Exhibit 99.1

|

CITI Conference March 8, 2021 |

|

This Operating and Financial Data connection with our Annual Report the year ended December 31, 2020. should be read in on Form 10-K for Statements made in this presentation may be forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements can be identified by the use of words such as “may,” “will,” “plan,” “potential,” “projected,” “should,” “expect,” “anticipate,” “estimate,” “target,” “continue” or comparable terminology. Forward-looking statements are inherently subject to certain risks, trends and uncertainties, many of which we cannot predict with accuracy and some of which we might not even anticipate, and involve factors that may cause actual results to differ materially from those projected or suggested. Readers are cautioned not to place undue reliance on these forward-looking statements and are advised to consider the factors listed above together with the additional factors under the heading “Disclosure Regarding Forward-Looking Statements” and “Risk Factors” in our annual reports on Form 10-K, as may be supplemented or amended by our quarterly reports on Form 10-Q, which are incorporated herein by reference. We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events, new information or otherwise. 2 |

|

Simplified Business Plan to Three Executable Strategies: Complete the Sale of the Suburban Office Portfolio Establish Roseland as an Optimized Platform Revitalize Waterfront Leasing 1 2 3 a. Maximize Suburban asset value with minimal COVID discount Increase strategic flexibility of the Company’s balance sheet Establish the Company as a predominantly residential REIT a. Reposition Harborside as complete campus offering Utilize world-class team leasing professionals a a. Stabilize occupancy at operating properties Realize cash flow of fully funded development projects Capitalize on value creation from enviable development pipeline b. of b. b. c. Generate traffic with proactive leasing program c. c. 3 |

|

Complete the Sale of the Suburban Office Portfolio 1 4 |

|

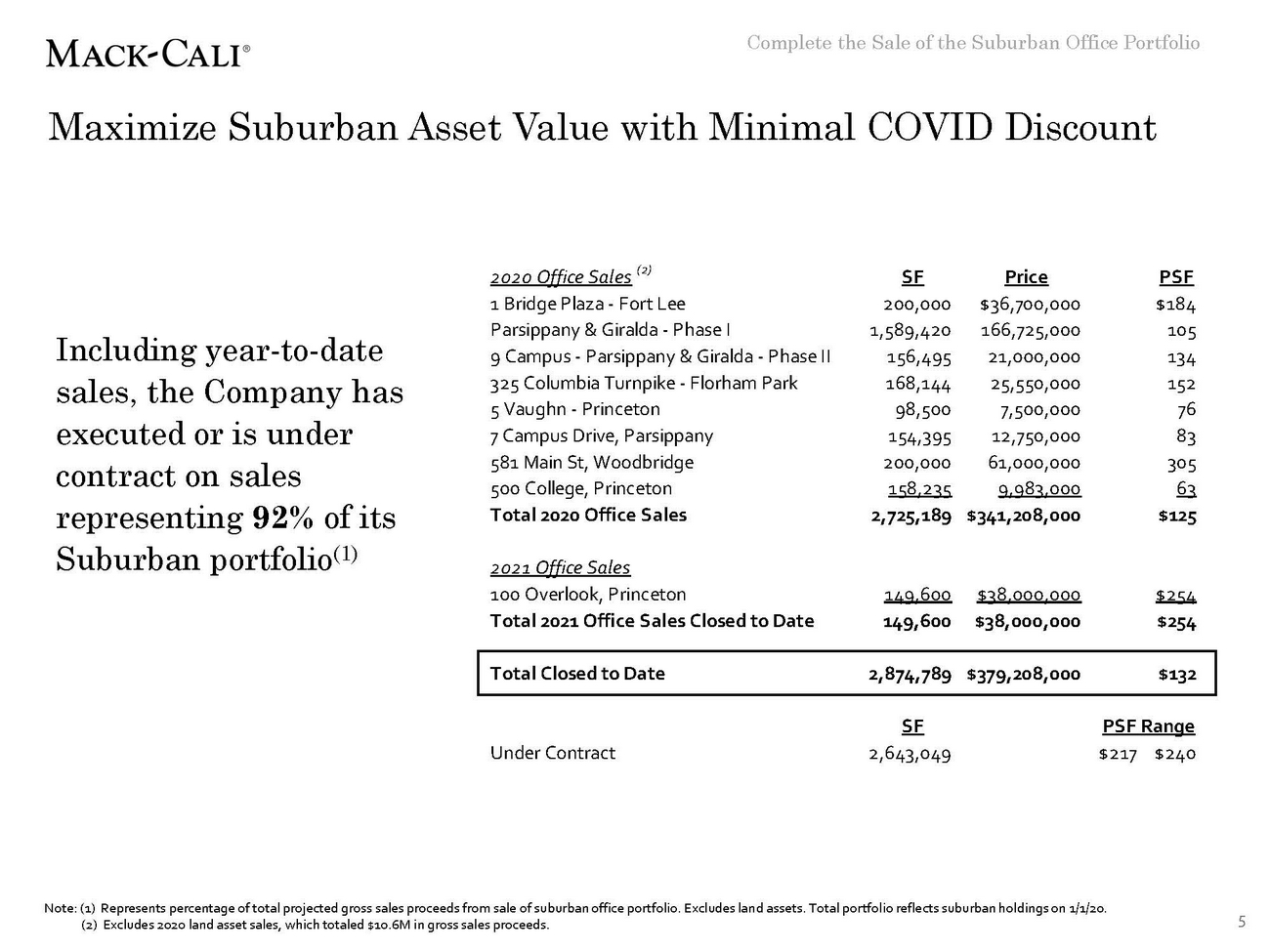

Complete the Sale of the Suburban Office Portfolio Maximize Suburban Asset Value with Minimal COVID Discount 2020 Office Sales (2) SF 200,000 1,589,420 156,495 168,144 98,500 154,395 200,000 158,235 2,725,189 Price $36,700,000 166,725,000 21,000,000 25,550,000 7,500,000 12,750,000 61,000,000 9,983,000 $341,208,000 PSF $184 105 134 152 76 83 305 63 $125 1 Bridge Plaza - Fort Lee Parsippany & Giralda - Phase I 9 Campus - Parsippany & Giralda - Phase II 325 Columbia Turnpike - Florham Park 5 Vaughn - Princeton 7 Campus Drive, Parsippany 581 Main St, Woodbridge 500 College, Princeton Total 2020 Office Sales Including year-to-date sales, the Company has executed or is under contract on sales representing 92% of its Suburban portfolio(1) 2021 Office Sales 100 Overlook, Princeton Total 2021 Office Sales Closed to Date 149,600 149,600 $38,000,000 $38,000,000 $254 $254 SF 2,643,049 PSF Range Under Contract $217 $240 Note: (1) Represents percentage of total projected gross sales proceeds from sale of suburban office portfolio. Excludes land assets. Total portfolio reflects suburban holdings on 1/1/20. (2) Excludes 2020 land asset sales, which totaled $10.6M in gross sales proceeds. 5 Total Closed to Date 2,874,789 $379,208,000 $132 |

|

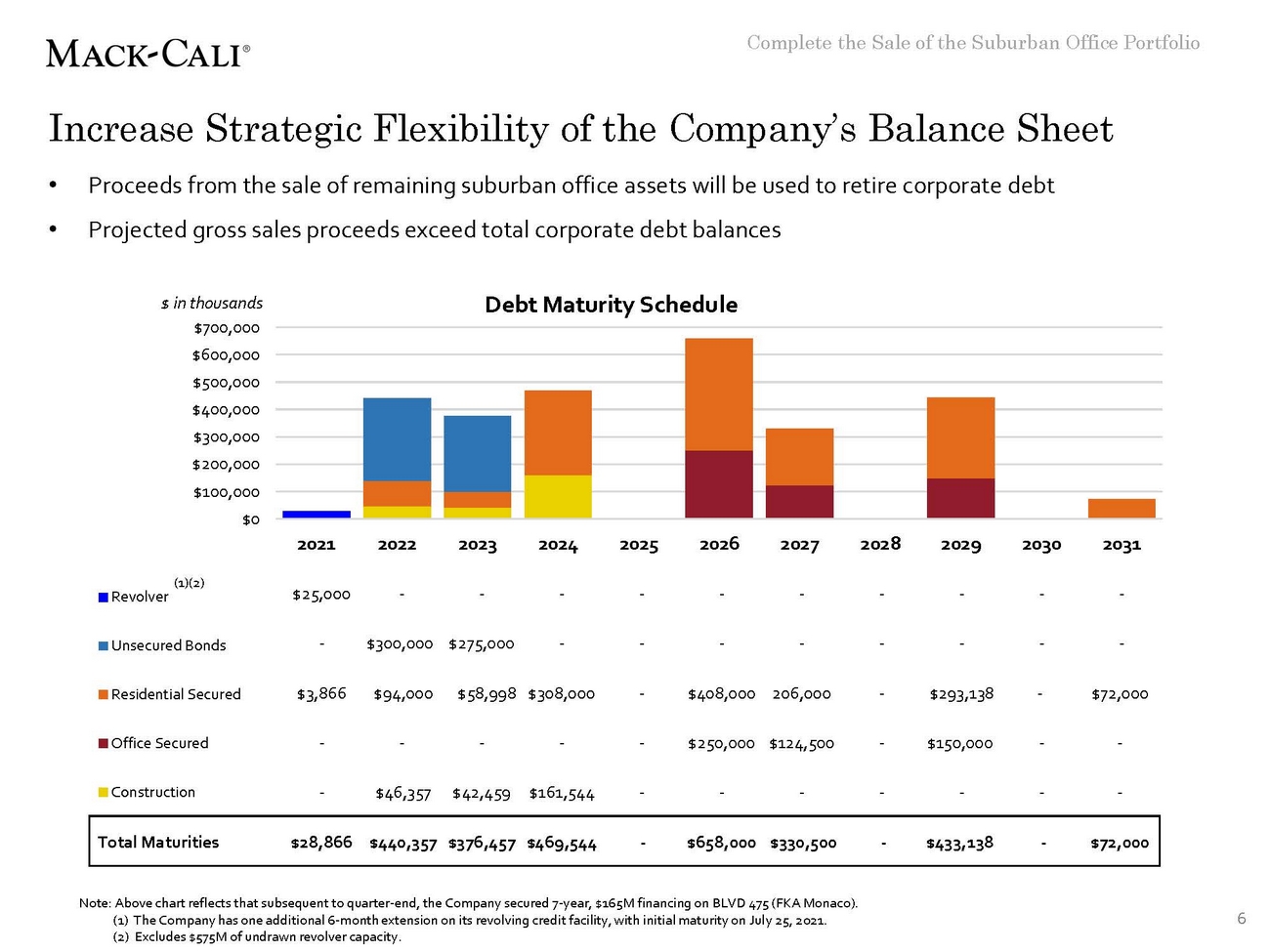

Complete the Sale of the Suburban Office Portfolio Increase Strategic Flexibility of the Company’s Balance Sheet • • Proceeds from the sale of remaining suburban office assets will be used to retire corporate debt Projected gross sales proceeds exceed total corporate debt balances Debt Maturity Schedule $ in thousands $700,000 $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 (1)(2) $25,000 - - - - - - - - - - Revolver - $300,000 $275,000 - - - - - - - - Unsecured Bonds $3,866 $94,000 $58,998 $308,000 - $408,000 206,000 - $293,138 - $72,000 Residential Secured - - - - - $250,000 $124,500 - $150,000 - - Office Secured Construction - $46,357 $42,459 $161,544 - - - - - - - Note: Above chart reflects that subsequent to quarter-end, the Company secured 7-year, $165M financing on BLVD 475 (FKA Monaco). (1) The Company has one additional 6-month extension on its revolving credit facility, with initial maturity on July 25, 2021. (2) Excludes $575M of undrawn revolver capacity. 6 Total Maturities$28,866 $440,357 $376,457 $469,544-$658,000 $330,500-$433,138-$72,000 |

|

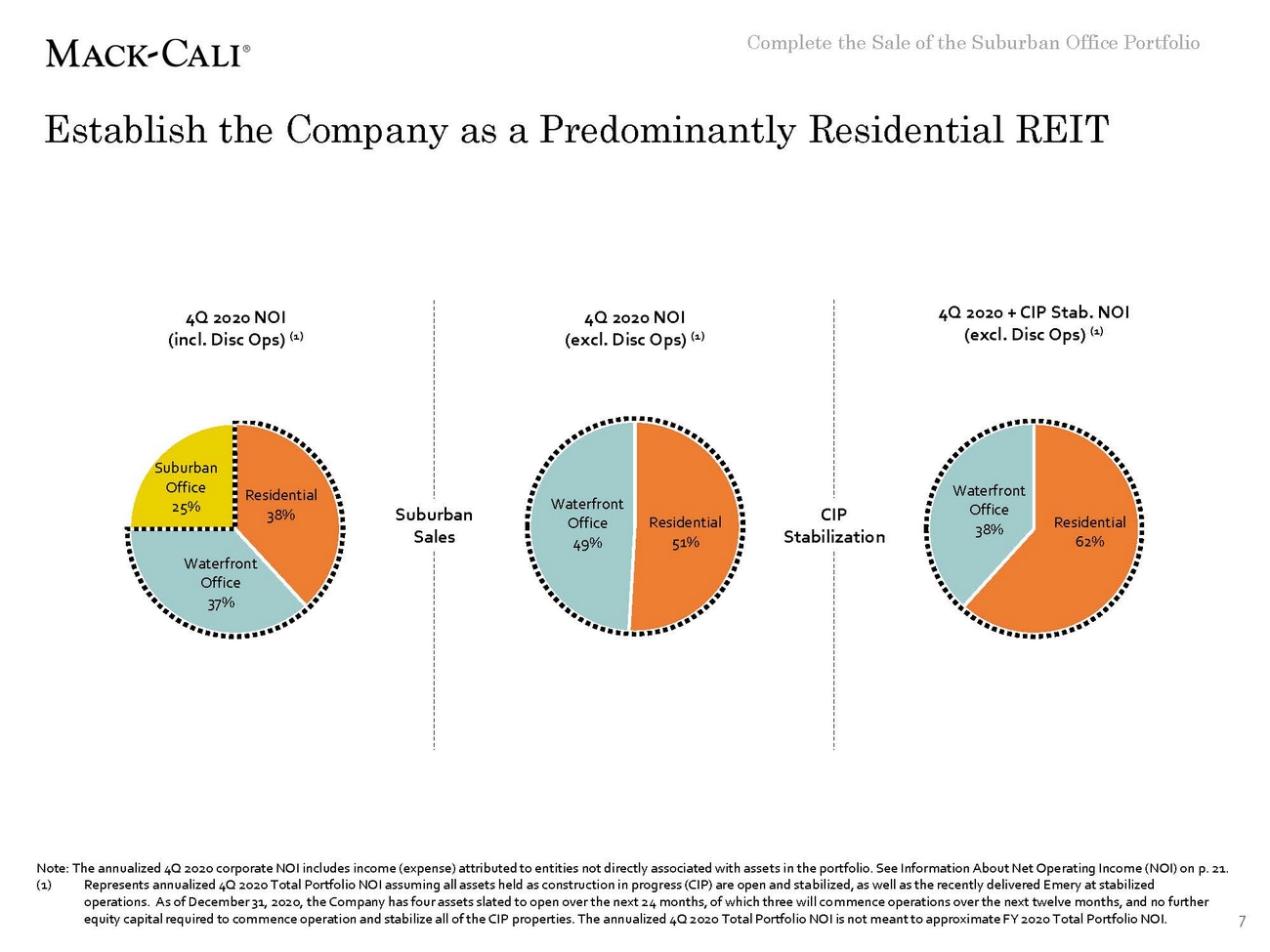

Complete the Sale of the Suburban Office Portfolio Establish the Company as a Predominantly Residential REIT 4Q 2020 + CIP Stab. NOI (excl. Disc Ops) (1) 4Q 2020 NOI (incl. Disc Ops) (1) 4Q 2020 NOI (excl. Disc Ops) (1) Suburban Office 25% Waterfront Office 38% Residential 38% Waterfront Office 49% Suburban Sales CIP Stabilization Residential 51% Residential 62% Waterfront Office 37% Note: The annualized 4Q 2020 corporate NOI includes income (expense) attributed to entities not directly associated with assets in the portfolio. See Information About Net Operating Income (NOI) on p. 21. (1) Represents annualized 4Q 2020 Total Portfolio NOI assuming all assets held as construction in progress (CIP) are open and sta bilized, as well as the recently delivered Emery at stabilized operations. As of December 31, 2020, the Company has four assets slated to open over the next 24 months, of which three will co mmence operations over the next twelve months, and no further equity capital required to commence operation and stabilize all of the CIP properties. The annualized 4Q 2020 Total Portfolio NOI is not meant to approximate FY 2020 Total Portfolio NOI. 7 |

|

Revitalize Waterfront Leasing 2 8 |

|

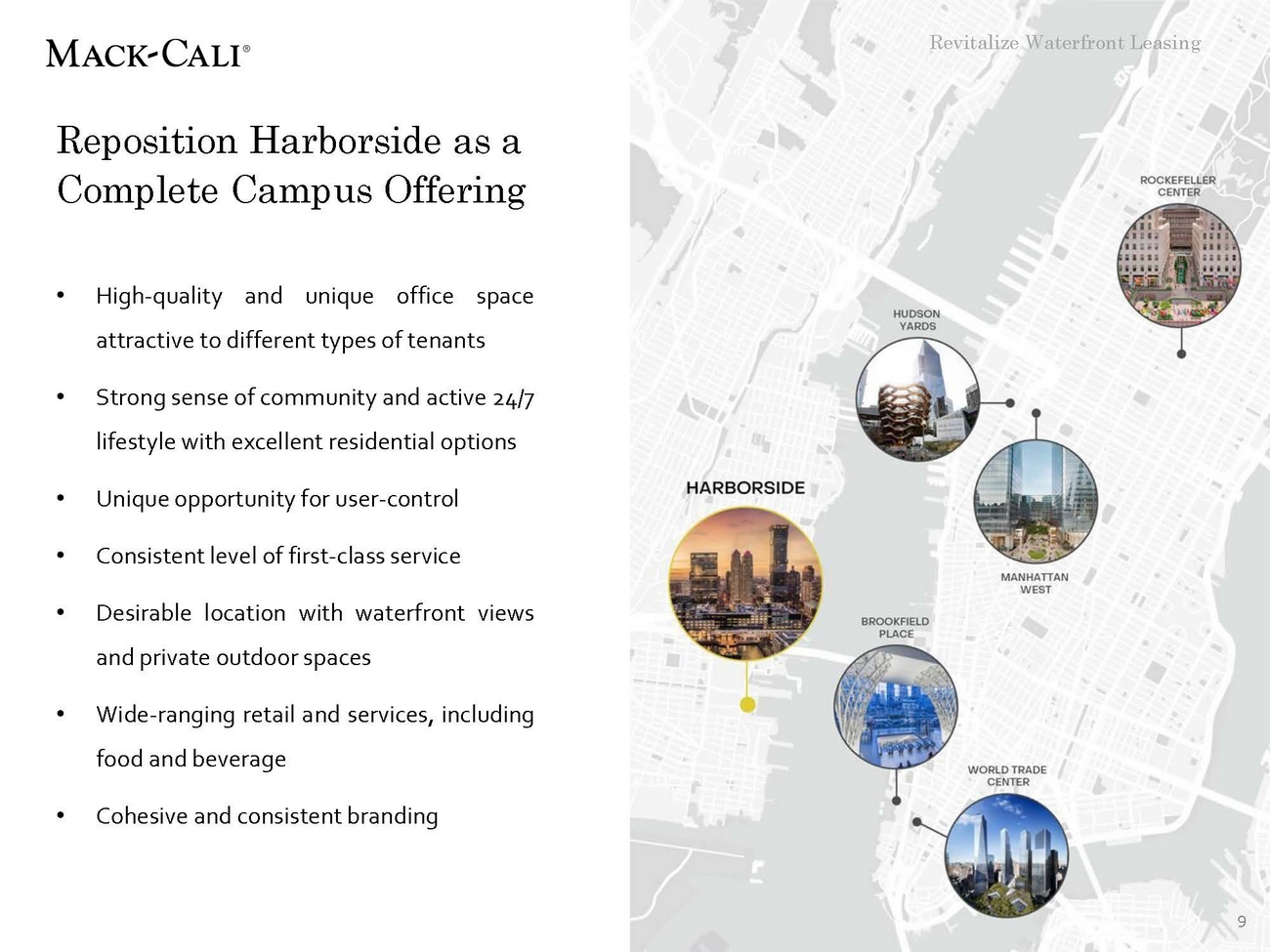

Revitalize Waterfront Leasing Reposition Harborside as a Complete Campus Offering • High-quality and unique office space attractive to different types of tenants • Strong sense of community and active 24/7 lifestyle with excellent residential options • Unique opportunity for user-control • Consistent level of first-class service • Desirable location with waterfront views and private outdoor spaces • Wide-ranging retail and services, including food and beverage • Cohesive and consistent branding 9 |

|

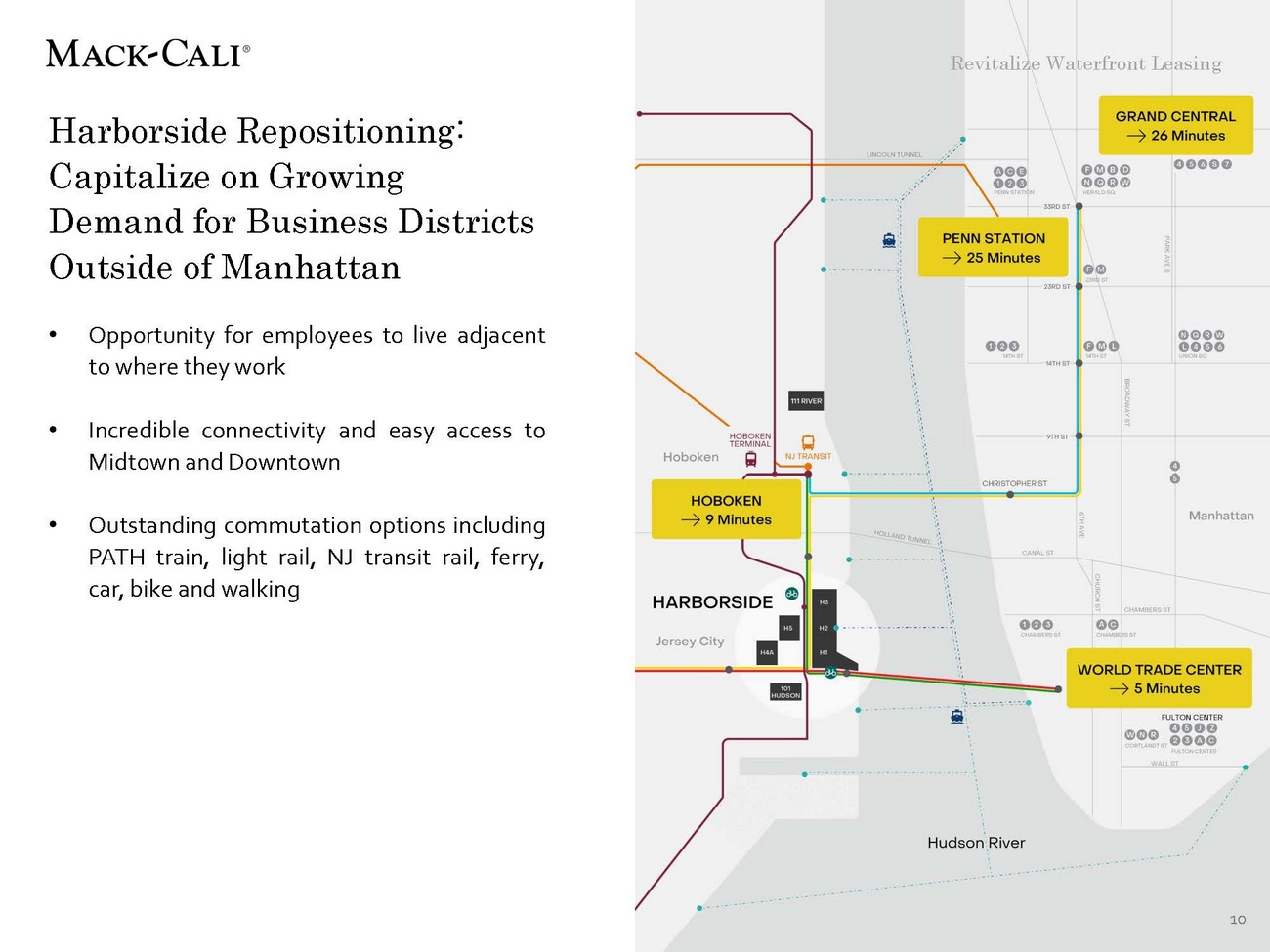

Revitalize Waterfront Leasing Revitalize Waterfront Leasing Harborside Repositioning: Capitalize on Growing Demand for Business Districts Outside of Manhattan • Opportunity for employees to live adjacent to where they work • Incredible connectivity and easy access to Midtown and Downtown • Outstanding commutation options including PATH train, light rail, car, bike and walking NJ transit rail, ferry, 10 |

|

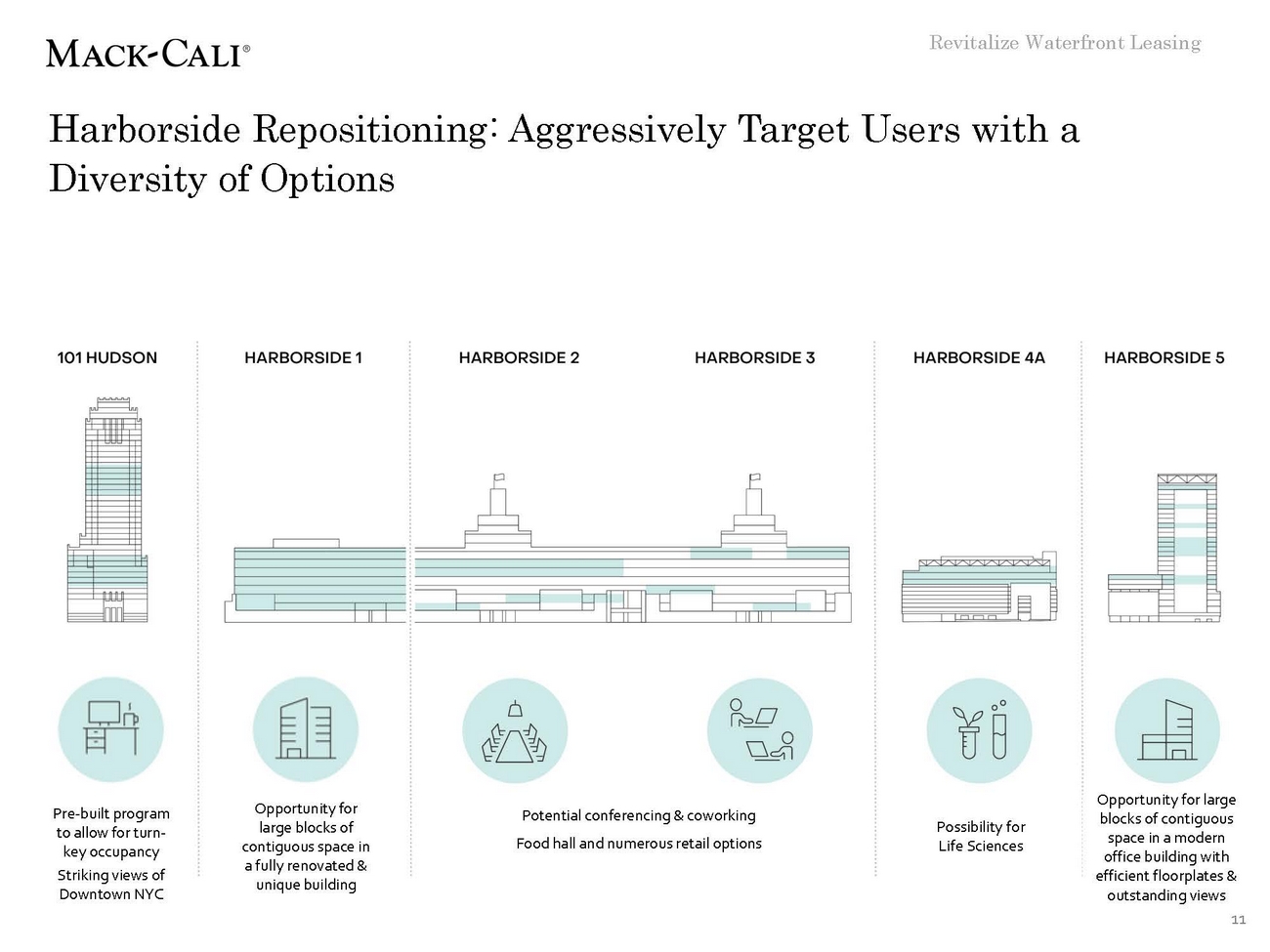

Revitalize Waterfront Leasing Harborside Repositioning: Aggressively Target Users with a Diversity of Options Opportunity for large Opportunity for large blocks of contiguous space in a fully renovated & unique building Pre-built program to allow for turn-key occupancy Striking views of Potential conferencing & coworking Food hall and numerous retail options blocks of contiguous space in a modern office building with efficient floorplates & outstanding views Possibility for Life Sciences Downtown NYC 11 |

|

Revitalize Waterfront Leasing Harborside Repositioning: Offer a Compelling Value Proposition for New York Companies 1. Analysis assumes a base rent of $43 per RSF with 2.25% fixed annual increases for Harborside, base rent of $57 per RSF for Do wntown Manhattan with a $5 per RSF increase after 5 years, and base rent of $77 per RSF for Midtown Manhattan, with a $5 per RSF increase after 5 years. Analysis assumes operating expenses of $8.30 per RSF and real estate taxes of $4.60 per RSF for Harborside, operating expenses of $12 per RSF and real estate taxes of $14 per RSF for Downtown Manhattan, and operating expenses of $14 per RSF and real estate taxes of $16 per RSF for Midtown Manhattan. All estimates are grown forward at 3% per annum. CRT is applied to the escalated rent (base rent, operating expense escalations, and real estate tax escalations) at 3.9% per annum. 2. 3. 4. 12 The NYC Measurement Conversion converts the Harborside figures to reflect the REBNY 27% full floor loss factor measurement st andard. Per Square Foot 10-Year Lease Term Harborside Downtown Manhattan Midtown Manhattan Base Rent (1) Present Value of Escalated Rent$47.12 $59.14 $79.14 OpEx & Tax Escalations ($/RSF) (2) Present Value of OpEx Escalations$1.08 Present Value of Tax Escalations$0.60 $1.56 $1.82 $1.82 $2.08 Commercial Rent Tax ($/RSF) (3) Present Value of CRT in NYCN/A$0.00 3.90%$2.44 3.90%$3.24 Escalated Rent Annuity$48.80 NYC Measurement Conversion (4) Conversion Factorx90.7% $64.96 x100.0% $86.28 x100.0% Annual Escalated Annuity - REBNY Measurement$44.26 $64.96 $86.28 Savings ($/RSF): Savings % $20.70 31.9% $42.02 48.7% |

|

Revitalize Waterfront Leasing Utilize world-class team of leasing professionals Mary Ann Tighe – CEO, Tri-State Region Edward J. Guiltinan Senior Vice President, Leasing • • • • • • • Responsible for +107.5 million SF of leases Anchored +14.4 million SF of new construction 9-time winner of REBNY’s Deal of the Year Award Named most powerful woman in NY – Crain’s Spearheaded the revitalization of Times Square & the cultural revitalization of Downtown Manhattan Twenty-year veteran at Rockefeller Group During tenure, executed +8 million SF of office, industrial and retail leases Recently leased 2 million SF of office and retail in the newly redeveloped 1271 Avenue of the Americas Former Senior Director of Leasing at Mack-Cali, where he completed +1.2 million SF of leases • • 13 |

|

Establish Roseland as an Optimized Platform 3 14 |

|

Establish Roseland as an Optimized Platform Stabilize Occupancy at Operating Properties 2020 Same Store Portfolio • TheCompany hascontinued to increase occupancy at its operating properties 10.0% 92.0% 5.0% • Same store physical occupancy 86.3% on upfrom 90.0% increased 140bps to December31st,2020, 0.0% 84.9% on September 30, 2020 88.0% • Average physical occupancy -5.0% increased each month in 4Q 2020, with the trend continuing into 2021 86.0% -10.0% • The Company has prioritized 84.0% “heads in beds”, driving occupancy with concessions and value pricing in line with comparable set 82.0% -15.0% Axis Title Physical Occupancy Net Effective Rent Roll-Up/Down (1) Note: (1)Net Effective Roll-Up/Roll Down represents lease-over-lease percentage change in rent inclusive of concessions. 15 Avg. Physical Occupancy Net Effective Rent Roll-Up/Down Focus on “Heads in Beds” |

|

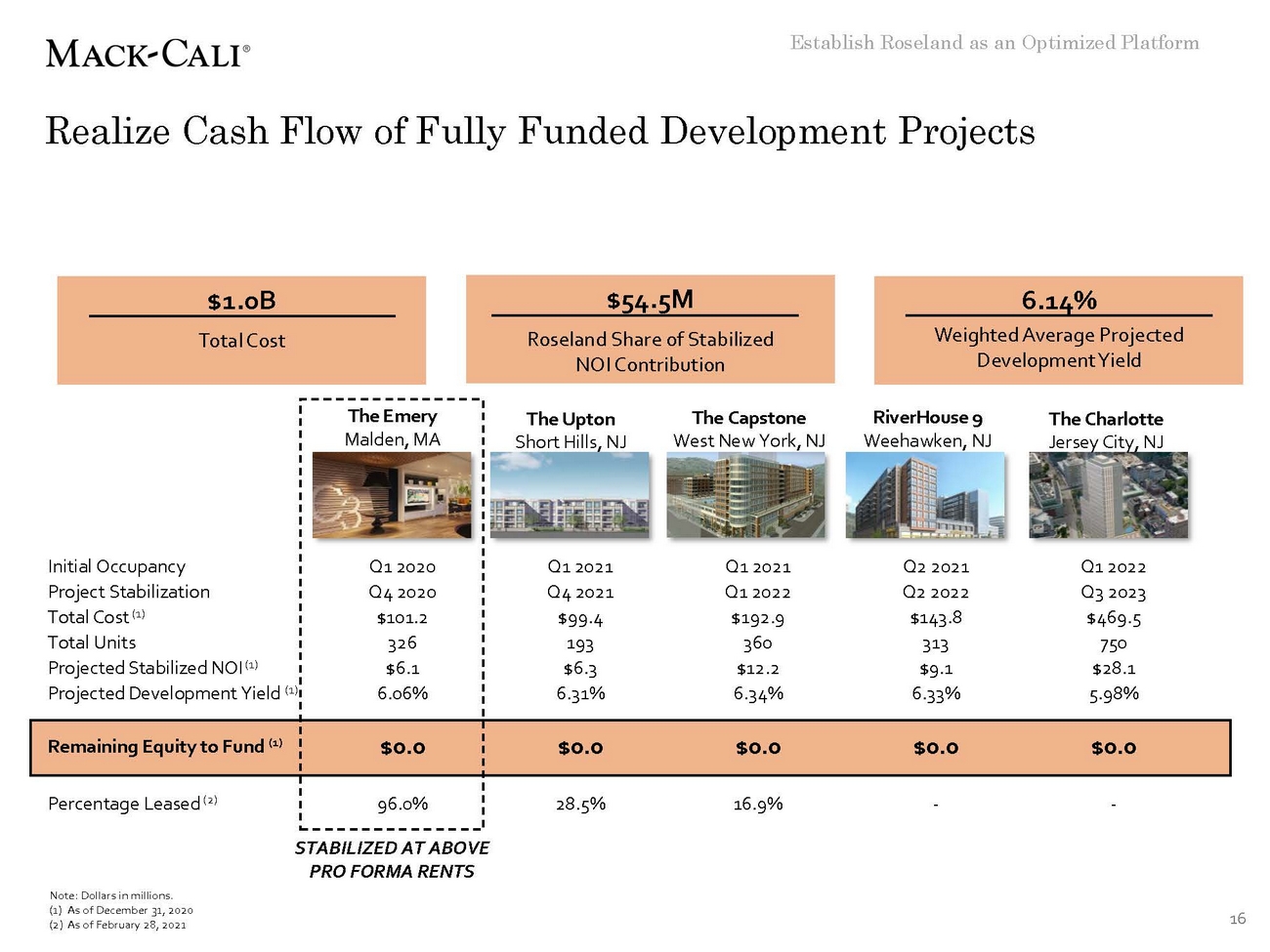

Establish Roseland as an Optimized Platform Realize Cash Flow of Fully Funded Development Projects Development Yield STABILIZED AT ABOVE PRO FORMA RENTS Note: Dollars in millions. (1) As of December 31, 2020 (2) As of February 28, 2021 16 Initial Occupancy Project Stabilization Total Cost (1) Total Units Projected Stabilized NOI (1) Projected Development Yield (1) The Emery Malden, MA Q1 2020 Q4 2020 $101.2 326 $6.1 6.06% The UptonThe CapstoneRiverHouse 9The Charlotte Short Hills, NJWest New York, NJWeehawken, NJJersey City, NJ Q1 2021Q1 2021Q2 2021Q1 2022 Q4 2021Q1 2022Q2 2022Q3 2023 $99.4$192.9$143.8$469.5 193360313750 $6.3$12.2$9.1$28.1 6.31%6.34%6.33%5.98% Remaining Equity to Fund (1) $0.0 $0.0$0.0$0.0$0.0 Percentage Leased (2) 96.0% 28.5%16.9%--6.14% Weighted Average Projected $54.5M Roseland Share of Stabilized NOI Contribution $1.0B Total Cost |

|

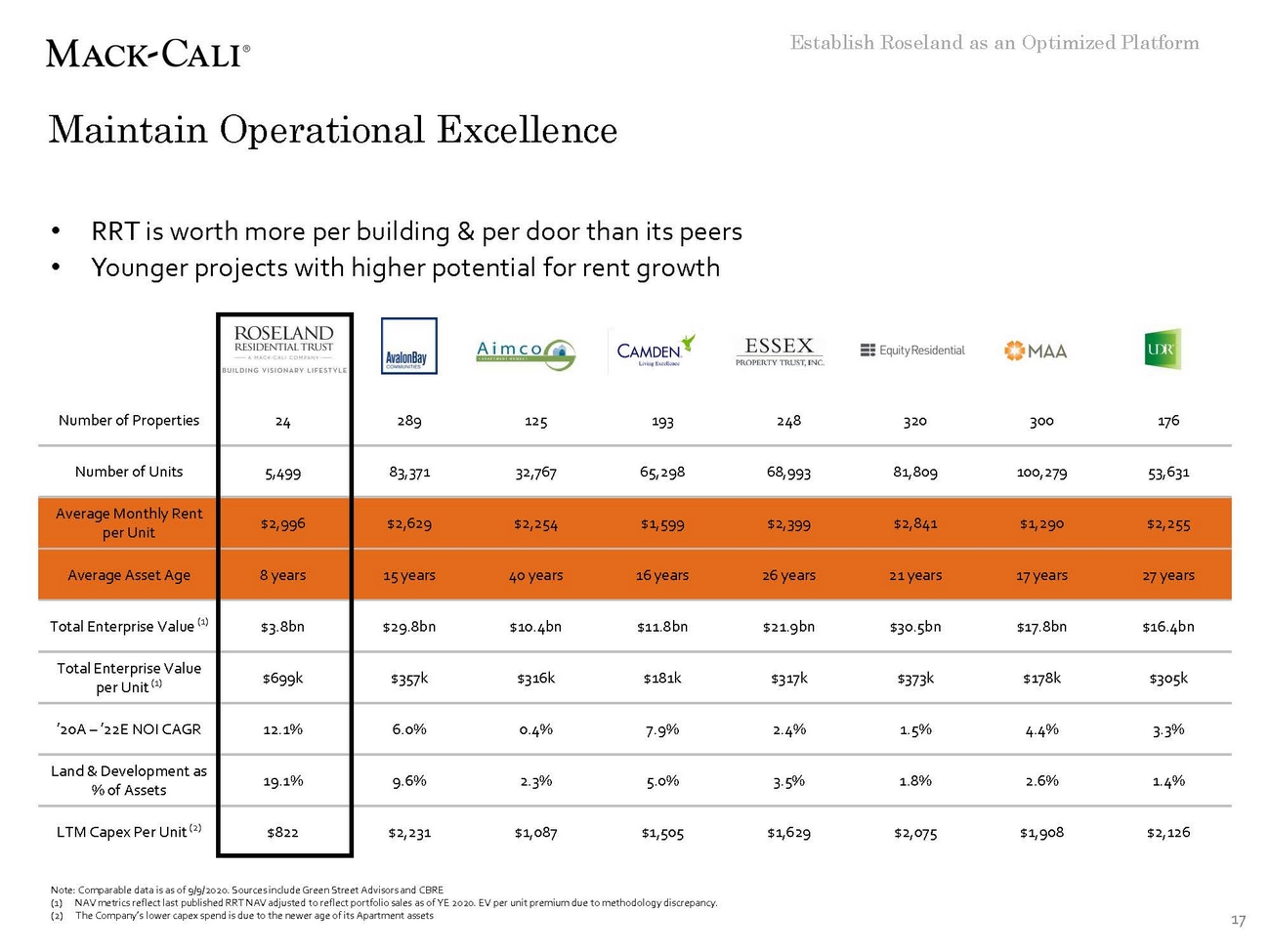

Establish Roseland as an Optimized Platform Maintain Operational Excellence • • RRT is worth more per building & per door than its peers Younger projects with higher potential for rent growth Note: Comparable data is as of 9/9/2020. Sources include Green Street Advisors and CBRE (1) NAV metrics reflect last published RRT NAV adjusted to reflect portfolio sales as of YE 2020. EV per unit premium due to methodology discrepancy. (2) The Company’s lower capex spend is due to the newer age of its Apartment assets 17 Number of Properties 24 289125193248320300176 Number of Units 5,499 83,37132,76765,29868,99381,809100,27953,631 Average Monthly Rent per Unit $2,996 $2,629$2,254$1,599$2,399$2,841$1,290$2,255 Average Asset Age 8 years 15 years40 years16 years26 years21 years17 years27 years Total Enterprise Value (1) $3.8bn $29.8bn$10.4bn$11.8bn$21.9bn$30.5bn$17.8bn$16.4bn Total Enterprise Value per Unit (1) $699k $357k$316k$181k$317k$373k$178k$305k ’20A – ’22E NOI CAGR 12.1% 6.0%0.4%7.9%2.4%1.5%4.4%3.3% Land & Development as % of Assets 19.1% 9.6%2.3%5.0%3.5%1.8%2.6%1.4% LTM Capex Per Unit (2) $822 $2,231$1,087$1,505$1,629$2,075$1,908$2,126 |

|

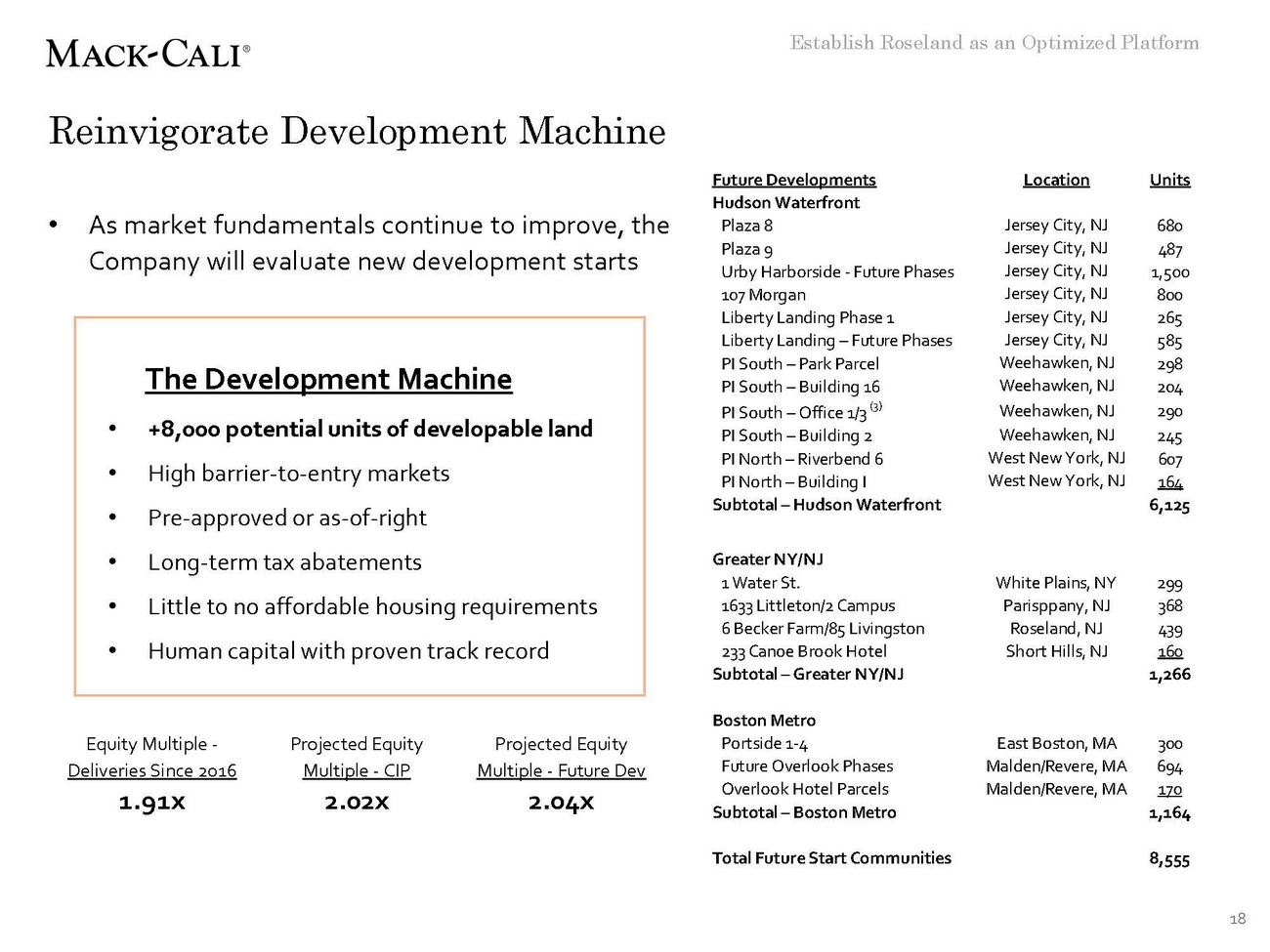

Establish Roseland as an Optimized Platform Reinvigorate Development Machine Future Developments Location Units Hudson Waterfront Plaza 8 Plaza 9 Urby Harborside - Future Phases 107 Morgan Liberty Landing Phase 1 Liberty Landing – Future Phases PI South – Park Parcel PI South – Building 16 PI South – Office 1/3 (3) PI South – Building 2 PI North – Riverbend 6 PI North – Building I Subtotal – Hudson Waterfront • As market fundamentals continue to improve, the Company will evaluate new development starts Jersey City, NJ Jersey City, NJ Jersey City, NJ Jersey City, NJ Jersey City, NJ Jersey City, NJ Weehawken, NJ Weehawken, NJ Weehawken, NJ Weehawken, NJ West New York, NJ West New York, NJ 680 487 1,500 800 265 585 298 204 290 245 607 164 6,125 Greater NY/NJ 1 Water St. 1633 Littleton/2 Campus 6 Becker Farm/85 Livingston 233 Canoe Brook Hotel Subtotal – Greater NY/NJ White Plains, NY Parisppany, NJ Roseland, NJ Short Hills, NJ 299 368 439 160 1,266 Boston Metro Portside 1-4 Future Overlook Phases Overlook Hotel Parcels Subtotal – Boston Metro Equity Multiple - Deliveries Since 2016 Projected Equity Multiple - CIP Projected Equity Multiple - Future Dev East Boston, MA Malden/Revere, MA Malden/Revere, MA 300 694 170 1,164 1.91x 2.02x 2.04x Total Future Start Communities 8,555 18 The Development Machine •+8,000 potential units of developable land •High barrier-to-entry markets •Pre-approved or as-of-right •Long-term tax abatements •Little to no affordable housing requirements •Human capital with proven track record |

|

Appendix 19 |

|

Global Definitions Average Revenue Per Home: Calculated as total apartment revenue for the Operating Communities: Communities that have achieved Project quarter ended September 30, 2020 divided by the average percent occupied for the quarter ended September 30, 2020, divided by the number of apartments and divided by three. Consolidated Operating Communities: Wholly-owned communities and Stabilization. Predevelopment Communities: Communities where the Company has communities for which the Company has a controlling interest. commenced predevelopment activities that have a near-term projected project start. Project Completion: As evidenced by a certificate of completion by a certified Class A Suburban: Long-term hold office properties in targeted submarkets; formerly defined as Urban Core. Flex Parks: Primarily office/flex properties, including any office buildings architect or issuance of a final or temporary certificate of occupancy. Project Stabilization: Lease-Up communities that have achieved over 95 located within a respective park. Future Development: Represents land inventory currently owned or controlled percent leased for six consecutive weeks. Projected Stabilized Yield: Represents Projected Stabilized Residential NOI by the Company. Identified Repurposing Communities: Communities not currently owned by divided by Total Costs. Repurposing Communities: Commercial holdings of the Company which have RRT, which have been identified for transfer from Mack-Cali to RRT for residential repurposing. In-Construction Communities: Communities that are under construction and been targeted for rezoning from their existing office to new multi-family use and have a likelihood of achieving desired rezoning and project approvals. Subordinated Joint Ventures: Joint Venture communities where the have not yet commenced initial leasing activities. Company's ownership distributions are subordinate to payment of priority capital preferred returns. Suburban: Long-term hold office properties (excluding Class A Suburban and Waterfront locations); formerly defined as Suburban Core Third Party Capital: Capital invested by third parties and not the Company. Lease-Up Communities: Communities that have commenced initial operations but have not yet achieved Project Stabilization. MCRC Capital: Represents cash equity that the Company has contributed or has a future obligation to contribute to a project. Net Asset Value (NAV): The metric represents the net projected value of the Total Costs: Represents full project budget, including land and developer fees, Company’s interest after accounting for all priority debt and equity payments. The metric includes capital invested by the Company. Non-Core: Properties designated for eventual sale/disposition or repositioning/redevelopment. and interest expense through Project Completion. Waterfront: Office assets located on NJ Hudson River waterfront. 20 |

|

Information About Net Operating Income (NOI) Reconciliation of Net Income (Loss) to Net Operating Income (NOI) $ in thousands (unaudited) 4Q 2020 3Q 2020 Office/Corp $47,498 Roseland $30,800 Total $78,298 Office/Corp $8,314 Roseland ($49,432) Total ($41,118) Net Income (loss) Deduct: Real estate services income Interest and other investment loss (income) Equity in (earnings) loss of unconsolidated joint ventures General & Administrative - property level Realized (gains) losses and unrealized losses on disposition (Gain) loss on disposition of developable land Gain on sale from unconsolidated joint ventures (Gain) loss from early extinguishment of debt, net Add: Real estate services expenses General and administrative Depreciation and amortization Interest expense Property impairments Land impairments Net operating income (NOI) - (2,766) - 1,298 (1,397) (7,164) - (35,184) 272 (2,766) (1) 3,551 (1,397) (48,497) (974) (35,184) 272 (12) (1) (493) - (15,775) - - - (2,864) (2) (880) (1,638) - - - - (2,876) (3) (1,373) (1,638) (15,775) - - - (1) 2,253 - (41,333) (974) - - 28 8,801 14,746 11,396 - (6,584) 3,420 2,855 15,016 9,122 - - 3,448 11,656 29,762 20,518 - (6,584) 42 22,946 17,485 12,519 - 1,292 3,258 6,010 15,551 9,067 36,582 - 3,300 28,956 33,036 21,586 36,582 1,292 $35,830 $16,272 $52,102 $46,317 $15,652 $61,969 Definition of Net Operating Income (NOI) NOI represents total revenues less total operating expenses, as reconciled to net income above. The Company considers NOI to be a meaningful non-GAAP financial measure for making decisions and assessing unlevered performance of its property types and markets, as it relates to total return on assets, as opposed to levered return on equity. As properties are considered for sale and acquisition based on NOI estimates and projections, the Company utilizes this measure to make investment decisions, as well as compare the performance of its assets to those of its peers. NOI should not be considered a substitute for net income, and the Company’s use of NOI may not be comparable to similarly titled measures used by other companies. The Company calculates NOI before any allocations to noncontrolling interests, as those interests do not affect the overall performance of the individual assets being measured and assessed. 21 |