suggesting board fees (from CLI and other boards) to be a meaningful source of income Lee Wielansky (CEO of Midland Group, St. Louis based real Jamie Behar (retired) estate firm) • Formerly at General Motors Investment Management Corporation • Formerly Chairman of Brookdale Senior Living (BKD) • Director at Mexican homebuilder Homex (2004-2013), member • Over course of his tenure at BKD, stock has of the audit committee declined 92%; forced out as Chairman by activist • Homex filed for bankruptcy in 2013, following allegations of investors in 2019 fraud that took place between 2010-2012 (Company settled with • Has served on the boards of four public companies for the SEC in 2017) over 10 years Howard Roth (retired) • Formerly at E&Y Michael Berman (retired) • Board member at Lexington Realty Trust; one of three individuals • Formerly at General Growth Properties against whom shareholder Blackstone voted at last annual meeting • Director and Chair of Audit Committee of publicly-traded REIT Brixmor (BRX) since 2013 • In 2015, Brixmor’s top officers became embroiled in an accounting scandal – allegations included a general ledger account referred to by management as a “cookie jar”. In July 2019, former Brixmor executives were charged with fraud, Brixmor settled with the SEC for $7m fine (1) https://www.nytimes.com/2013/04/13/business/sham-shareholder-democracy.html

The Path Forward: Restoring Oversight and Accountability

The Path Forward Bow Street supports a coherent strategy for value realization led by a strong, independent Board • Despite a strong collection of assets, it is clear that Mack-Cali’s current strategy has failed to either grow NAV or close the NAV discount. Bow Street believes that in order to trade in line with peers, CLI must start looking a lot more like its peers 1) High Integrity Leadership – Mack-Cali’s current culture is toxic, benefitting management and the Legacy Directors over other stakeholders 2) Simplify Residential Platform – Residential platform should be restructured to prepare for an eventual separation of the business 3) Restructure Office Portfolio – Reposition office portfolio by selling sub-institutional suburban properties and investing in Harborside properties 4) Focus on Delivering Promised Leverage Reductions – CLI cannot expect to close the discount to its peer group while its leverage is 2x peers 5) Genuine Receptivity (as Opposed to Hostility) to Prospective Sale Proposals – Periodic assessments of capital markets to evaluate larger transactions for crystalizing shareholder value 6) Strong Independent Board and Oversight – Strategy directly overseen by strong and independent Board which holds management accountable Independent and experienced Board to provide oversight and hold management accountable

1) High Integrity Leadership 20+ years of underperformance and insider dealings at Mack-Cali have created a toxic culture where loyalty is prized over skill, and insider interests trump shareholder returns • While it is ultimately the responsibility of the new Board to identify a new CEO if necessary, we believe any new CEO must have: – Public market experience – Mack-Cali has an antagonistic relationship with sell-side analysts and its shareholders. The Company requires a CEO who can build consensus around a long-term strategy that resonates with REIT investors – High Integrity – Given the Legacy Board’s history of poor governance and current management’s tenuous relationship with the truth, we believe the new CEO needs to have unimpeachable character and ethics to build credibility with stakeholders – Keen Portfolio Management Skills – Unfortunately, Bow Street believes the near-term future is likely to remain challenged for Mack-Cali. The new CEO will require experience navigating through real estate cycles and transitioning portfolios • Bow Street has engaged with a world-leading executive search firm to explore a prospective management transition Bow Street has engaged with a leading search firm to identify prospective CEO candidates

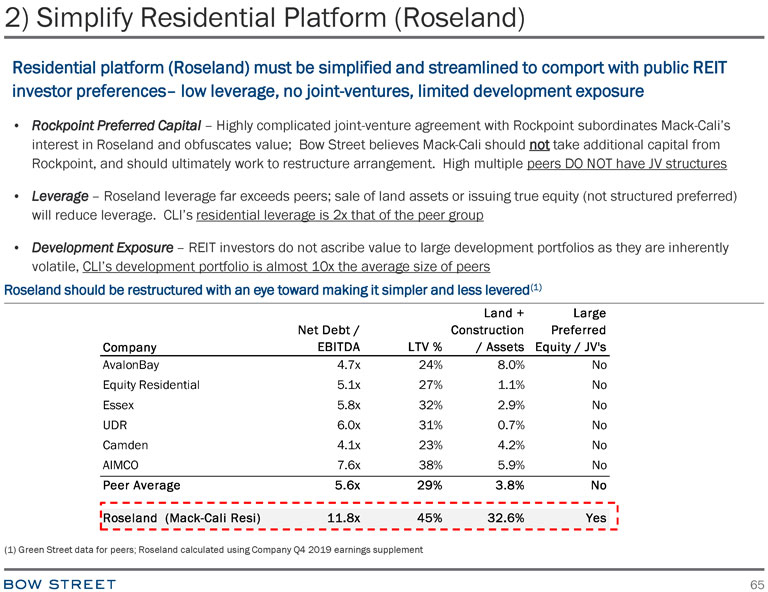

2) Simplify Residential Platform (Roseland) Residential platform (Roseland) must be simplified and streamlined to comport with public REIT investor preferences– low leverage, no joint-ventures, limited development exposure • Rockpoint Preferred Capital – Highly complicated joint-venture agreement with Rockpoint subordinates Mack-Cali’s interest in Roseland and obfuscates value; Bow Street believes Mack-Cali should not take additional capital from Rockpoint, and should ultimately work to restructure arrangement. High multiple peers DO NOT have JV structures • Leverage – Roseland leverage far exceeds peers; sale of land assets or issuing true equity (not structured preferred) will reduce leverage. CLI’s residential leverage is 2x that of the peer group • Development Exposure– REIT investors do not ascribe value to large development portfolios as they are inherently volatile, CLI’s development portfolio is almost 10x the average size of peers Roseland should be restructured with an eye toward making it simpler and less levered(1) Land + Large Net Debt / Construction Preferred Company EBITDA LTV % / Assets Equity / JV’s AvalonBay 4.7x 24% 8.0% No Equity Residential 5.1x 27% 1.1% No Essex 5.8x 32% 2.9% No UDR 6.0x 31% 0.7% No Camden 4.1x 23% 4.2% No AIMCO 7.6x 38% 5.9% No Peer Average 5.6x 29% 3.8% No Roseland (Mack-Cali Resi) 11.8x 45% 32.6% Yes (1) Green Street data for peers; Roseland calculated using Company Q4 2019 earnings supplement

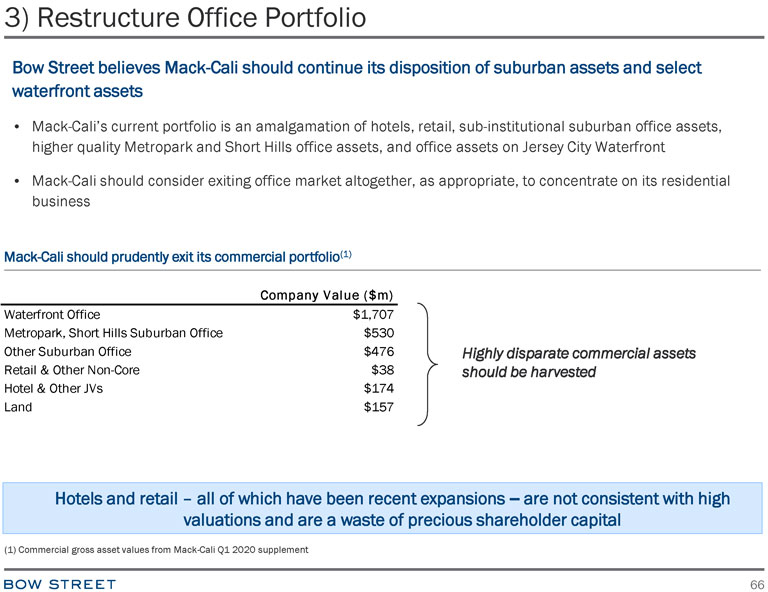

3) Restructure Office Portfolio Bow Street believes Mack-Cali should continue its disposition of suburban assets and select waterfront assets • Mack-Cali’s current portfolio is an amalgamation of hotels, retail, sub-institutional suburban office assets, higher quality Metropark and Short Hills office assets, and office assets on Jersey City Waterfront • Mack-Cali should consider exiting office market altogether, as appropriate, to concentrate on its residential business Mack-Cali should prudently exit its commercial portfolio(1) Company Value ($m) Waterfront Office $1,707 Metropark, Short Hills Suburban Office $530 Other Suburban Office $476 Highly disparate commercial assets Retail & Other Non-Core $38 should be harvested Hotel & Other JVs $174 Land $157 Hotels and retail – all of which have been recent expansions – are not consistent with high valuations and are a waste of precious shareholder capital (1) Commercial gross asset values from Mack-Cali Q1 2020 supplement

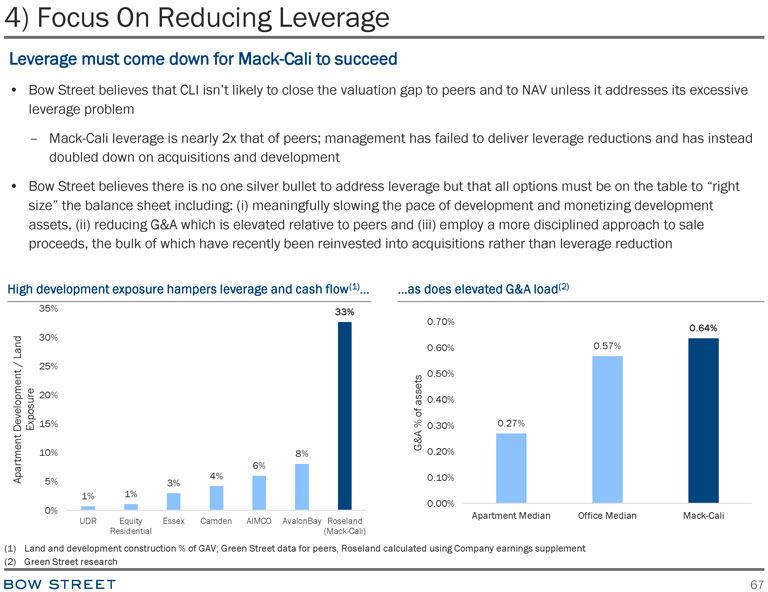

4) Focus On Reducing Leverage Leverage must come down for Mack-Cali to succeed • Bow Street believes that CLI isn’t likely to close the valuation gap to peers and to NAV unless it addresses its excessive leverage problem – Mack-Cali leverage is nearly 2x that of peers; management has failed to deliver leverage reductions and has instead doubled down on acquisitions and development • Bow Street believes there is no one silver bullet to address leverage but that all options must be on the table to “right size” the balance sheet including: (i) meaningfully slowing the pace of development and monetizing development assets, (ii) reducing G&A which is elevated relative to peers and (iii) employ a more disciplined approach to sale proceeds, the bulk of which have recently been reinvested into acquisitions rather than leverage reduction High development exposure hampers leverage and cash flow(1)… …as does elevated G&A load(2) 35% 33% 0.70% 0.64% 30% Land 0.60% 0.57% / 25% 0.50% 20% assets 0.40% of 15% % 0.30% 0.27% Development Exposure G&A 10% 8% 0.20% 6% Apartment 4% 0.10% 5% 3% 1% 1% 0.00% 0% Apartment Median Office Median Mack-Cali UDR Equity Essex Camden AIMCO AvalonBay Roseland Residential (Mack-Cali) (1) Land and development construction % of GAV; Green Street data for peers, Roseland calculated using Company earnings supplement

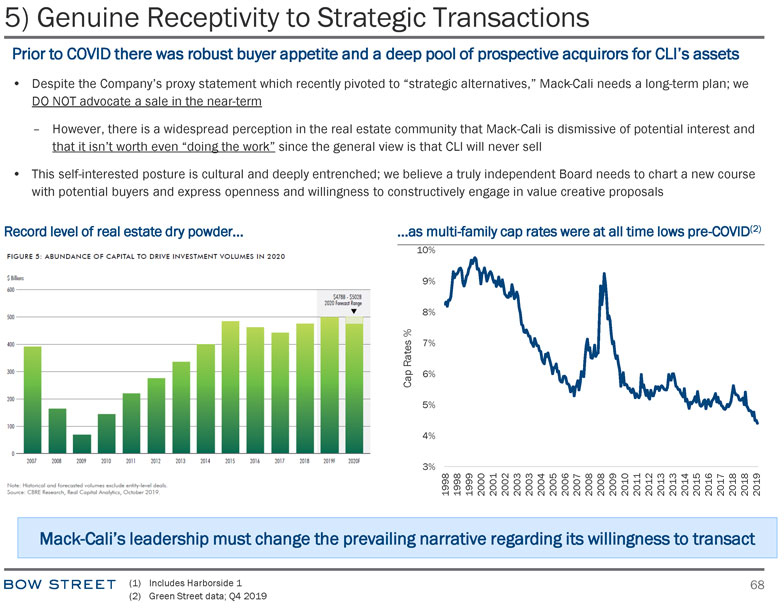

5) Genuine Receptivity to Strategic Transactions Prior to COVID there was robust buyer appetite and a deep pool of prospective acquirors for CLI’s assets • Despite the Company’s proxy statement which recently pivoted to “strategic alternatives,” Mack-Cali needs a long-term plan; we DO NOT advocate a sale in the near-term – However, there is a widespread perception in the real estate community that Mack-Cali is dismissive of potential interest and that it isn’t worth even “doing the work” since the general view is that CLI will never sell • This self-interested posture is cultural and deeply entrenched; we believe a truly independent Board needs to chart a new course with potential buyers and express openness and willingness to constructively engage in value creative proposals Record level of real estate dry powder… …as multi-family cap rates were at all time lows pre-COVID(2) 10% 9% 8% % 7% Rates Cap 6% 5% 4% 3% 1998 1998 1999 2000 2001 2002 2003 2003 2004 2005 2006 2007 2008 2008 2009 2010 2011 2012 2013 2013 2014 2015 2016 2017 2018 2018 2019 Mack-Cali’s leadership must change the prevailing narrative regarding its willingness to transact

6) Strong, Independent Board and Oversight Bow Street Board nominees bring independent oversight and experience • Bow Street believes the current CEO and Legacy Board have created a toxic environment that prioritizes insider interests and has long failed to be accountable to shareholders • We believe a meaningful refreshment of the Board, with four new independent directors – in addition to the four independent directors elected by shareholders last year – is required to change the culture in the boardroom and rid the Company of this deep entrenchment • 7 of our 8 director nominees are fully independent of Bow Street (all are independent of Mack-Cali) and bring deep CEO, real estate, public markets and governance expertise to a Board that currently values loyalty to Messrs. DeMarco and Mack over service to shareholders – Akiva Katz – the lone non-independent director nominee – will bring a shareholder mindset to the Board. Mack-Cali is a significant investment for Bow Street and Mr. Katz will invest the time and effort to ensure that the Board is well apprised of shareholder and other stakeholder perspectives, which we believe have been suppressed by current management’s bullying tone and actions • We believe a new, rigorously independent Board will create the conditions that will allow Mack-Cali’s persistent NAV discount to be closed, and will restore investor faith in Mack-Cali Without a strong, independent Board of Directors, Mack-Cali will never close its NAV discount