Exhibit 99.1

1 Supplemental Operating and Financial Data 3Q2020 November 5, 2020

Table of Contents ▪ Company Highlights Page ▪ Company Overview 4 ▪ Key Financial Metrics 6 ▪ Business Segment Disclosure 7 ▪ Financial Schedules 9 ▪ Debt Statistics 19 ▪ Unconsolidated Joint Ventures 23 ▪ Transaction Activity 24 ▪ Multifamily Portfolio ▪ Operating Schedules 26 ▪ Financial Statements 30 ▪ Office Portfolio ▪ Property Listing 33 ▪ Operating Schedules 34 3Q 2020 2 This Supplemental Operating and Financial Data should be read in connection with the company’s third quarter 2020 earnings press release (included as Exhibit 99 . 2 of the company’s Current Report on Form 8 - K, filed on November 4 , 2020 ) as certain disclosures, definitions and reconciliations in such announcement have not been included in this Supplemental Operating and Financial Data . RiverHouse 9 - Weehawken, NJ (In - Construction) The Charlotte - Jersey City, NJ (In - Construction) Harborside 2 & 3 - Jersey City, NJ

3 Company Highlights 3Q 2020 3

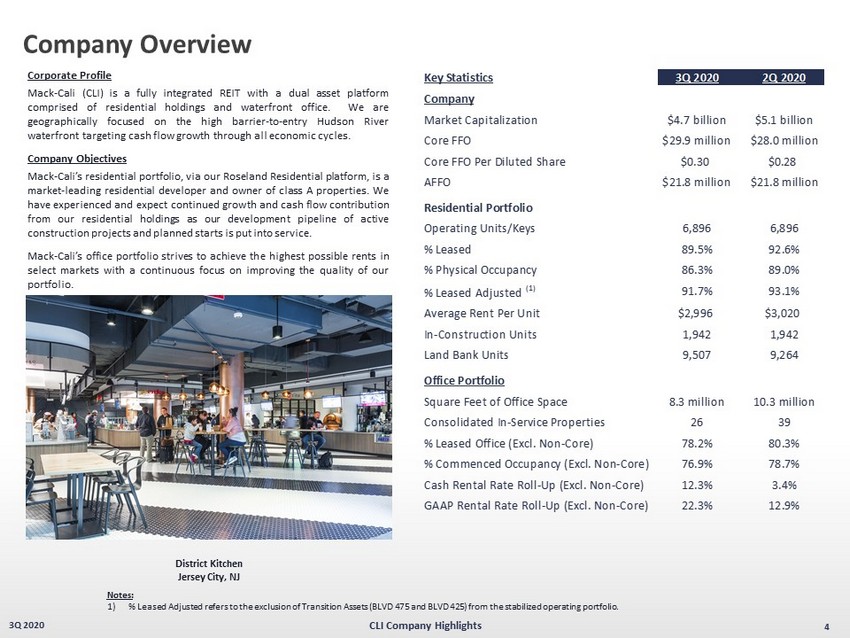

Company Overview 4 3Q 2020 Corporate Profile Mack - Cali (CLI) is a fully integrated REIT with a dual asset platform comprised of residential holdings and waterfront office . We are geographically focused on the high barrier - to - entry Hudson River waterfront targeting cash flow growth through all economic cycles . Company Objectives Mack - Cali’s residential portfolio, via our Roseland Residential platform, is a market - leading residential developer and owner of class A properties . We have experienced and expect continued growth and cash flow contribution from our residential holdings as our development pipeline of active construction projects and planned starts is put into service . Mack - Cali’s office portfolio strives to achieve the highest possible rents in select markets with a continuous focus on improving the quality of our portfolio . CLI Company Highlights District Kitchen, Harborside 2 & 3 Jersey City, NJ Key Statistics 3Q 2020 2Q 2020 Company Market Capitalization $4.7 billion $5.1 billion Core FFO $29.9 million $28.0 million Core FFO Per Diluted Share $0.30 $0.28 AFFO $21.8 million $21.8 million Residential Portfolio Operating Units/Keys 6,896 6,896 % Leased 89.5% 92.6% % Physical Occupancy 86.3% 89.0% Average Rent Per Unit $2,996 $3,020 In-Construction Units 1,942 1,942 Land Bank Units 9,507 9,264 Office Portfolio Square Feet of Office Space 8.3 million 10.3 million Consolidated In-Service Properties 26 39 % Leased Office (Excl. Non-Core) 78.2% 80.3% % Commenced Occupancy (Excl. Non-Core) 76.9% 78.7% Cash Rental Rate Roll-Up (Excl. Non-Core) 12.3% 3.4% GAAP Rental Rate Roll-Up (Excl. Non-Core) 22.3% 12.9% Average In-Place Rent Per Square Foot $37.23 $36.23

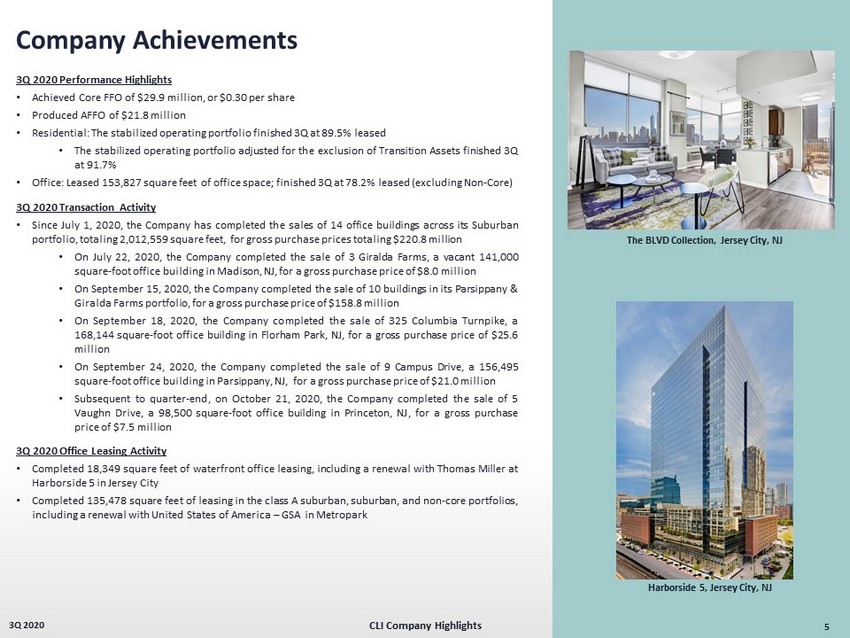

5 3Q 2020 3 Q 2020 Performance Highlights • Achieved Core FFO of $ 29 . 9 million, or $ 0 . 30 per share • Produced AFFO of $ 21 . 8 million • Residential : The stabilized operating portfolio finished 3 Q at 89 . 5 % leased • Office : Leased 153 , 827 square feet of office space ; finished 3 Q at 78 . 2 % leased (excluding Non - Core) 3 Q 2020 Transaction Activity • Since July 1 , 2020 , the Company has completed the sales of 14 office buildings across its Suburban portfolio, totaling 2 , 012 , 559 square feet, for gross purchase prices totaling $ 220 . 8 million • On July 22 , 2020 , the Company completed the sale of 3 Giralda Farms, a vacant 141 , 000 square - foot office building in Madison, NJ, for a gross purchase price of $ 8 . 0 million • On September 15 , 2020 , the Company completed the sale of 10 buildings in its Parsippany & Giralda Farms portfolio, for a gross purchase price of $ 158 . 8 million • On September 18 , 2020 , the Company completed the sale of 325 Columbia Turnpike, a 168 , 144 square - foot office building in Florham Park, NJ, for a gross purchase price of $ 25 . 6 million • On September 24 , 2020 , the Company completed the sale of 9 Campus Drive, a 156 , 495 square - foot office building in Parsippany, NJ, for a gross purchase price of $ 21 . 0 million • Subsequent to quarter - end, on October 21 , 2020 , the Company completed the sale of 5 Vaughn Drive, a 98 , 500 square - foot office building in Princeton, NJ, for a gross purchase price of $ 7 . 5 million 3 Q 2020 Office Leasing Activity • Completed 18 , 349 square feet of waterfront office leasing, including a renewal with Thomas Miller at Harborside 5 in Jersey City • Completed 135 , 478 square feet of leasing in the class A suburban, suburban, and non - core portfolios, including a renewal with United States of America – GSA in Metropark Liberty Towers, Jersey City, NJ The Capstone (Riverwalk C), West New York, NJ (rendering) Company Achievements CLI Company Highlights

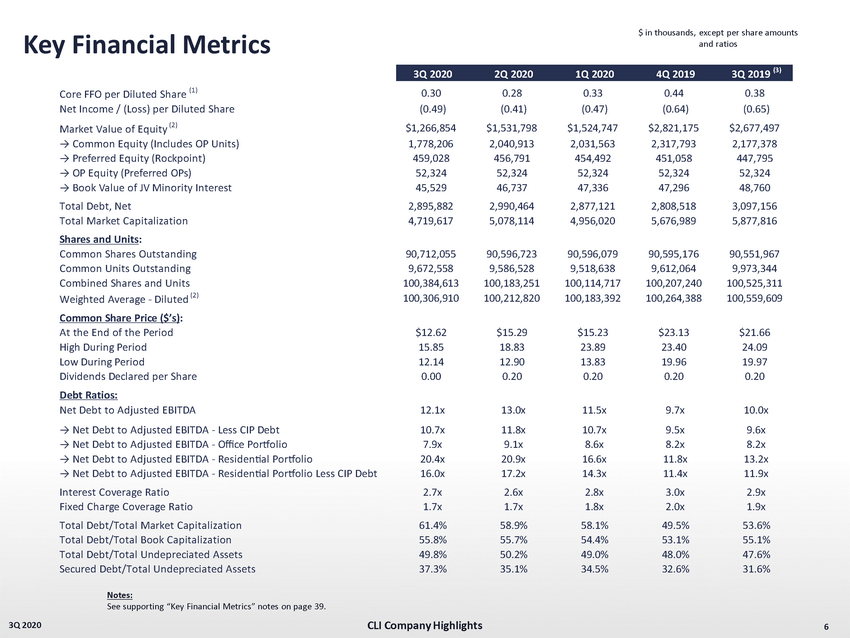

6 3Q 2020 Key Financial Metrics $ in thousands, except per share amounts and ratios Notes: See supporting “Key Financial Metrics” notes on page 39. CLI Company Highlights 3Q 2020 2Q 2020 1Q 2020 4Q 2019 3Q 2019 (3) Core FFO per Diluted Share (1) 0.30 0.28 0.33 0.44 0.38 Net Income / (Loss) per Diluted Share (0.49) (0.41) (0.47) (0.64) (0.65) Market Value of Equity (2) $1,266,854 $1,531,798 $1,524,747 $2,821,175 $2,677,497 → Common Equity (Includes OP Units) 1,778,206 2,040,913 2,031,563 2,317,793 2,177,378 → Preferred Equity (Rockpoint) 459,028 456,791 454,492 451,058 447,795 → OP Equity (Preferred OPs) 52,324 52,324 52,324 52,324 52,324 → Book Value of JV Minority Interest 45,529 46,737 47,336 47,296 48,760 Total Debt, Net 2,895,882 2,990,464 2,877,121 2,808,518 3,097,156 Total Market Capitalization 4,719,617 5,078,114 4,956,020 5,676,989 5,877,816 Shares and Units: Common Shares Outstanding 90,712,055 90,596,723 90,596,079 90,595,176 90,551,967 Common Units Outstanding 9,672,558 9,586,528 9,518,638 9,612,064 9,973,344 Combined Shares and Units 100,384,613 100,183,251 100,114,717 100,207,240 100,525,311 Weighted Average - Diluted (2) 100,306,910 100,212,820 100,183,392 100,264,388 100,559,609 Common Share Price ($’s): At the End of the Period $12.62 $15.29 $15.23 $23.13 $21.66 High During Period 15.85 18.83 23.89 23.40 24.09 Low During Period 12.14 12.90 13.83 19.96 19.97 Dividends Declared per Share 0.00 0.20 0.20 0.20 0.20 Debt Ratios: Net Debt to Adjusted EBITDA 12.1x 13.0x 11.5x 9.7x 10.0x → Net Debt to Adjusted EBITDA - Less CIP Debt 10.7x 11.8x 10.7x 9.5x 9.6x → Net Debt to Adjusted EBITDA - Office Portfolio 7.9x 9.1x 8.6x 8.2x 8.2x → Net Debt to Adjusted EBITDA - Residential Portfolio 20.4x 20.9x 16.6x 11.8x 13.2x → Net Debt to Adjusted EBITDA - Residential Portfolio Less CIP Debt 16.0x 17.2x 14.3x 11.4x 11.9x Interest Coverage Ratio 2.7x 2.6x 2.8x 3.0x 2.9x Fixed Charge Coverage Ratio 1.7x 1.7x 1.8x 2.0x 1.9x Total Debt/Total Market Capitalization 61.4% 58.9% 58.1% 49.5% 53.6% Total Debt/Total Book Capitalization 55.8% 55.7% 54.4% 53.1% 55.1% Total Debt/Total Undepreciated Assets 49.8% 50.2% 49.0% 48.0% 47.6% Secured Debt/Total Undepreciated Assets 37.3% 35.1% 34.5% 32.6% 31.6%

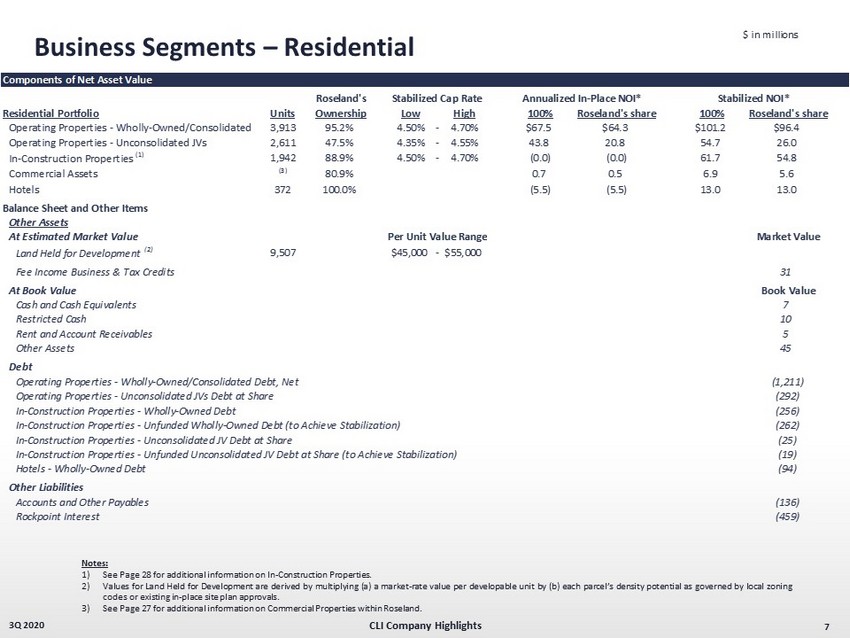

7 3Q 2020 Business Segments – Residential $ in millions Notes: 1) See Page 28 for additional information on In - Construction Properties . 2) Values for Land Held for Development are derived by multiplying (a) a market - rate value per developable unit by (b) each parcel’s density potential as governed by local zoning codes or existing in - place site plan approvals . 3) See Page 27 for additional information on Commercial Properties within Roseland . CLI Company Highlights Roseland's Residential Portfolio Units Ownership Low High 100% Roseland's share 100% Roseland's share Operating Properties - Wholly-Owned/Consolidated 3,913 95.2% 4.50% - 4.70% $67.5 $64.3 $101.2 $96.4 Operating Properties - Unconsolidated JVs 2,611 47.5% 4.35% - 4.55% 43.8 20.8 54.7 26.0 In-Construction Properties (1) 1,942 88.9% 4.50% - 4.70% (0.0) (0.0) 61.7 54.8 Commercial Assets (3) 80.9% 0.7 0.5 6.9 5.6 Hotels 372 100.0% (5.5) (5.5) 13.0 13.0 Balance sheet and other items Other assets At estimated market value Land held for development (2) 9,507 $45,000 - $55,000 At book value Book Value Cash and cash equivalents 7 Restricted cash 10 Rent and account receivables 5 Other assets 45 Other liabilities Operating Properties - Wholly-Owned/Consolidated debt, net (1,211) Operating Properties - Unconsolidated JVs debt at share (292) In-Construction Properties - Wholly-Owned debt (256) In-Construction Properties - Unfunded Wholly-Owned debt (to achieve stabilization) (262) In-Construction Properties - Unconsolidated JV debt at share (25) In-Construction Properties - Unfunded Unconsolidated JV debt at share (to achieve stabilization) (19) Hotels - Wholly-Owned debt (94) Accounts and other payables (136) Rockpoint Interest (459) Asset and development management Fees from consolidated and unconsolidated ventures 31 Per Unit Value Range Annualized In-Place NOI* Stabilized NOI* Select Business Segment Disclosure Stabilized Cap Rate Range

Business Segments – Office 8 3Q 2020 $ in millions CLI Company Highlights Notes: 1) These assets are under contract for sale for total gross proceeds in a range of $ 375 - $ 385 million . These assets represent 1 , 667 , 962 square feet . 2) Represents the Hyatt Regency in Jersey City, which is not part of Roseland . 3) Estimated market values for Land Held for Development are based on the estimated buildable SF and marketable units at estimated market pricing . The low range assumes 90 . 0 % of the high range of value . Annualized In-Place NOI* Office Portfolio MSF Ownership At Share Occupancy Hudson Waterfront (Jersey City, Hoboken) 4.908 100.0% $82.9 76.9% Class A Suburban (Metropark, Short Hills) (1) 1.955 100.0% 43.9 89.0% Suburban (1) 1.877 100.0% 22.9 70.0% Office JVs 0.246 41.9% 1.3 97.1% Retail 0.191 100.0% 2.3 N/A Hotel (2) 351 units 50.0% (7.1) N/A Balance sheet and other items Other assets At estimated market value Low High Land held for development (3) $111.1 $123.5 At book value Book Value Cash and cash equivalents 16 Restricted cash 4 Rent and account receivables 92 Other assets 217 Other liabilities Unsecured revolving credit facility and term loans (156) Senior unsecured notes, net (572) Consolidated property debt (521) Unconsolidated property debt at share (53) Accounts and other payables (166) Preferred Equity/LP Interests (53) Common Stock and operating partnership units Outstanding shares of common stock and operating partnership units 100 Select Business Segment Disclosure

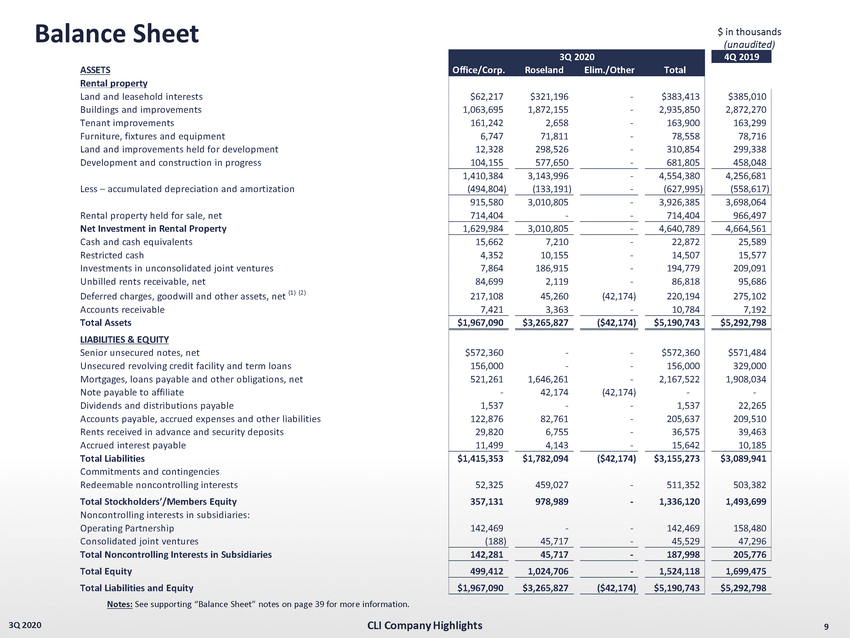

9 3Q 2020 Balance Sheet $ in thousands (unaudited) Notes: See supporting “Balance Sheet” notes on page 39 for more information. CLI Company Highlights 4Q 2019 ASSETS Office/Corp. Roseland Elim./Other Total Rental property Land and leasehold interests $62,217 $321,196 - $383,413 $385,010 Buildings and improvements 1,063,695 1,872,155 - 2,935,850 2,872,270 Tenant improvements 161,242 2,658 - 163,900 163,299 Furniture, fixtures and equipment 6,747 71,811 - 78,558 78,716 Land and improvements held for development 12,328 298,526 - 310,854 299,338 Development and construction in progress 104,155 577,650 - 681,805 458,048 1,410,384 3,143,996 - 4,554,380 4,256,681 Less – accumulated depreciation and amortization (494,804) (133,191) - (627,995) (558,617) 915,580 3,010,805 - 3,926,385 3,698,064 Rental property held for sale, net 714,404 - - 714,404 966,497 Net Investment in Rental Property 1,629,984 3,010,805 - 4,640,789 4,664,561 Cash and cash equivalents 15,662 7,210 - 22,872 25,589 Restricted cash 4,352 10,155 - 14,507 15,577 Investments in unconsolidated joint ventures 7,864 186,915 - 194,779 209,091 Unbilled rents receivable, net 84,699 2,119 - 86,818 95,686 Deferred charges, goodwill and other assets, net (1) (2) 217,108 45,260 (42,174) 220,194 275,102 Accounts receivable 7,421 3,363 - 10,784 7,192 Total Assets $1,967,090 $3,265,827 ($42,174) $5,190,743 $5,292,798 LIABILITIES & EQUITY Senior unsecured notes, net $572,360 - - $572,360 $571,484 Unsecured revolving credit facility and term loans 156,000 - - 156,000 329,000 Mortgages, loans payable and other obligations, net 521,261 1,646,261 - 2,167,522 1,908,034 Note payable to affiliate - 42,174 (42,174) - - Dividends and distributions payable 1,537 - - 1,537 22,265 Accounts payable, accrued expenses and other liabilities 122,876 82,761 - 205,637 209,510 Rents received in advance and security deposits 29,820 6,755 - 36,575 39,463 Accrued interest payable 11,499 4,143 - 15,642 10,185 Total Liabilities $1,415,353 $1,782,094 ($42,174) $3,155,273 $3,089,941 Commitments and contingencies Redeemable noncontrolling interests 52,325 459,027 - 511,352 503,382 Total Stockholders’/Members Equity 357,131 978,989 - 1,336,120 1,493,699 Noncontrolling interests in subsidiaries: Operating Partnership 142,469 - - 142,469 158,480 Consolidated joint ventures (188) 45,717 - 45,529 47,296 Total Noncontrolling Interests in Subsidiaries 142,281 45,717 - 187,998 205,776 Total Equity 499,412 1,024,706 - 1,524,118 1,699,475 Total Liabilities and Equity $1,967,090 $3,265,827 ($42,174) $5,190,743 $5,292,798 3Q 2020

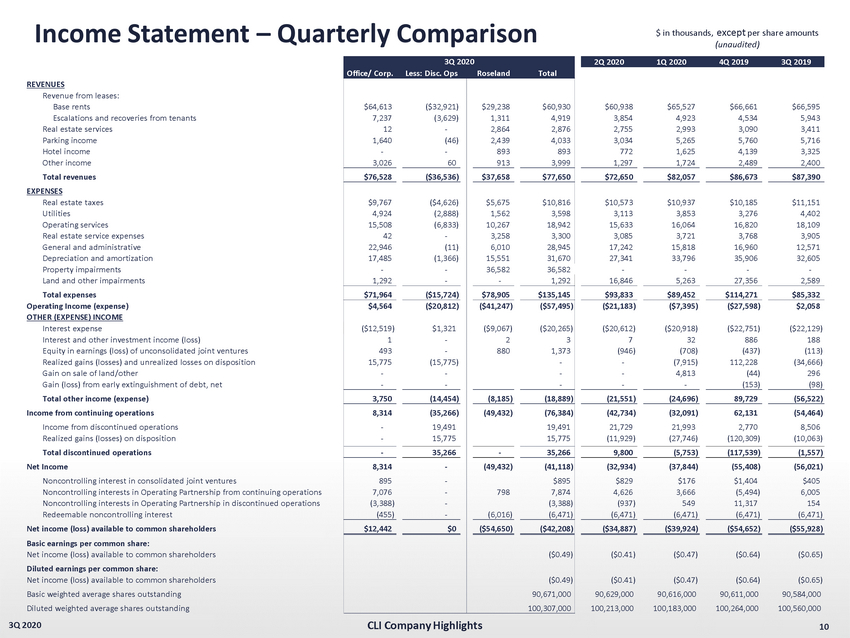

10 3Q 2020 Income Statement – Quarterly Comparison $ in thousands, except per share amounts (unaudited) CLI Company Highlights 2Q 2020 1Q 2020 4Q 2019 3Q 2019 Office/ Corp. Less: Disc. Ops Roseland Total REVENUES Revenue from leases: Base rents $64,613 ($32,921) $29,238 $60,930 $60,938 $65,527 $66,661 $66,595 Escalations and recoveries from tenants 7,237 (3,629) 1,311 4,919 3,854 4,923 4,534 5,943 Real estate services 12 - 2,864 2,876 2,755 2,993 3,090 3,411 Parking income 1,640 (46) 2,439 4,033 3,034 5,265 5,760 5,716 Hotel income - - 893 893 772 1,625 4,139 3,325 Other income 3,026 60 913 3,999 1,297 1,724 2,489 2,400 Total revenues $76,528 ($36,536) $37,658 $77,650 $72,650 $82,057 $86,673 $87,390 EXPENSES Real estate taxes $9,767 ($4,626) $5,675 $10,816 $10,573 $10,937 $10,185 $11,151 Utilities 4,924 (2,888) 1,562 3,598 3,113 3,853 3,276 4,402 Operating services 15,508 (6,833) 10,267 18,942 15,633 16,064 16,820 18,109 Real estate service expenses 42 - 3,258 3,300 3,085 3,721 3,768 3,905 General and administrative 22,946 (11) 6,010 28,945 17,242 15,818 16,960 12,571 Depreciation and amortization 17,485 (1,366) 15,551 31,670 27,341 33,796 35,906 32,605 Property impairments - - 36,582 36,582 - - - - Land and other impairments 1,292 - - 1,292 16,846 5,263 27,356 2,589 Total expenses $71,964 ($15,724) $78,905 $135,145 $93,833 $89,452 $114,271 $85,332 Operating Income (expense) $4,564 ($20,812) ($41,247) ($57,495) ($21,183) ($7,395) ($27,598) $2,058 OTHER (EXPENSE) INCOME Interest expense ($12,519) $1,321 ($9,067) ($20,265) ($20,612) ($20,918) ($22,751) ($22,129) Interest and other investment income (loss) 1 - 2 3 7 32 886 188 Equity in earnings (loss) of unconsolidated joint ventures 493 - 880 1,373 (946) (708) (437) (113) Realized gains (losses) and unrealized losses on disposition 15,775 (15,775) - - (7,915) 112,228 (34,666) Gain on sale of land/other - - - - 4,813 (44) 296 Gain (loss) from early extinguishment of debt, net - - - - - (153) (98) Total other income (expense) 3,750 (14,454) (8,185) (18,889) (21,551) (24,696) 89,729 (56,522) Income from continuing operations 8,314 (35,266) (49,432) (76,384) (42,734) (32,091) 62,131 (54,464) Income from discontinued operations - 19,491 19,491 21,729 21,993 2,770 8,506 Realized gains (losses) on disposition - 15,775 15,775 (11,929) (27,746) (120,309) (10,063) Total discontinued operations - 35,266 - 35,266 9,800 (5,753) (117,539) (1,557) Net Income 8,314 - (49,432) (41,118) (32,934) (37,844) (55,408) (56,021) Noncontrolling interest in consolidated joint ventures 895 - $895 $829 $176 $1,404 $405 Noncontrolling interests in Operating Partnership from continuing operations 7,076 - 798 7,874 4,626 3,666 (5,494) 6,005 Noncontrolling interests in Operating Partnership in discontinued operations (3,388) - (3,388) (937) 549 11,317 154 Redeemable noncontrolling interest (455) - (6,016) (6,471) (6,471) (6,471) (6,471) (6,471) Net income (loss) available to common shareholders $12,442 $0 ($54,650) ($42,208) ($34,887) ($39,924) ($54,652) ($55,928) Basic earnings per common share: Net income (loss) available to common shareholders ($0.49) ($0.41) ($0.47) ($0.64) ($0.65) Diluted earnings per common share: Net income (loss) available to common shareholders ($0.49) ($0.41) ($0.47) ($0.64) ($0.65) Basic weighted average shares outstanding 90,671,000 90,629,000 90,616,000 90,611,000 90,584,000 Diluted weighted average shares outstanding 100,307,000 100,213,000 100,183,000 100,264,000 100,560,000 3Q 2020

FFO & Core FFO – Quarterly Comparison 11 3Q 2020 $ in thousands, except per share amounts and ratios (unaudited) Notes: See footnotes and “Information About FFO, Core FFO, AFFO & Adjusted EBITDA” on page 17. CLI Company Highlights 3Q 2020 2Q 2020 1Q 2020 4Q 2019 3Q 2019 Net income (loss) available to common shareholders ($42,208) ($34,887) ($39,924) ($54,652) ($55,928) Add (deduct): Noncontrolling interest in Operating Partnership (7,874) (4,626) (3,666) 5,494 (6,005) Noncontrolling interests in discontinued operations 3,388 937 (549) (11,317) (154) Real estate-related depreciation and amortization on continuing operations (1) 34,665 30,199 36,696 39,155 35,785 Real estate-related depreciation and amortization on discontinued operations 1,366 1,452 1,453 21,776 16,797 Property impairments on continuing operations 36,582 - - - - Property impairments on discontinued operations - - - - 5,894 Impairment of unconsolidated joint venture investment (included in Equity in earnings) - - - 3,661 - Continuing operations: Realized (gains) and unrealized losses on disposition of rental property, net - - 7,915 (112,228) 34,666 Discontinued operations: Realized (gains) loss and unrealized losses on disposition of rental property, net (15,775) 11,929 27,746 120,309 413 Funds from operations (2) $10,144 $5,004 $29,671 $12,198 $31,468 Add/(Deduct): (Gain)/Loss from extinguishment of debt, net - - - $153 $98 Dead deal costs 2,583 277 - - 271 Land and other impairments 1,292 - 5,263 27,356 6,345 Gain on disposition of developable land - 16,846 (4,813) 44 (296) Severance/separation costs on management restructuring 8,900 891 1,947 - 277 Reporting system conversion costs - - 363 998 - Strategic direction costs - - - 4,629 - Proxy fight costs 6,954 5,017 799 - - Noncontrolling interest share on consolidated joint ventures impairment charges - - - (1,263) - Core FFO $29,873 $28,035 $33,320 $44,115 $38,163 Diluted weighted average shares/units outstanding (7) 100,307,000 100,213,000 100,183,000 100,264,000 100,560,000 Funds from operations per share-diluted $0.10 $0.05 $0.30 $0.12 $0.31 Core Funds from Operations per share/unit-diluted $0.30 $0.28 $0.33 $0.44 $0.38 Dividends declared per common share $0.00 $0.20 $0.20 $0.20 $0.20

AFFO & Adjusted EBITDA – Quarterly Comparison 12 3Q 2020 $ in thousands, except per share amounts and ratios (unaudited) CLI Company Highlights 3Q 2020 2Q 2020 1Q 2020 4Q 2019 3Q 2019 Core FFO (calculated on previous page) $29,873 $28,035 $33,230 $44,115 $38,163 Add (Deduct) Non-Cash Items: Straight-line rent adjustments (3) ($467) $856 ($2,132) ($4,084) ($3,625) Amortization of market lease intangibles, net (4) (858) (857) (946) (1,116) (1,057) Amortization of lease inducements (40) 59 57 (15) (108) Amortization of stock compensation 799 2,496 2,612 2,192 2,061 Non-real estate depreciation and amortization 336 482 450 431 611 Amortization of debt discount/(premium) and mark-to-market, net (238) (238) (238) (237) (238) Amortization of deferred financing costs 1,074 1,060 1,020 1,147 1,121 Deduct: Non-incremental revenue generating capital expenditures: Building improvements (2,975) (1,104) (3,247) (6,012) (3,091) Tenant improvements and leasing commissions (5) (4,057) (2,897) (8,093) (9,354) (7,245) Tenant improvements and leasing commissions on space vacant for more than one year (1,627) (6,068) (2,958) (888) (6,138) Adjusted FFO (2) $21,821 $21,824 $19,755 $26,179 $20,454 Core FFO (calculated on previous page) $29,873 $28,035 $33,230 $44,115 $38,163 Deduct: Equity in earnings (loss) of unconsolidated joint ventures, net ($1,373) $946 $708 ($3,223) $113 Equity in earnings share of depreciation and amortization (3,331) (3,340) (3,350) (3,678) (3,655) Add-back: Interest expense 21,586 21,919 22,226 24,072 23,450 Recurring JV distributions 6,425 3,682 2,459 5,123 3,528 Income (loss) in noncontrolling interest in consolidated joint ventures (895) (830) (176) (1,404) (405) Redeemable noncontrolling interest 6,471 6,471 6,471 6,471 6,471 Income tax expense 84 34 6 0 59 Adjusted EBITDA $58,840 $56,917 $61,574 $71,476 $67,724 Net debt at period end (6) $2,858,504 $2,950,026 $2,835,993 $2,767,351 $3,097,156 Net debt to Adjusted EBITDA 12.1x 13.0x 11.5x 9.7x 10.0x Notes: See footnotes and “Information About FFO, Core FFO, AFFO & Adjusted EBITDA” on page 17.

13 3Q 2020 Income Statement – Year - to - Date Comparison $ in thousands, except per share amounts (unaudited) CLI Company Highlights All Operations Less: Disc. Ops Total All Operations Less: Disc. Ops Total REVENUES Revenue from leases: Base rents $293,450 ($106,056) $187,394 $325,551 ($118,735) $206,816 Escalations and recoveries from tenants 24,756 (11,059) 13,697 30,964 (12,833) 18,131 Real estate services 8,624 - 8,624 10,783 - 10,783 Parking income 12,477 (145) 12,332 16,269 (172) 16,097 Hotel income 3,290 - 3,290 5,702 - 5,702 Other income 6,964 56 7,020 7,324 (592) 6,732 Total revenues $349,561 ($117,204) $232,357 $396,593 ($132,332) $264,261 EXPENSES Real estate taxes $47,401 ($15,075) $32,326 $49,929 ($16,116) $33,813 Utilities 19,177 (8,613) 10,564 25,797 (11,192) 14,605 Operating services 72,698 (22,059) 50,639 78,360 (25,539) 52,821 Real estate service expenses 10,106 - 10,106 12,150 - 12,150 General and administrative 62,044 (39) 62,005 42,889 (53) 42,836 Depreciation and amortization 97,078 (4,271) 92,807 146,936 (50,826) 96,110 Property impairments 36,582 - 36,582 - - - Land and other impairments 23,401 - 23,401 5,088 - 5,088 Total expenses $368,487 ($50,057) $318,430 $361,149 ($103,726) $257,423 Operating Income (expense) ($18,926) ($67,147) ($86,073) $35,444 ($28,606) $6,838 OTHER (EXPENSE) INCOME Interest expense ($65,730) $3,935 ($61,795) ($71,739) $3,922 ($67,817) Interest and other investment income (loss) 43 (1) 42 1,528 (2) 1,526 Equity in earnings (loss) of unconsolidated joint ventures (281) - (281) (882) - (882) Gain on change of control of interests - - - 13,790 - 13,790 Realized gains (losses) and unrealized losses on disposition (31,815) 23,900 (7,915) 217,833 15,865 233,698 Gain on sale of land/other 4,813 - 4,813 566 - 566 Gain on sale of investment in unconsolidated joint venture - - - 903 - 903 Gain (loss) from early extinguishment of debt, net - - - 1,801 - 1,801 Total other income (expense) (92,970) 27,834 (65,136) 163,800 19,785 183,585 Income from continuing operations (111,896) (39,313) (151,209) 199,244 (8,821) 190,423 Income from discontinued operations - 63,213 63,213 - 24,686 24,686 Realized gains (losses) on disposition - (23,900) (23,900) - (15,865) (15,865) Total discontinued operations - 39,313 39,313 - 8,821 8,821 Net Income (111,896) - (111,896) 199,244 - 199,244 Noncontrolling interest in consolidated joint ventures 1,900 - $1,900 2,500 - $2,500 Noncontrolling interests in Operating Partnership of income from continuing operations 16,166 - 16,166 (18,191) - (18,191) Noncontrolling interests in Operating Partnership in discontinued operations (3,776) - (3,776) (896) - (896) Redeemable noncontrolling interest (19,413) - (19,413) (16,144) - (16,144) Net income (loss) available to common shareholders ($117,019) $0 ($117,019) $166,513 $0 $166,513 Basic earnings per common share: Net income (loss) available to common shareholders ($1.37) $1.59 Diluted earnings per common share: Net income (loss) available to common shareholders ($1.37) $1.59 Basic weighted average shares outstanding 90,639,000 90,539,000 Diluted weighted average shares outstanding 100,235,000 100,802,000 YTD 2020 YTD 2019

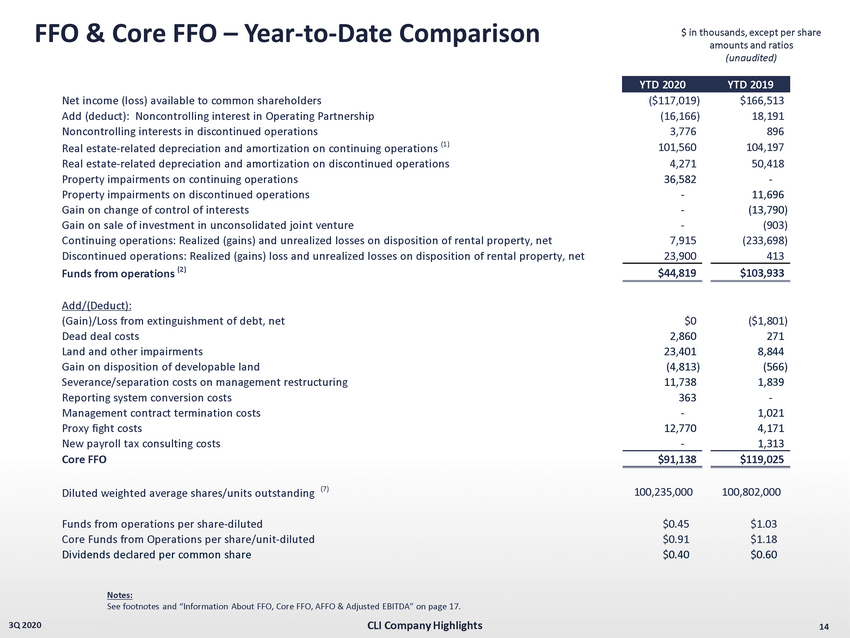

FFO & Core FFO – Year - to - Date Comparison 14 3Q 2020 $ in thousands, except per share amounts and ratios (unaudited) CLI Company Highlights Notes: See footnotes and “Information About FFO, Core FFO, AFFO & Adjusted EBITDA” on page 17. YTD 2020 YTD 2019 Net income (loss) available to common shareholders ($117,019) $166,513 Add (deduct): Noncontrolling interest in Operating Partnership (16,166) 18,191 Noncontrolling interests in discontinued operations 3,776 896 Real estate-related depreciation and amortization on continuing operations (1) 101,560 104,197 Real estate-related depreciation and amortization on discontinued operations 4,271 50,418 Property impairments on continuing operations 36,582 - Property impairments on discontinued operations - 11,696 Gain on change of control of interests - (13,790) Gain on sale of investment in unconsolidated joint venture - (903) Continuing operations: Realized (gains) and unrealized losses on disposition of rental property, net 7,915 (233,698) Discontinued operations: Realized (gains) loss and unrealized losses on disposition of rental property, net 23,900 413 Funds from operations (2) $44,819 $103,933 Add/(Deduct): (Gain)/Loss from extinguishment of debt, net $0 ($1,801) Dead deal costs 2,860 271 Land and other impairments 23,401 8,844 Gain on disposition of developable land (4,813) (566) Severance/separation costs on management restructuring 11,738 1,839 Reporting system conversion costs 363 - Management contract termination costs - 1,021 Proxy fight costs 12,770 4,171 New payroll tax consulting costs - 1,313 Core FFO $91,138 $119,025 Diluted weighted average shares/units outstanding (7) 100,235,000 100,802,000 Funds from operations per share-diluted $0.45 $1.03 Core Funds from Operations per share/unit-diluted $0.91 $1.18 Dividends declared per common share $0.40 $0.60

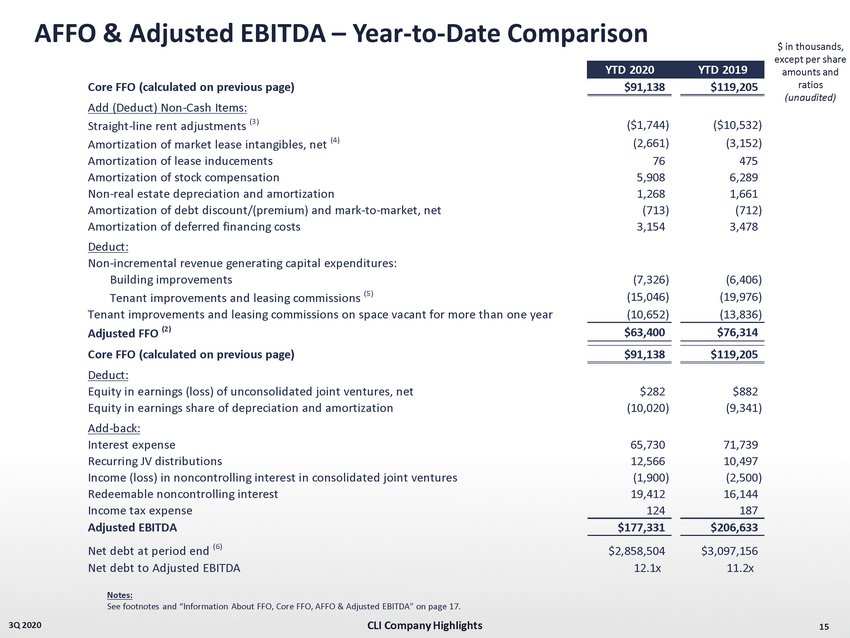

AFFO & Adjusted EBITDA – Year - to - Date Comparison 15 3Q 2020 $ in thousands, except per share amounts and ratios (unaudited) CLI Company Highlights YTD 2020 YTD 2019 Core FFO (calculated on previous page) $91,138 $119,205 Add (Deduct) Non-Cash Items: Straight-line rent adjustments (3) ($1,744) ($10,532) Amortization of market lease intangibles, net (4) (2,661) (3,152) Amortization of lease inducements 76 475 Amortization of stock compensation 5,908 6,289 Non-real estate depreciation and amortization 1,268 1,661 Amortization of debt discount/(premium) and mark-to-market, net (713) (712) Amortization of deferred financing costs 3,154 3,478 Deduct: Non-incremental revenue generating capital expenditures: Building improvements (7,326) (6,406) Tenant improvements and leasing commissions (5) (15,046) (19,976) Tenant improvements and leasing commissions on space vacant for more than one year (10,652) (13,836) Adjusted FFO (2) $63,400 $76,314 Core FFO (calculated on previous page) $91,138 $119,205 Deduct: Equity in earnings (loss) of unconsolidated joint ventures, net $282 $882 Equity in earnings share of depreciation and amortization (10,020) (9,341) Add-back: Interest expense 65,730 71,739 Recurring JV distributions 12,566 10,497 Income (loss) in noncontrolling interest in consolidated joint ventures (1,900) (2,500) Redeemable noncontrolling interest 19,412 16,144 Income tax expense 124 187 Adjusted EBITDA $177,331 $206,633 Net debt at period end (6) $2,858,504 $3,097,156 Net debt to Adjusted EBITDA 12.1x 11.2x Notes: See footnotes and “Information About FFO, Core FFO, AFFO & Adjusted EBITDA” on page 17.

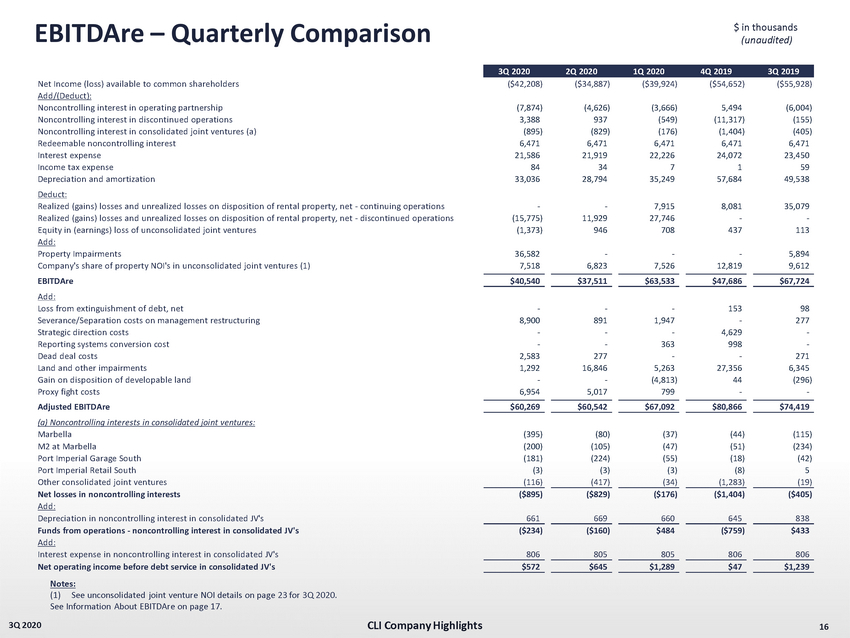

EBITDAre – Quarterly Comparison 16 3Q 2020 $ in thousands (unaudited) Notes: (1) See unconsolidated joint venture NOI details on page 23 for 3Q 2020. See Information About EBITDAre on page 17. CLI Company Highlights 3Q 2020 2Q 2020 1Q 2020 4Q 2019 3Q 2019 Net Income (loss) available to common shareholders ($42,208) ($34,887) ($39,924) ($54,652) ($55,928) Add/(Deduct): Noncontrolling interest in operating partnership (7,874) (4,626) (3,666) 5,494 (6,004) Noncontrolling interest in discontinued operations 3,388 937 (549) (11,317) (155) Noncontrolling interest in consolidated joint ventures (a) (895) (829) (176) (1,404) (405) Redeemable noncontrolling interest 6,471 6,471 6,471 6,471 6,471 Interest expense 21,586 21,919 22,226 24,072 23,450 Income tax expense 84 34 7 1 59 Depreciation and amortization 33,036 28,794 35,249 57,684 49,538 Deduct: Realized (gains) losses and unrealized losses on disposition of rental property, net - continuing operations - - 7,915 8,081 35,079 Realized (gains) losses and unrealized losses on disposition of rental property, net - discontinued operations (15,775) 11,929 27,746 - - Equity in (earnings) loss of unconsolidated joint ventures (1,373) 946 708 437 113 Add: Property Impairments 36,582 - - - 5,894 Company's share of property NOI's in unconsolidated joint ventures (1) 7,518 6,823 7,526 12,819 9,612 EBITDAre $40,540 $37,511 $63,533 $47,686 $67,724 Add: Loss from extinguishment of debt, net - - - 153 98 Severance/Separation costs on management restructuring 8,900 891 1,947 - 277 Strategic direction costs - - - 4,629 - Reporting systems conversion cost - - 363 998 - Dead deal costs 2,583 277 - - 271 Land and other impairments 1,292 16,846 5,263 27,356 6,345 Gain on disposition of developable land - - (4,813) 44 (296) Proxy fight costs 6,954 5,017 799 - - Adjusted EBITDAre $60,269 $60,542 $67,092 $80,866 $74,419 (a) Noncontrolling interests in consolidated joint ventures: Marbella (395) (80) (37) (44) (115) M2 at Marbella (200) (105) (47) (51) (234) Port Imperial Garage South (181) (224) (55) (18) (42) Port Imperial Retail South (3) (3) (3) (8) 5 Other consolidated joint ventures (116) (417) (34) (1,283) (19) Net losses in noncontrolling interests ($895) ($829) ($176) ($1,404) ($405) Add: Depreciation in noncontrolling interest in consolidated JV's 661 669 660 645 838 Funds from operations - noncontrolling interest in consolidated JV's ($234) ($160) $484 ($759) $433 Add: Interest expense in noncontrolling interest in consolidated JV's 806 805 805 806 806 Net operating income before debt service in consolidated JV's $572 $645 $1,289 $47 $1,239

FFO, Core FFO, AFFO, & Adjusted EBITDA (Notes) 17 3Q 2020 Notes (1) Includes the Company’s share from unconsolidated joint ventures, and adjustments for noncontrolling interest, of $ 3 , 331 and $ 3 , 655 for the three months ended September 30 , 2020 and 2019 , respectively, and $ 10 , 020 and $ 9 , 341 for the nine months ended September 30 , 2020 and 2019 , respectively . Excludes non - real estate - related depreciation and amortization of $ 336 and $ 611 for the three months ended September 30 , 2020 and 2019 , respectively, and $ 1 , 268 and $ 1 , 661 for the nine months ended September 30 , 2020 and 2019 . (2) Funds from operations is calculated in accordance with the definition of FFO of the National Association of Real Estate Investment Trusts (NAREIT) . See “Information About FFO, Core FFO and AFFO” below . (3) Includes free rent of $ 3 , 930 and $ 5 , 853 for the three months ended September 30 , 2020 and 2019 , respectively, and $ 10 , 187 and $ 16 , 095 for the nine months ended September 30 , 2020 and 2019 , respectively . Also includes the Company's share from unconsolidated joint ventures of $ 52 and $ 266 for the three months ended September 30 , 2020 and 2019 , respectively, and $ 69 and ( $ 59 ) for the nine months ended September 30 , 2020 and 2019 , respectively . (4) Includes the Company's share from unconsolidated joint ventures of $ 0 and $ 0 for the three months ended September 30 , 2020 and 2019 , respectively, and $ 0 and $ 0 for the nine months ended September 30 , 2020 and 2019 , respectively . (5) Excludes expenditures for tenant spaces in properties that have not been owned by the Company for at least a year . (6) Net Debt calculated by taking the sum of senior unsecured notes, unsecured revolving credit facility, and mortgages, loans payable and other obligations, and deducting cash and cash equivalents and restricted cash, all at period end . (7) Calculated based on weighted average common shares outstanding, assuming redemption of Operating Partnership common units into common shares 9 , 936 and 9 , 852 for the three months ended September 30 , 2020 and 2019 , respectively, and 9 , 411 and 9 , 960 for the nine months ended September 30 , 2020 and 2019 , respectively . Funds from operations (“FFO”) is defined as net income (loss) before noncontrolling interests of unitholders, computed in accordance with generally accepted accounting principles (“GAAP”), excluding gains or losses from depreciable rental property transactions (including both acquisitions and dispositions), and impairments related to depreciable rental property, plus real estate - related depreciation and amortization . The Company believes that FFO per share is helpful to investors as one of several measures of the performance of an equity REIT . The Company further believes that as FFO per share excludes the effect of depreciation, gains (or losses) from property transactions and impairments related to depreciable rental property (all of which are based on historical costs which may be of limited relevance in evaluating current performance), FFO per share can facilitate comparison of operating performance between equity REITs . FFO per share should not be considered as an alternative to net income available to common shareholders per share as an indication of the Company’s performance or to cash flows as a measure of liquidity . FFO per share presented herein is not necessarily comparable to FFO per share presented by other real estate companies due to the fact that not all real estate companies use the same definition . However, the Company’s FFO per share is comparable to the FFO per share of real estate companies that use the current definition of the National Association of Real Estate Investment Trusts (“NAREIT”) . A reconciliation of net income per share to FFO per share is included in the financial tables above . Core FFO is defined as FFO, as adjusted for items that may distort the comparative measurement of the Company’s performance over time . Adjusted FFO ("AFFO") is defined as Core FFO less ( i ) recurring tenant improvements, leasing commissions and capital expenditures, (ii) straight - line rents and amortization of acquired above/below - market leases, net, and (iii) other non - cash income, plus (iv) other non - cash charges . Core FFO and AFFO are both non - GAAP financial measures that are not intended to represent cash flow and are not indicative of cash flows provided by operating activities as determined in accordance with GAAP . Core FFO and AFFO are presented solely as supplemental disclosures that the Company’s management believes provides useful information regarding the Company's operating performance and its ability to fund its dividends . There are not generally accepted definitions established for Core FFO or AFFO . Therefore, the Company's measures of Core FFO and AFFO may not be comparable to the Core FFO and AFFO reported by other REITs . A reconciliation of net income to Core FFO and AFFO are included in the financial tables above . Information About FFO, Core FFO and AFFO EBITDAre is a non - GAAP financial measure. The Company computes EBITDAre in accordance with standards established by the National Association of Real Estate Investment Trusts, or NAREIT, which may n ot be comparable to EBITDAre reported by other REITs that do not compute EBITDAre in accordance with the NAREIT definition, or that interpret the NAREIT definition differently than the Company does. The Whit e Paper on EBITDAre approved by the Board of Governors of NAREIT in September 2017 defines EBITDAre as net income (loss) (computed in accordance with Generally Accepted Accounting Principles, or GAAP), plus interest expense, plus income tax expense, plus depreciation and amortization, plus (minus) losses and gains on the dispositi on of depreciated property, plus impairment write - downs of depreciated property and investments in unconsolidated joint ventures, plus adjustments to reflect the entity's share of EBITDAre of unconsolidated joint ventures. The Company presents EBITDAre , because the Company believes that EBITDAre , along with cash flow from operating activities, investing activities and financing activities, provides investors with an a ddi tional indicator of the Company’s ability to incur and service debt. EBITDAre should not be considered as an alternative to net income (determined in accordance with GAAP), as an indication of the Compan y’s financial performance, as an alternative to net cash flows from operating activities (determined in accordance with GAAP), or as a measure of the Company’s liquidity. Information About EBITDAre CLI Company Highlights

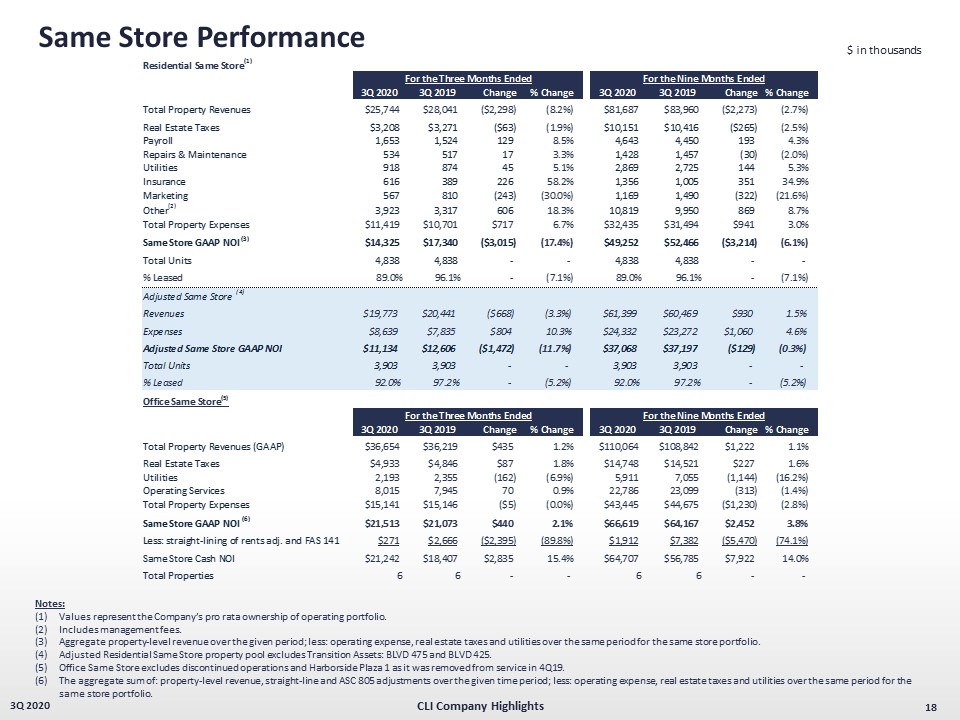

Same Store Performance 18 3Q 2020 $ in thousands Notes: (1) Values represent the Company’s pro rata ownership of operating portfolio. (2) Includes management fees. (3) Aggregate property - level revenue over the given period; less: operating expense, real estate taxes and utilities over the same p eriod for the same store portfolio. (4) Office Same Store excludes discontinued operations and Harborside Plaza 1 as it was removed from service in 4Q19. (5) The aggregate sum of: property - level revenue, straight - line and ASC 805 adjustments over the given time period; less: operating expense, real estate taxes and utilities over the same period for the same store portfolio. CLI Company Highlights Residential Same Store (1) 3Q 2020 3Q 2019 Change % Change 3Q 2020 3Q 2019 Change % Change Total Property Revenues $25,744 $28,041 ($2,298) (8.2%) $81,687 $83,960 ($2,273) (2.7%) Real Estate Taxes $3,208 $3,271 ($63) (1.9%) $10,151 $10,416 ($265) (2.5%) Payroll 1,653 1,524 129 8.5% 4,643 4,450 193 4.3% Repairs & Maintenance 534 517 17 3.3% 1,428 1,457 (30) (2.0%) Utilities 918 874 45 5.1% 2,869 2,725 144 5.3% Insurance 616 389 226 58.2% 1,356 1,005 351 34.9% Marketing 567 810 (243) (30.0%) 1,169 1,490 (322) (21.6%) Other (2) 3,923 3,317 606 18.3% 10,819 9,950 869 8.7% Total Property Expenses $11,419 $10,701 $717 6.7% $32,435 $31,494 $941 3.0% Same Store GAAP NOI (3) $14,325 $17,340 ($3,015) (17.4%) $49,252 $52,466 ($3,214) (6.1%) Total Units 4,838 4,838 - - 4,838 4,838 - - % Leased 89.0% 96.1% - (7.1%) 89.0% 96.1% - (7.1%) Less: Transition Assets Revenues $5,971 $7,600 ($1,629) (21.4%) $20,288 $23,491 ($3,203) (13.6%) Expenses $2,780 $2,866 ($86) (3.0%) $8,103 $8,222 ($119) (1.4%) NOI $3,191 $4,734 ($1,543) (32.6%) $12,185 $15,269 ($3,085) (20.2%) Adjusted Same Store GAAP NOI $11,134 $12,606 ($1,472) (11.7%) $37,068 $37,197 ($129) (0.3%) Total Units 3,903 3,903 - - 3,903 3,903 - - % Leased 92.0% 97.2% - (5.2%) 92.0% 97.2% - (5.2%) Office Same Store (4) 3Q 2020 3Q 2019 Change % Change 3Q 2020 3Q 2019 Change % Change Total Property Revenues (GAAP) $36,654 $36,219 $435 1.2% $110,064 $108,842 $1,222 1.1% Real Estate Taxes $4,933 $4,846 $87 1.8% $14,748 $14,521 $227 1.6% Utilities 2,193 2,355 (162) (6.9%) 5,911 7,055 (1,144) (16.2%) Operating Services 8,015 7,945 70 0.9% 22,786 23,099 (313) (1.4%) Total Property Expenses $15,141 $15,146 ($5) (0.0%) $43,445 $44,675 ($1,230) (2.8%) Same Store GAAP NOI (5) $21,513 $21,073 $440 2.1% $66,619 $64,167 $2,452 3.8% Less: straight-lining of rents adj. and FAS 141 $271 $2,666 ($2,395) (89.8%) $1,912 $7,382 ($5,470) (74.1%) Same Store Cash NOI $21,242 $18,407 $2,835 15.4% $64,707 $56,785 $7,922 14.0% For the Three Months Ended For the Nine Months Ended For the Three Months Ended For the Nine Months Ended

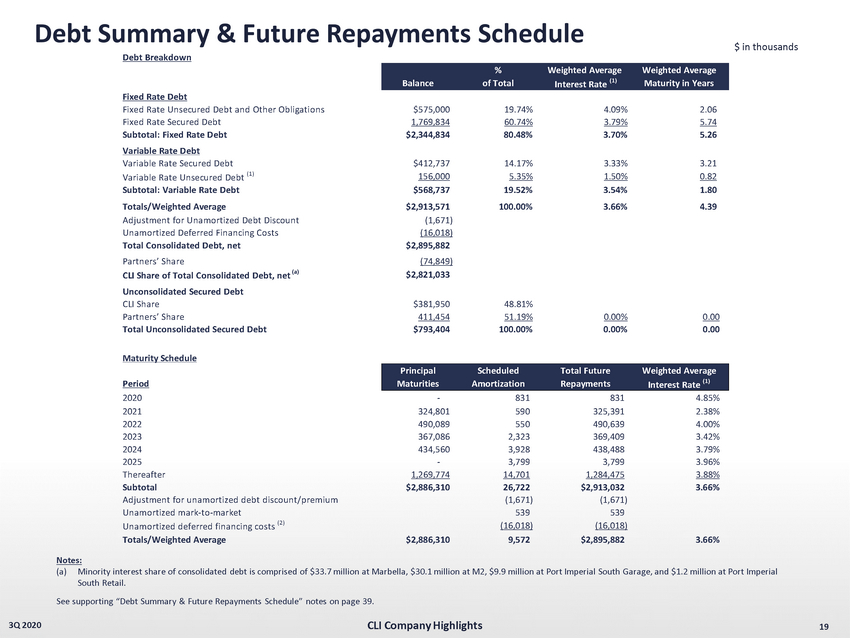

19 3Q 2020 Debt Summary & Future Repayments Schedule $ in thousands Notes: (a) Minority interest share of consolidated debt is comprised of $33.7 million at Marbella, $30.1 million at M2, $9.9 million at Por t Imperial South Garage, and $1.2 million at Port Imperial South Retail. See supporting “Debt Summary & Future Repayments Schedule” notes on page 39. CLI Company Highlights Debt Breakdown % Weighted Average Weighted Average Balance of Total Interest Rate (1) Maturity in Years Fixed Rate Debt Fixed Rate Unsecured Debt and Other Obligations $575,000 19.74% 4.09% 2.06 Fixed Rate Secured Debt 1,769,834 60.74% 3.79% 5.74 Subtotal: Fixed Rate Debt $2,344,834 80.48% 3.70% 5.26 Variable Rate Debt Variable Rate Secured Debt $412,737 14.17% 3.33% 3.21 Variable Rate Unsecured Debt (1) 156,000 5.35% 1.50% 0.82 Subtotal: Variable Rate Debt $568,737 19.52% 3.54% 1.80 Totals/Weighted Average $2,913,571 100.00% 3.66% 4.39 Adjustment for Unamortized Debt Discount (1,671) Unamortized Deferred Financing Costs (16,018) Total Consolidated Debt, net $2,895,882 Partners’ Share (74,849) CLI Share of Total Consolidated Debt, net (a) $2,821,033 Unconsolidated Secured Debt CLI Share $381,950 48.81% Partners’ Share 411,454 51.19% 0.00% 0.00 Total Unconsolidated Secured Debt $793,404 100.00% 0.00% 0.00 Maturity Schedule Principal Scheduled Total Future Weighted Average Period Maturities Amortization Repayments Interest Rate (1) 2020 - 831 831 4.85% 2021 324,801 590 325,391 2.38% 2022 490,089 550 490,639 4.00% 2023 367,086 2,323 369,409 3.42% 2024 434,560 3,928 438,488 3.79% 2025 - 3,799 3,799 3.96% Thereafter 1,269,774 14,701 1,284,475 3.88% Subtotal $2,886,310 26,722 $2,913,032 3.66% Adjustment for unamortized debt discount/premium (1,671) (1,671) Unamortized mark-to-market 539 539 Unamortized deferred financing costs (2) (16,018) (16,018) Totals/Weighted Average $2,886,310 9,572 $2,895,882 3.66%

20 3Q 2020 Residential Debt Profile Notes: See supporting “Debt Profile” notes on page 39. $ in thousands CLI Company Highlights Effective September 30, December 31, Date of Lender Interest Rate (1) 2020 2019 Maturity Secured Construction Loans Marriott Hotels at Port Imperial Fifth Third Bank LIBOR + 3.40% 94,000 74,000 04/09/22 The Emery (f.k.a. Chase III) Fifth Third Bank LIBOR + 2.50% 56,207 24,064 05/16/22 RiverHosue 9 (f.k.a. Port Imperial South 9) Bank of New York Mellon LIBOR + 2.13% 39,883 11,615 12/19/22 The Upton (f.k.a. Short Hills Residential) People's United Bank LIBOR + 2.15% 33,088 9,431 03/26/23 The Charlotte (f.k.a. 25 Christopher Columbus) QuadReal Finance LIBOR + 2.70% 126,560 5,144 12/01/24 Total Secured Construction Debt $349,738 $124,254 Secured Permanent Loans BLVD 475 (f.k.a. Monaco) (4) Northwestern Mutual Life 3.15% 165,537 166,752 02/01/21 Port Imperial South 4/5 Retail American General Life & A/G PC 4.56% 3,883 3,934 12/01/21 Portside 7 CBRE Capital Markets/FreddieMac 3.57% 58,998 58,998 08/01/23 Signature Place Nationwide Life Insurance Company 3.74% 43,000 43,000 08/01/24 Liberty Towers American General Life Insurance Company 3.37% 265,000 232,000 10/01/24 Portside 5/6 New York Life Insurance Co. 4.56% 97,000 97,000 03/10/26 BLVD 425 (f.k.a. Marbella) New York Life Insurance Co. 4.17% 131,000 131,000 08/10/26 BLVD 401 (f.k.a. M2 at Marbella) New York Life Insurance Co. 4.29% 117,000 117,000 08/10/26 145 Front Street MUFG Union Bank LIBOR + 1.84% 63,000 63,000 12/10/26 Quarry Place at Tuckahoe Natixis Real Estate Capital LLC 4.48% 41,000 41,000 08/05/27 RiverHouse 11 at Port Imperial Northwestern Mutual Life 4.52% 100,000 100,000 01/10/29 Soho Lofts New York Community Bank 3.77% 160,000 160,000 07/01/29 Riverwatch New York Community Bank 3.79% 30,000 30,000 07/01/29 Port Imperial South 4/5 Garage American General Life & A/G PC 4.85% 32,914 32,600 12/01/29 Principal balance outstanding 1,308,332 1,276,284 Unamortized deferred financing costs (11,810) (13,394) Total Secured Permanent Debt $1,296,522 $1,262,890 Total Debt - Residential Portfolio - A $1,646,260 $1,387,144

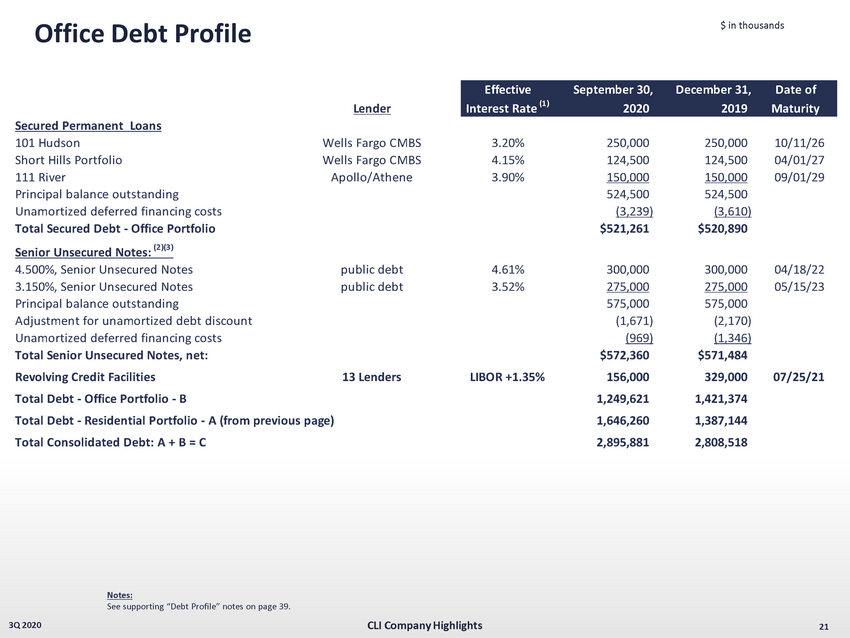

21 3Q 2020 Office Debt Profile Notes: See supporting “Debt Profile” notes on page 39. $ in thousands CLI Company Highlights Effective September 30, December 31, Date of Lender Interest Rate (1) 2020 2019 Maturity Secured Permanent Loans 101 Hudson Wells Fargo CMBS 3.20% 250,000 250,000 10/11/26 Short Hills Portfolio Wells Fargo CMBS 4.15% 124,500 124,500 04/01/27 111 River Apollo/Athene 3.90% 150,000 150,000 09/01/29 Principal balance outstanding 524,500 524,500 Unamortized deferred financing costs (3,239) (3,610) Total Secured Debt - Office Portfolio $521,261 $520,890 Senior Unsecured Notes: (2)(3) 4.500%, Senior Unsecured Notes public debt 4.61% 300,000 300,000 04/18/22 3.150%, Senior Unsecured Notes public debt 3.52% 275,000 275,000 05/15/23 Principal balance outstanding 575,000 575,000 Adjustment for unamortized debt discount (1,671) (2,170) Unamortized deferred financing costs (969) (1,346) Total Senior Unsecured Notes, net: $572,360 $571,484 Revolving Credit Facilities 13 Lenders LIBOR +1.35% 156,000 329,000 07/25/21 Total Debt - Office Portfolio - B 1,249,621 1,421,374 Total Debt - Residential Portfolio - A (from previous page) 1,646,260 1,387,144 Total Consolidated Debt: A + B = C 2,895,881 2,808,518

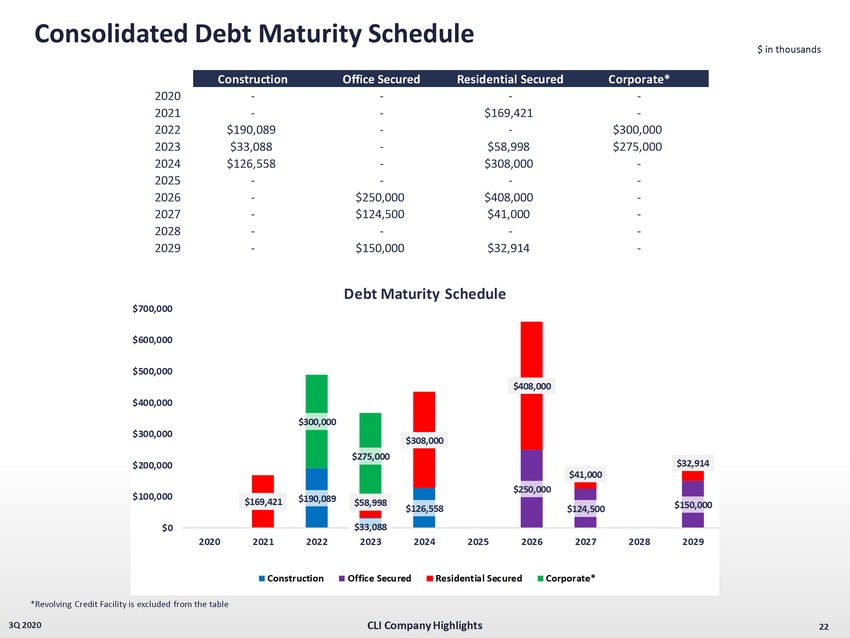

22 3Q 2020 Consolidated Debt Maturity Schedule $ in thousands CLI Company Highlights *Revolving Credit Facility is excluded from the table Construction Office Secured Residential Secured Corporate* 2020 - - - - 2021 - - $169,421 - 2022 $190,089 - - $300,000 2023 $33,088 - $58,998 $275,000 2024 $126,558 - $308,000 - 2025 - - - - 2026 - $250,000 $408,000 - 2027 - $124,500 $41,000 - 2028 - - - - 2029 - $150,000 $32,914 - $190,089 $33,088 $126,558 $250,000 $124,500 $150,000 $169,421 $58,998 $308,000 $408,000 $41,000 $32,914 $300,000 $275,000 $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 Debt Maturity Schedule Construction Office Secured Residential Secured Corporate*

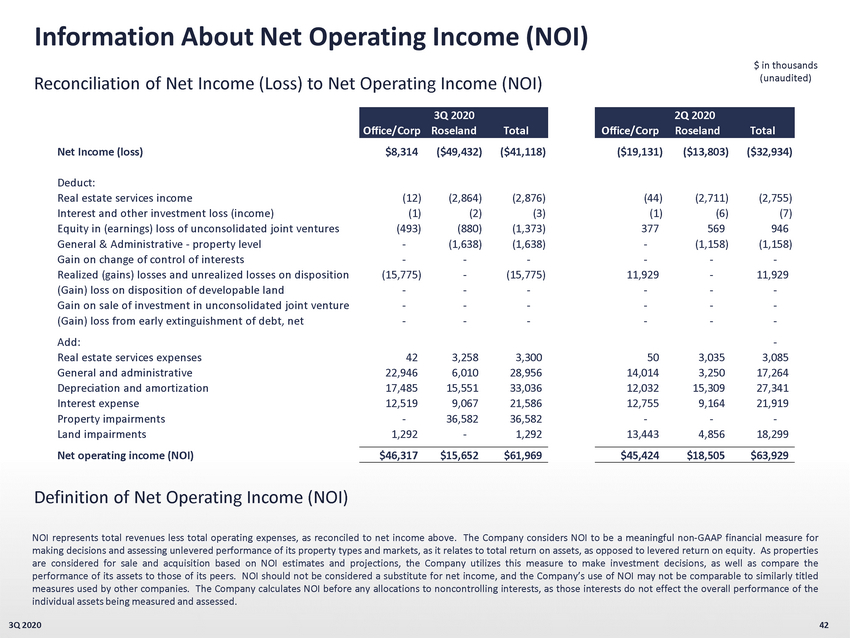

Unconsolidated Joint Ventures 23 3Q 2020 $ in thousands Notes: (a) The sum of property - level revenue, straight - line and ASC 805 adjustments; less: operating expense, real estate taxes and utilities. (b) Property - level revenue; less: operating expense, real estate taxes and utilities, property - level G&A expense and propert y - level interest expense. (c) GAAP NOI at Company’s ownership interest in the joint venture property. (d) NOI After Debt Service at Company’s ownership interest in the joint venture property, calculated as Company’s share of GAAP N OI after deducting Company’s share of the unconsolidated joint ventures’ interest expense. The Company’s share of the interest expense is $4,071,000 for 3Q 2020. See supporting “Unconsolidated Joint Ventures” notes on page 39 and Information About Net Operating Income (NOI) on page 42. CLI Company Highlights Leased CLI's Nominal 3Q 2020 Total NOI After CLI Share CLI Share CLI NOI After CLI 3Q Property Units/SF Occupancy Ownership (1) NOI (a) Debt Debt Service (b) of NOI (c) of Debt Debt Service (d) 2020 FFO Operating Properties Residential Metropolitan 130 96.2% 25.0% $627 $42,567 $368 $157 $10,642 $58 ($57) Metropolitan Lofts 59 98.3% 50.0% 199 18,200 83 100 9,100 42 21 RiverTrace at Port Imperial 316 95.3% 22.5% 1,498 82,000 840 337 18,450 189 186 Crystal House 825 90.9% 25.0% 2,752 161,500 1,339 688 40,375 335 380 Riverpark at Harrison 141 92.9% 45.0% 319 30,192 40 144 13,586 18 28 Station House 378 90.5% 50.0% 1,514 95,576 362 757 47,788 181 162 Urby Harborside 762 93.3% 85.0% 7,056 192,000 4,561 5,998 163,200 3,877 3,789 Subtotal - Residential 2,611 92.6% 47.5% $13,965 $622,035 $7,593 $8,181 $303,141 $4,700 $4,509 Office 12 Vreeland 139,750 100.0% 50.0% $399 $5,008 $351 $200 $2,504 $176 $174 Offices at Crystal Lake 106,345 93.2% 31.3% 422 2,733 422 132 854 132 121 Subtotal - Office 246,095 97.1% 41.9% $821 $7,741 $773 $332 $3,358 $308 $295 Retail/Hotel Hyatt Regency Jersey City 351 N/A 50.0% (3,525) 100,000 (3,525) (1,763) 50,000 (1,763) 413 Subtotal - Retail/Hotel N/A 50.0% ($3,525) $100,000 ($3,525) ($1,763) $50,000 ($1,763) $413 Total Operating 46.3% $11,261 $729,776 $4,841 $6,750 $356,499 $3,245 $5,217 Other Unconsolidated JVs $1,539 $63,628 $1,539 $768 25,451 $768 $147 Total Unconsolidated JVs (2) $12,800 $793,404 $6,380 $7,518 $381,950 $4,013 $5,364

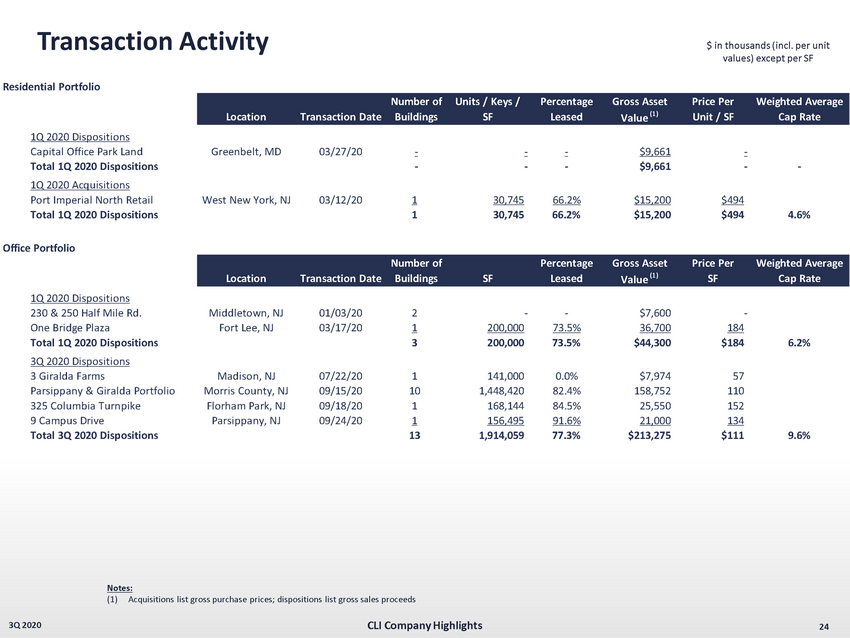

Transaction Activity 24 3Q 2020 $ in thousands (incl. per unit values) except per SF Notes: (1) Acquisitions list gross purchase prices; dispositions list gross sales proceeds CLI Company Highlights Residential Portfolio Number of Units / Keys / Percentage Gross Asset Price Per Weighted Average Location Transaction Date Buildings SF Leased Value (1) Unit / SF Cap Rate 1Q 2020 Dispositions Capital Office Park Land Greenbelt, MD 03/27/20 - - - $9,661 - Total 1Q 2020 Dispositions - - - $9,661 - - 1Q 2020 Acquisitions Port Imperial North Retail West New York, NJ 03/12/20 1 30,745 66.2% $15,200 $494 Total 1Q 2020 Dispositions 1 30,745 66.2% $15,200 $494 4.6% Office Portfolio Number of Percentage Gross Asset Price Per Weighted Average Location Transaction Date Buildings SF Leased Value (1) SF Cap Rate 1Q 2020 Dispositions 230 & 250 Half Mile Rd. Middletown, NJ 01/03/20 2 - - $7,600 - One Bridge Plaza Fort Lee, NJ 03/17/20 1 200,000 73.5% 36,700 184 Total 1Q 2020 Dispositions 3 200,000 73.5% $44,300 $184 6.2% 3Q 2020 Dispositions 3 Giralda Farms Madison, NJ 07/22/20 1 141,000 0.0% $7,974 57 Parsippany & Giralda Portfolio Morris County, NJ 09/15/20 10 1,448,420 82.4% 158,752 110 325 Columbia Turnpike Florham Park, NJ 09/18/20 1 168,144 84.5% 25,550 152 9 Campus Drive Parsippany, NJ 09/24/20 1 156,495 91.6% 21,000 134 Total 3Q 2020 Dispositions 13 1,914,059 77.3% $213,275 $111 9.6%

25 Multifamily Portfolio 3Q 2020 25

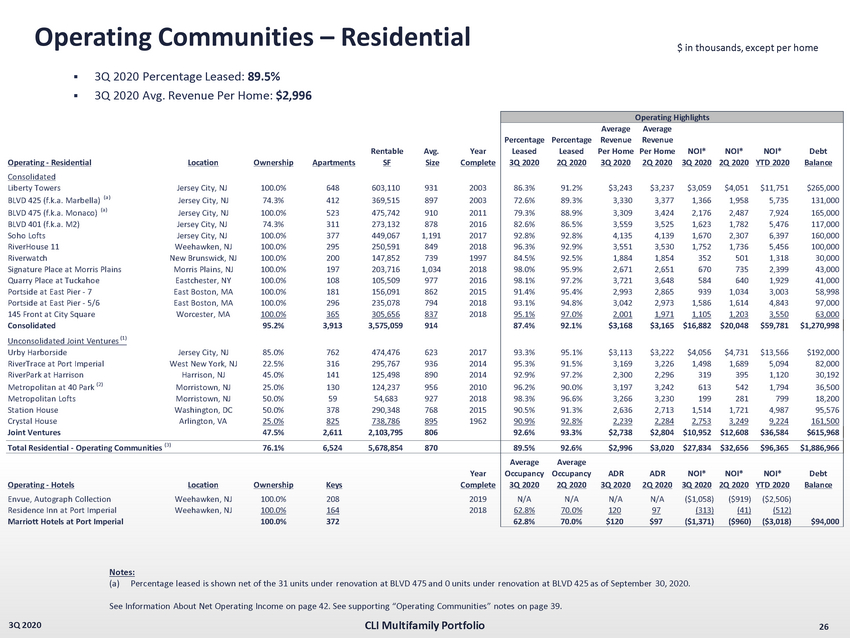

$ in thousands, except per home Operating Communities – Residential 26 3Q 2020 Notes: (a) Percentage leased is shown net of the 31 units under renovation at BLVD 475 and 0 units under renovation at BLVD 425 as of Se pte mber 30, 2020. See Information About Net Operating Income on page 42. See supporting “Operating Communities” notes on page 39. CLI Multifamily Portfolio ▪ 3 Q 2020 Percentage Leased : 89 . 5 % ▪ 3 Q 2020 Avg . Revenue Per Home : $ 2 , 996 Average Average Percentage Percentage Revenue Revenue Rentable Avg. Year Leased Leased Per Home Per Home NOI* NOI* NOI* Debt Operating - Residential Location Ownership Apartments SF Size Complete 3Q 2020 2Q 2020 3Q 2020 2Q 2020 3Q 2020 2Q 2020 YTD 2020 Balance Consolidated Liberty Towers Jersey City, NJ 100.0% 648 603,110 931 2003 86.3% 91.2% $3,243 $3,237 $3,059 $4,051 $11,751 $265,000 BLVD 425 (f.k.a. Marbella) (a) Jersey City, NJ 74.3% 412 369,515 897 2003 72.6% 89.3% 3,330 3,377 1,366 1,958 5,735 131,000 BLVD 475 (f.k.a. Monaco) (a) Jersey City, NJ 100.0% 523 475,742 910 2011 79.3% 88.9% 3,309 3,424 2,176 2,487 7,924 165,000 BLVD 401 (f.k.a. M2) Jersey City, NJ 74.3% 311 273,132 878 2016 82.6% 86.5% 3,559 3,525 1,623 1,782 5,476 117,000 Soho Lofts Jersey City, NJ 100.0% 377 449,067 1,191 2017 92.8% 92.8% 4,135 4,139 1,670 2,307 6,397 160,000 RiverHouse 11 Weehawken, NJ 100.0% 295 250,591 849 2018 96.3% 92.9% 3,551 3,530 1,752 1,736 5,456 100,000 Riverwatch New Brunswick, NJ 100.0% 200 147,852 739 1997 84.5% 92.5% 1,884 1,854 352 501 1,318 30,000 Signature Place at Morris Plains Morris Plains, NJ 100.0% 197 203,716 1,034 2018 98.0% 95.9% 2,671 2,651 670 735 2,399 43,000 Quarry Place at Tuckahoe Eastchester, NY 100.0% 108 105,509 977 2016 98.1% 97.2% 3,721 3,648 584 640 1,929 41,000 Portside at East Pier - 7 East Boston, MA 100.0% 181 156,091 862 2015 91.4% 95.4% 2,993 2,865 939 1,034 3,003 58,998 Portside at East Pier - 5/6 East Boston, MA 100.0% 296 235,078 794 2018 93.1% 94.8% 3,042 2,973 1,586 1,614 4,843 97,000 145 Front at City Square Worcester, MA 100.0% 365 305,656 837 2018 95.1% 97.0% 2,001 1,971 1,105 1,203 3,550 63,000 Consolidated 95.2% 3,913 3,575,059 914 87.4% 92.1% $3,168 $3,165 $16,882 $20,048 $59,781 $1,270,998 Unconsolidated Joint Ventures (1) Urby Harborside Jersey City, NJ 85.0% 762 474,476 623 2017 93.3% 95.1% $3,113 $3,222 $4,056 $4,731 $13,566 $192,000 RiverTrace at Port Imperial West New York, NJ 22.5% 316 295,767 936 2014 95.3% 91.5% 3,169 3,226 1,498 1,689 5,094 82,000 RiverPark at Harrison Harrison, NJ 45.0% 141 125,498 890 2014 92.9% 97.2% 2,300 2,296 319 395 1,120 30,192 Metropolitan at 40 Park (2) Morristown, NJ 25.0% 130 124,237 956 2010 96.2% 90.0% 3,197 3,242 613 542 1,794 36,500 Metropolitan Lofts Morristown, NJ 50.0% 59 54,683 927 2018 98.3% 96.6% 3,266 3,230 199 281 799 18,200 Station House Washington, DC 50.0% 378 290,348 768 2015 90.5% 91.3% 2,636 2,713 1,514 1,721 4,987 95,576 Crystal House Arlington, VA 25.0% 825 738,786 895 1962 90.9% 92.8% 2,239 2,284 2,753 3,249 9,224 161,500 Joint Ventures 47.5% 2,611 2,103,795 806 92.6% 93.3% $2,738 $2,804 $10,952 $12,608 $36,584 $615,968 Total Residential - Operating Communities (3) 76.1% 6,524 5,678,854 870 89.5% 92.6% $2,996 $3,020 $27,834 $32,656 $96,365 $1,886,966 Average Average Year Occupancy Occupancy ADR ADR NOI* NOI* NOI* Debt Operating - Hotels Location Ownership Keys Complete 3Q 2020 2Q 2020 3Q 2020 2Q 2020 3Q 2020 2Q 2020 YTD 2020 Balance Envue, Autograph Collection Weehawken, NJ 100.0% 208 2019 N/A N/A N/A N/A ($1,058) ($919) ($2,506) Residence Inn at Port Imperial Weehawken, NJ 100.0% 164 2018 62.8% 70.0% 120 97 (313) (41) (512) Marriott Hotels at Port Imperial 100.0% 372 62.8% 70.0% $120 $97 ($1,371) ($960) ($3,018) $94,000 Operating Highlights

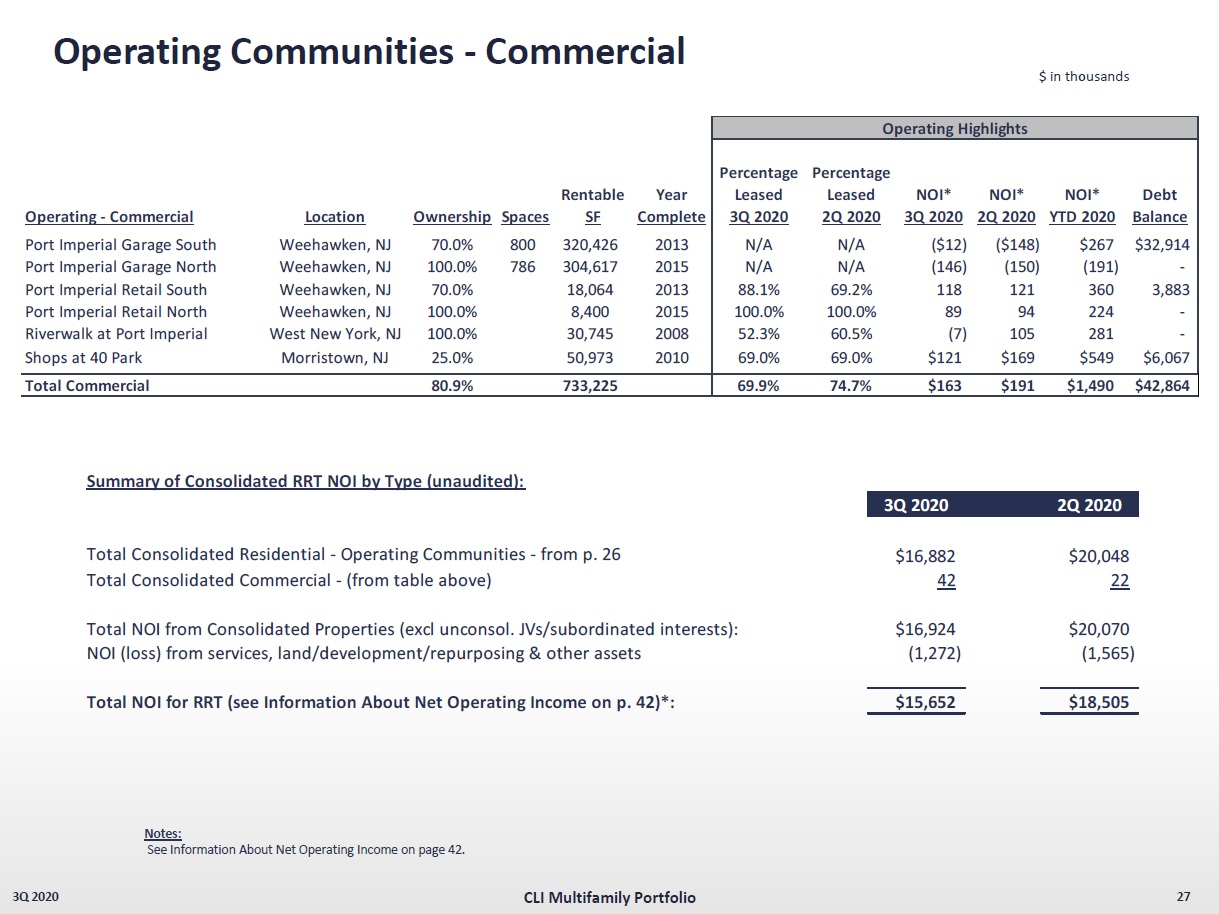

Operating Communities - Commercial 3Q 2020 27 $ in thousands CLI Multifamily Portfolio Notes: See Information About Net Operating Income on page 42. Percentage Percentage Rentable Year Leased Leased NOI* NOI* NOI* Debt Operating - Commercial Location Ownership Spaces SF Complete 3Q 2020 2Q 2020 3Q 2020 2Q 2020 YTD 2020 Balance Port Imperial Garage South Weehawken, NJ 70.0% 800 320,426 2013 N/A N/A ($12) ($148) $267 $32,914 Port Imperial Garage North Weehawken, NJ 100.0% 786 304,617 2015 N/A N/A (146) (150) (191) - Port Imperial Retail South Weehawken, NJ 70.0% 18,064 2013 88.1% 69.2% 118 121 360 3,883 Port Imperial Retail North Weehawken, NJ 100.0% 8,400 2015 100.0% 100.0% 89 94 224 - Riverwalk at Port Imperial West New York, NJ 100.0% 30,745 2008 52.3% 60.5% (7) 105 281 - Shops at 40 Park (1) Morristown, NJ 25.0% 50,973 2010 69.0% 69.0% $121 $169 $549 $6,067 Total Commercial 80.9% 733,225 69.9% 74.7% $163 $191 $1,490 $42,864 Operating Highlights Summary of Consolidated RRT NOI by Type (unaudited): 3Q 2020 2Q 2020 Total Consolidated Residential - Operating Communities - from p. 26 (2) $16,882 $20,048 Total Consolidated Commercial - (from table above) 42 22 Total NOI from Consolidated Properties (excl unconsol. JVs/subordinated interests): $16,924 $20,070 NOI (loss) from services, land/development/repurposing & other assets (1,272) (1,565) Total NOI for RRT (see Information About Net Operating Income on p. 42)*: $15,652 $18,505

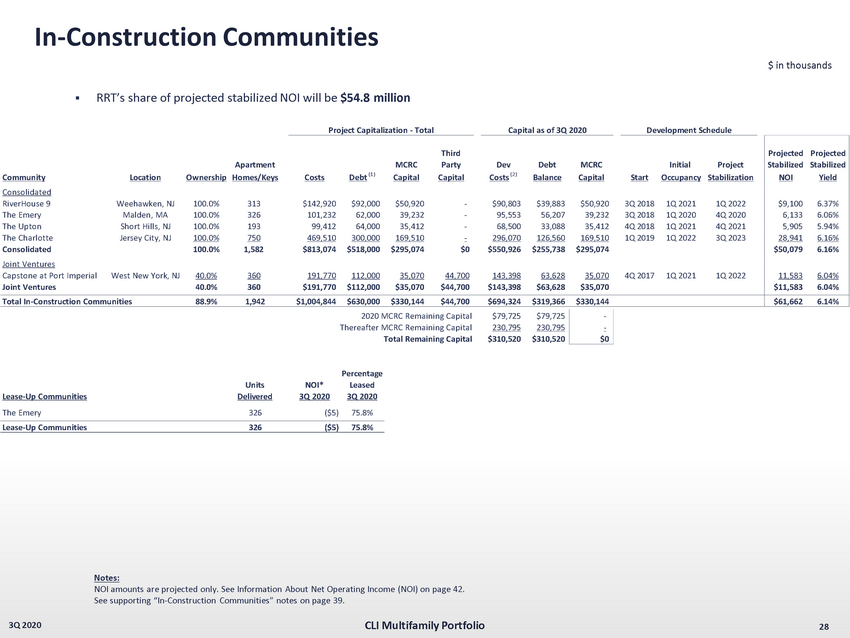

In - Construction Communities 28 3Q 2020 ▪ RRT’s share of projected stabilized NOI will be $ 54 . 8 million $ in thousands Notes: NOI amounts are projected only. See Information About Net Operating Income (NOI) on page 42. See supporting “In - Construction Communities” notes on page 39. CLI Multifamily Portfolio Third Projected Projected Apartment MCRC Party Dev Debt MCRC Initial Project Stabilized Stabilized Community Location Ownership Homes/Keys Costs Debt (1) Capital Capital Costs (2) Balance Capital Start Occupancy Stabilization NOI Yield Consolidated RiverHouse 9 Weehawken, NJ 100.0% 313 $142,920 $92,000 $50,920 - $90,803 $39,883 $50,920 3Q 2018 1Q 2021 1Q 2022 $9,100 6.37% The Emery Malden, MA 100.0% 326 101,232 62,000 39,232 - 95,553 56,207 39,232 3Q 2018 1Q 2020 4Q 2020 6,133 6.06% The Upton Short Hills, NJ 100.0% 193 99,412 64,000 35,412 - 68,500 33,088 35,412 4Q 2018 1Q 2021 4Q 2021 5,905 5.94% The Charlotte Jersey City, NJ 100.0% 750 469,510 300,000 169,510 - 296,070 126,560 169,510 1Q 2019 1Q 2022 3Q 2023 28,941 6.16% Consolidated 100.0% 1,582 $813,074 $518,000 $295,074 $0 $550,926 $255,738 $295,074 $50,079 6.16% Joint Ventures Capstone at Port Imperial West New York, NJ 40.0% 360 191,770 112,000 35,070 44,700 143,398 63,628 35,070 4Q 2017 1Q 2021 1Q 2022 11,583 6.04% Joint Ventures 40.0% 360 $191,770 $112,000 $35,070 $44,700 $143,398 $63,628 $35,070 $11,583 6.04% Total In-Construction Communities 88.9% 1,942 $1,004,844 $630,000 $330,144 $44,700 $694,324 $319,366 $330,144 $61,662 6.14% 2020 MCRC Remaining Capital $79,725 $79,725 - Thereafter MCRC Remaining Capital 230,795 230,795 - Total Remaining Capital $310,520 $310,520 $0 Percentage Units NOI* Leased Lease-Up Communities Delivered 3Q 2020 3Q 2020 The Emery 326 ($5) 75.8% Lease-Up Communities 326 ($5) 75.8% Project Capitalization - Total Capital as of 3Q 2020 Development Schedule

2015/2016 Achievements - Development Pipeline Activity and Future Development Starts 3Q 2020 Notes: NOI amounts are projected only. See Information About Net Operating Income (NOI) on page 42. See supporting “Pipeline Activity and Future Development Starts” notes on page 39. $ in millions (unaudited) 29 CLI Multifamily Portfolio Projected Projected RRT Nominal % Leased As of: Actual/Projected Projected Stabilized Share of Stabilized Ownership 9/30/2020 Initial Leasing Units Yield NOI NOI After Debt Service 2020 Deliveries The Emery 100.0% 75.8% 1Q 2020 326 6.06% $6.1 $3.4 Total 2020 Deliveries 100.0% 326 6.06% $6.1 $3.4 2021 Deliveries The Upton 100.0% 1Q 2021 193 5.94% $5.9 $3.2 Capstone at Port Imperial 40.0% 1Q 2021 360 6.04% 11.6 2.7 RiverHouse 9 100.0% 1Q 2021 313 6.37% 9.1 5.2 Total 2021 Deliveries 75.1% 866 6.14% $26.6 $11.1 2022 Deliveries The Charlotte 100.0% 1Q 2022 750 6.16% $28.9 $15.4 Total 2022 Deliveries 100.0% 750 5.97% $28.9 $15.4 Total 88.9% 1,942 6.14% $61.6 $29.9 Future Developments Location Units Hudson Waterfront Plaza 8 Jersey City, NJ 680 Urby Harborside - Future Phases Jersey City, NJ 1,546 Plaza 9 Jersey City, NJ 487 107 Morgan Jersey City, NJ 800 Liberty Landing Phase 1 Jersey City, NJ 265 Liberty Landing – Future Phases Jersey City, NJ 585 PI South – Park Parcel Weehawken, NJ 245 PI South – Building 16 Weehawken, NJ 204 PI South – Office 1/3 (1) Weehawken, NJ 290 PI South – Building 2 Weehawken, NJ 245 PI North – Riverbend 6 West New York, NJ 607 PI North – Building J West New York, NJ 141 PI North – Building I West New York, NJ 224 Subtotal – Hudson Waterfront 6,319 Subtotal – Northeast Corridor 987 Subtotal – Boston Metro 1,164 Subtotal – Washington D.C. 738 Subtotal – New York 299 Total Future Start Communities 9,507

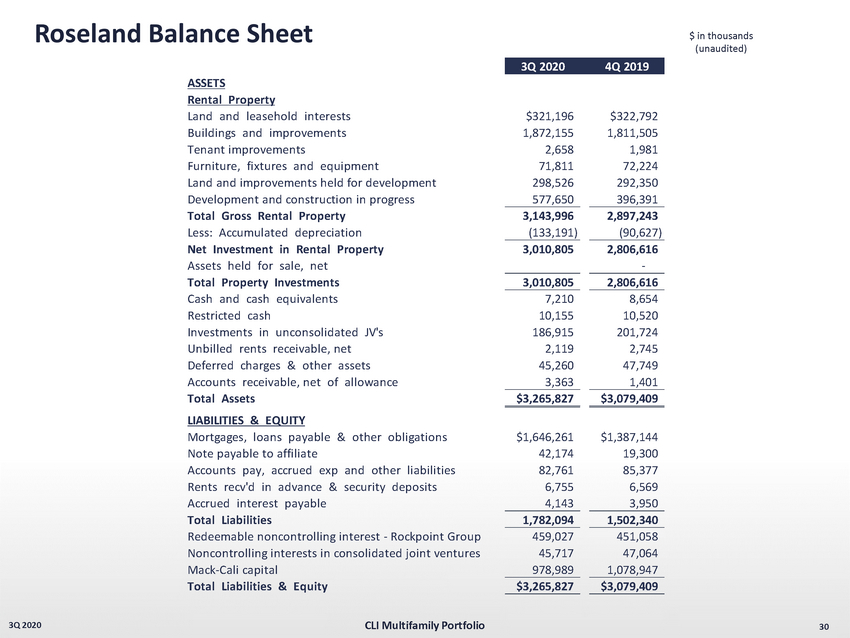

Roseland Balance Sheet 30 3Q 2020 $ in thousands (unaudited) CLI Multifamily Portfolio 3Q 2020 4Q 2019 ASSETS Rental Property Land and leasehold interests $321,196 $322,792 Buildings and improvements 1,872,155 1,811,505 Tenant improvements 2,658 1,981 Furniture, fixtures and equipment 71,811 72,224 Land and improvements held for development 298,526 292,350 Development and construction in progress 577,650 396,391 Total Gross Rental Property 3,143,996 2,897,243 Less: Accumulated depreciation (133,191) (90,627) Net Investment in Rental Property 3,010,805 2,806,616 Assets held for sale, net - Total Property Investments 3,010,805 2,806,616 Cash and cash equivalents 7,210 8,654 Restricted cash 10,155 10,520 Investments in unconsolidated JV's 186,915 201,724 Unbilled rents receivable, net 2,119 2,745 Deferred charges & other assets 45,260 47,749 Accounts receivable, net of allowance 3,363 1,401 Total Assets $3,265,827 $3,079,409 LIABILITIES & EQUITY Mortgages, loans payable & other obligations $1,646,261 $1,387,144 Note payable to affiliate 42,174 19,300 Accounts pay, accrued exp and other liabilities 82,761 85,377 Rents recv'd in advance & security deposits 6,755 6,569 Accrued interest payable 4,143 3,950 Total Liabilities 1,782,094 1,502,340 Redeemable noncontrolling interest - Rockpoint Group 459,027 451,058 Noncontrolling interests in consolidated joint ventures 45,717 47,064 Mack-Cali capital 978,989 1,078,947 Total Liabilities & Equity $3,265,827 $3,079,409

Roseland Income Statement 31 3Q 2020 $ in thousands (unaudited) CLI Multifamily Portfolio 3Q 2020 2Q 2020 1Q 2020 4Q 2019 3Q 2019 REVENUES Base rents $29,238 $31,190 $33,013 $34,919 $34,232 Escalation and recoveries from tenants 1,311 1,218 1,080 1,223 1,377 Real estate services 2,864 2,711 2,949 2,995 1,450 Parking income 2,439 1,496 2,990 3,366 3,240 Hotel income 893 772 1,625 4,139 3,325 Other income 913 847 1,189 1,056 942 Total revenues $37,658 $38,234 $42,846 $47,698 $44,566 EXPENSES Real estate taxes $5,675 $6,312 $6,283 $6,082 $5,664 Utilities 1,562 1,376 1,633 1,216 1,712 Operating services 10,267 8,172 8,290 8,982 9,739 Real estate service expenses 3,258 3,035 3,673 3,703 1,961 General and administrative 6,010 3,250 2,893 3,377 3,025 Depreciation and amortization 15,551 15,309 21,067 22,564 17,228 Property impairments 36,582 - - - - Land and other impairments - 4,856 175 1,035 2,137 Total expenses $78,905 $42,310 $44,014 $46,959 $41,466 Operating Income ($41,247) ($4,076) ($1,168) $739 $3,100 OTHER (EXPENSE) INCOME Interest expense ($9,067) ($9,164) ($8,909) ($10,363) ($10,330) Interest and other investment income (loss) 2 6 1 844 152 Equity in earnings (loss) of unconsolidated joint ventures 880 (569) (590) 2,297 (420) Realized gains (losses) and unrealized losses on disposition - - - 113,787 - Gane on sale of land/other - - 764 (44) 296 Total other income (expense) ($8,185) ($9,727) ($8,734) $106,521 ($10,302) Net income (loss) ($49,432) ($13,803) ($9,902) $107,260 ($7,202) Noncontrolling interest in consolidated joint ventures $798 $447 $176 $140 $405 Redeemable noncontrolling interest (6,016) (6,016) (6,016) (6,015) (6,015) Net income (loss) available to common shareholders ($54,650) ($19,372) ($15,742) $101,385 ($12,812)

32 Office Portfolio 3Q 2020 32

Property Listing 33 3Q 2020 CLI Office Portfolio Notes: See supporting “Property Listing” notes on page 40. Avg. Base Rent Building Location Total SF Leased SF % Leased + Escalations (1) SF % Total In-Place Rent 101 Hudson Jersey City, NJ 1,246,283 1,024,901 82.2% $39.15 21,135 2% $47.01 Harborside 2 & 3 Jersey City, NJ 1,487,222 1,199,259 80.6% 39.40 - 0% - Harborside 4A Jersey City, NJ 231,856 231,856 100.0% 35.66 - 0% - Harborside 5 Jersey City, NJ 977,225 547,868 56.1% 41.12 2,551 0% 43.43 111 River Street Hoboken, NJ 566,215 463,677 81.9% 41.37 - 0% - Total Waterfront 4,508,801 3,467,561 76.9% $39.65 23,686 1% $46.62 Harborside 1 (2) Jersey City, NJ 399,578 - N/A N/A N/A N/A N/A Total Waterfront (including Out of Service) 4,908,379 3,467,561 70.6% $39.65 23,686 0% $46.62 101 Wood Avenue S Iselin, NJ 262,841 262,841 100.0% 34.86 - 0% - 99 Wood Avenue S Iselin, NJ 271,988 222,287 81.7% 37.23 - 0% - 581 Main Street (3) Woodbridge, NJ 200,000 200,000 100.0% 34.43 - 0% - 333 Thornall Street Edison, NJ 196,128 174,381 88.9% 36.67 - 0% - 343 Thornall Street Edison, NJ 195,709 180,698 92.3% 37.24 - 0% - 150 JFK Parkway (3) Short Hills, NJ 247,476 158,741 64.1% 37.68 23,521 10% 39.05 51 JFK Parkway (3) Short Hills, NJ 260,741 223,700 85.8% 54.43 - 0% - 101 JFK Parkway (3) Short Hills, NJ 197,196 194,111 98.4% 43.90 - 0% - 103 JFK Parkway (3) Short Hills, NJ 123,000 123,000 100.0% 43.10 - 0% - Total Class A Suburban 1,955,079 1,739,759 89.0% $39.89 23,521 1% $39.05 7 Giralda Farms (3) Madison, NJ 236,674 142,136 60.1% 36.48 - 0% - 4 Gatehall Drive (3) Parsippany, NJ 248,480 147,778 59.5% 28.78 - 0% - 7 Campus Drive (3) Parsippany, NJ 154,395 69,810 45.2% 26.40 - 0% - 100 Schultz Drive Red Bank, NJ 100,000 28,506 28.5% 32.10 - 0% - 200 Schultz Drive Red Bank, NJ 102,018 87,579 85.8% 30.23 - 0% - 1 River Center 1 Red Bank, NJ 122,594 119,622 97.6% 29.04 7,707 6% 26.85 1 River Center 2 Red Bank, NJ 120,360 120,360 100.0% 27.77 - 0% - 1 River Center 3 Red Bank, NJ 194,518 76,572 39.4% 31.28 - 0% - 100 Overlook Center Princeton, NJ 149,600 140,583 94.0% 31.85 - 0% - 5 Vaughn Drive (4) Princeton, NJ 98,500 30,870 31.3% 31.06 - 0% - 23 Main Street (5) Holmdel, NJ 350,000 350,000 100.0% 18.39 - 0% - Total Suburban 1,877,139 1,313,816 70.0% $27.30 7,707 0% $26.85 Total Core Office Portfolio (6) 8,341,019 6,521,136 78.2% $37.23 54,914 1% $40.60 2020 Expirations

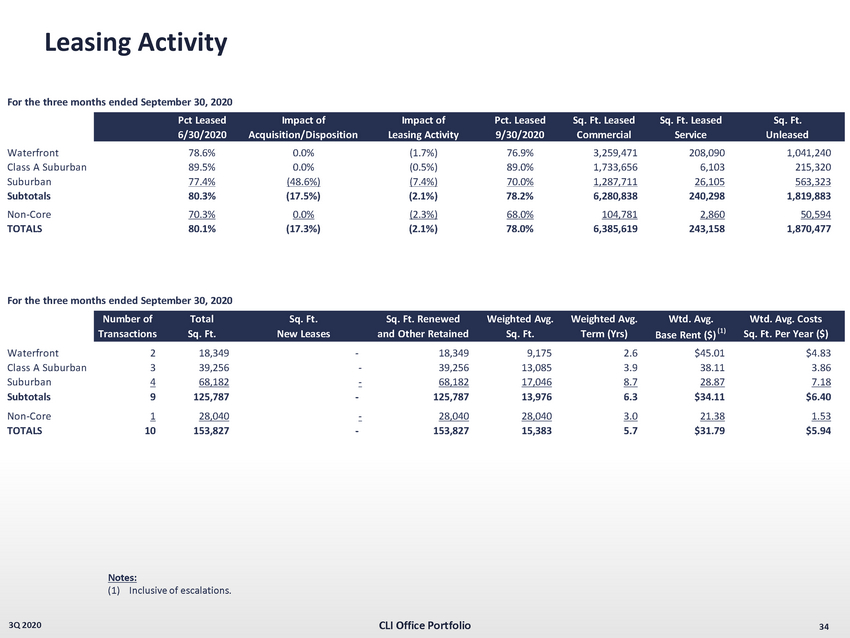

Leasing Activity 34 3Q 2020 Notes: (1) Inclusive of escalations. CLI Office Portfolio For the three months ended September 30, 2020 Pct Leased Impact of Impact of Pct. Leased Sq. Ft. Leased Sq. Ft. Leased Sq. Ft. 6/30/2020 Acquisition/Disposition Leasing Activity 9/30/2020 Commercial Service Unleased Waterfront 78.6% 0.0% (1.7%) 76.9% 3,259,471 208,090 1,041,240 Class A Suburban 89.5% 0.0% (0.5%) 89.0% 1,733,656 6,103 215,320 Suburban 77.4% (48.6%) (7.4%) 70.0% 1,287,711 26,105 563,323 Subtotals 80.3% (17.5%) (2.1%) 78.2% 6,280,838 240,298 1,819,883 Non-Core 70.3% 0.0% (2.3%) 68.0% 104,781 2,860 50,594 TOTALS 80.1% (17.3%) (2.1%) 78.0% 6,385,619 243,158 1,870,477 For the three months ended September 30, 2020 Number of Total Sq. Ft. Sq. Ft. Renewed Weighted Avg. Weighted Avg. Wtd. Avg. Wtd. Avg. Costs Transactions Sq. Ft. New Leases and Other Retained Sq. Ft. Term (Yrs) Base Rent ($) (1) Sq. Ft. Per Year ($) Waterfront 2 18,349 - 18,349 9,175 2.6 $45.01 $4.83 Class A Suburban 3 39,256 - 39,256 13,085 3.9 38.11 3.86 Suburban 4 68,182 - 68,182 17,046 8.7 28.87 7.18 Subtotals 9 125,787 - 125,787 13,976 6.3 $34.11 $6.40 Non-Core 1 28,040 - 28,040 28,040 3.0 21.38 1.53 TOTALS 10 153,827 - 153,827 15,383 5.7 $31.79 $5.94

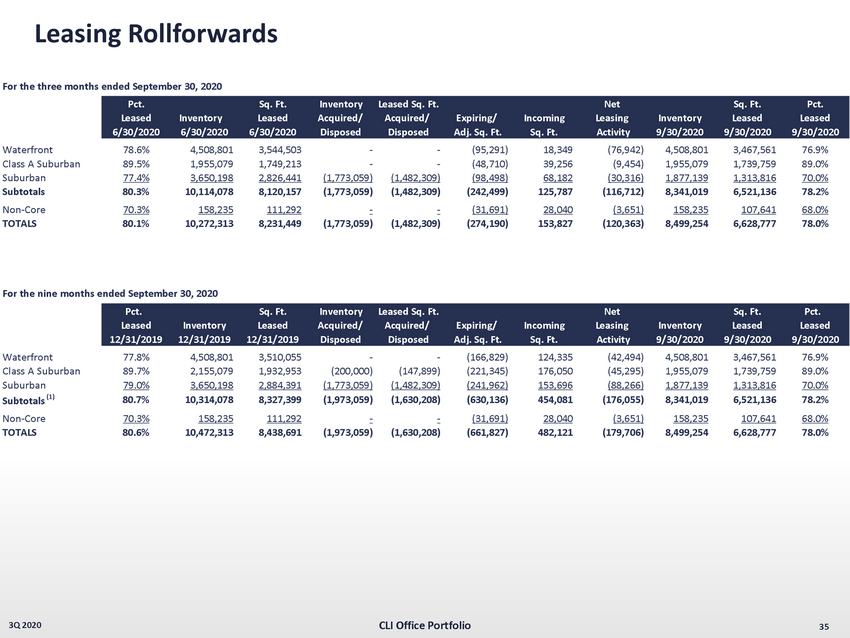

35 3Q 2020 Leasing Rollforwards CLI Office Portfolio For the three months ended September 30, 2020 Pct. Sq. Ft. Inventory Leased Sq. Ft. Net Sq. Ft. Pct. Leased Inventory Leased Acquired/ Acquired/ Expiring/ Incoming Leasing Inventory Leased Leased 6/30/2020 6/30/2020 6/30/2020 Disposed Disposed Adj. Sq. Ft. Sq. Ft. Activity 9/30/2020 9/30/2020 9/30/2020 Waterfront 78.6% 4,508,801 3,544,503 - - (95,291) 18,349 (76,942) 4,508,801 3,467,561 76.9% Class A Suburban 89.5% 1,955,079 1,749,213 - - (48,710) 39,256 (9,454) 1,955,079 1,739,759 89.0% Suburban 77.4% 3,650,198 2,826,441 (1,773,059) (1,482,309) (98,498) 68,182 (30,316) 1,877,139 1,313,816 70.0% Subtotals 80.3% 10,114,078 8,120,157 (1,773,059) (1,482,309) (242,499) 125,787 (116,712) 8,341,019 6,521,136 78.2% Non-Core 70.3% 158,235 111,292 - - (31,691) 28,040 (3,651) 158,235 107,641 68.0% TOTALS 80.1% 10,272,313 8,231,449 (1,773,059) (1,482,309) (274,190) 153,827 (120,363) 8,499,254 6,628,777 78.0% For the nine months ended September 30, 2020 Pct. Sq. Ft. Inventory Leased Sq. Ft. Net Sq. Ft. Pct. Leased Inventory Leased Acquired/ Acquired/ Expiring/ Incoming Leasing Inventory Leased Leased 12/31/2019 12/31/2019 12/31/2019 Disposed Disposed Adj. Sq. Ft. Sq. Ft. Activity 9/30/2020 9/30/2020 9/30/2020 Waterfront 77.8% 4,508,801 3,510,055 - - (166,829) 124,335 (42,494) 4,508,801 3,467,561 76.9% Class A Suburban 89.7% 2,155,079 1,932,953 (200,000) (147,899) (221,345) 176,050 (45,295) 1,955,079 1,739,759 89.0% Suburban 79.0% 3,650,198 2,884,391 (1,773,059) (1,482,309) (241,962) 153,696 (88,266) 1,877,139 1,313,816 70.0% Subtotals (1) 80.7% 10,314,078 8,327,399 (1,973,059) (1,630,208) (630,136) 454,081 (176,055) 8,341,019 6,521,136 78.2% Non-Core 70.3% 158,235 111,292 - - (31,691) 28,040 (3,651) 158,235 107,641 68.0% TOTALS 80.6% 10,472,313 8,438,691 (1,973,059) (1,630,208) (661,827) 482,121 (179,706) 8,499,254 6,628,777 78.0%

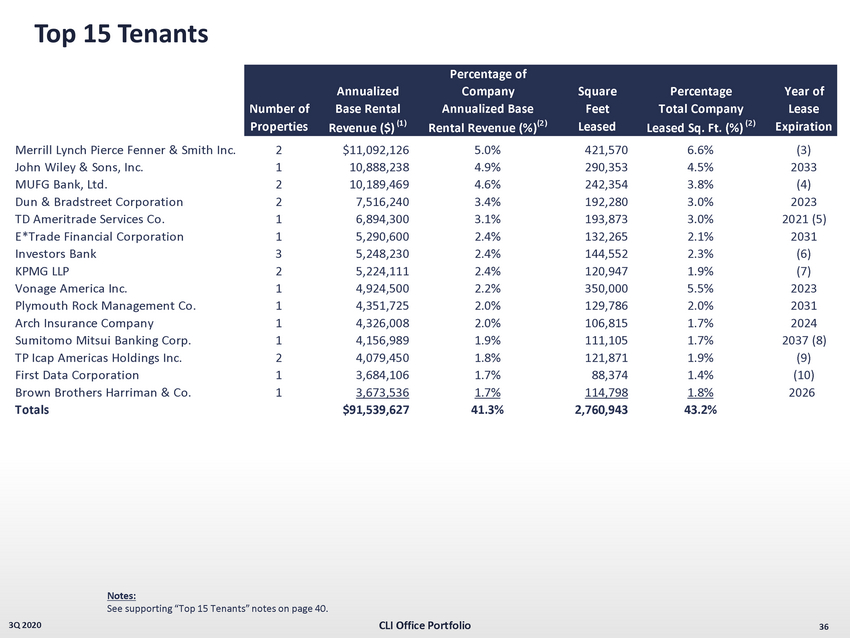

36 3Q 2020 Top 15 Tenants Notes: See supporting “Top 15 Tenants” notes on page 40. CLI Office Portfolio Percentage of Annualized Company Square Percentage Year of Number of Base Rental Annualized Base Feet Total Company Lease Properties Revenue ($) (1) Rental Revenue (%) (2) Leased Leased Sq. Ft. (%) (2) Expiration Merrill Lynch Pierce Fenner & Smith Inc. 2 $11,092,126 5.0% 421,570 6.6% (3) John Wiley & Sons, Inc. 1 10,888,238 4.9% 290,353 4.5% 2033 MUFG Bank, Ltd. 2 10,189,469 4.6% 242,354 3.8% (4) Dun & Bradstreet Corporation 2 7,516,240 3.4% 192,280 3.0% 2023 TD Ameritrade Services Co. 1 6,894,300 3.1% 193,873 3.0% 2021 (5) E*Trade Financial Corporation 1 5,290,600 2.4% 132,265 2.1% 2031 Investors Bank 3 5,248,230 2.4% 144,552 2.3% (6) KPMG LLP 2 5,224,111 2.4% 120,947 1.9% (7) Vonage America Inc. 1 4,924,500 2.2% 350,000 5.5% 2023 Plymouth Rock Management Co. 1 4,351,725 2.0% 129,786 2.0% 2031 Arch Insurance Company 1 4,326,008 2.0% 106,815 1.7% 2024 Sumitomo Mitsui Banking Corp. 1 4,156,989 1.9% 111,105 1.7% 2037 (8) TP Icap Americas Holdings Inc. 2 4,079,450 1.8% 121,871 1.9% (9) First Data Corporation 1 3,684,106 1.7% 88,374 1.4% (10) Brown Brothers Harriman & Co. 1 3,673,536 1.7% 114,798 1.8% 2026 Totals $91,539,627 41.3% 2,760,943 43.2%

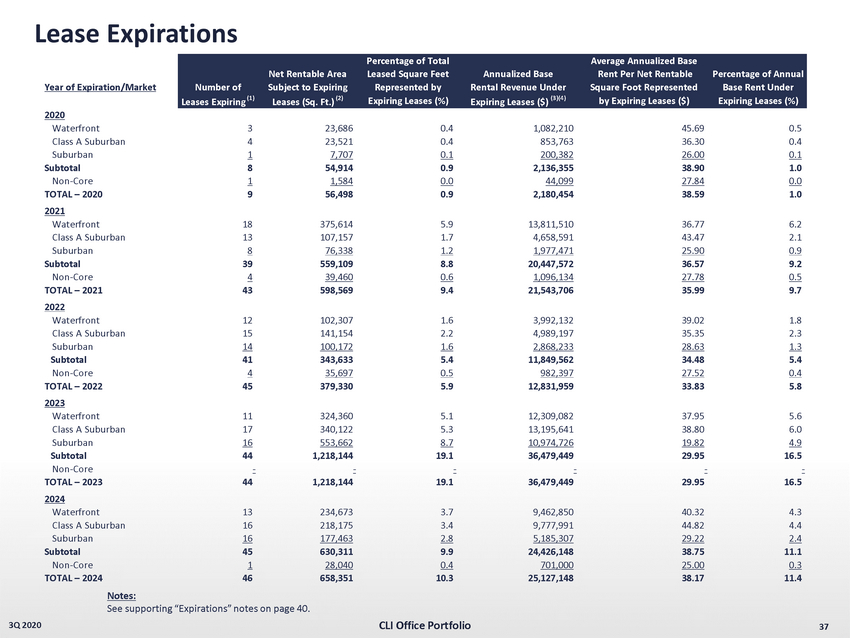

37 3Q 2020 Lease Expirations Notes: See supporting “Expirations” notes on page 40. CLI Office Portfolio Percentage of Total Average Annualized Base Net Rentable Area Leased Square Feet Annualized Base Rent Per Net Rentable Percentage of Annual Year of Expiration/Market Number of Subject to Expiring Represented by Rental Revenue Under Square Foot Represented Base Rent Under Leases Expiring (1) Leases (Sq. Ft.) (2) Expiring Leases (%) Expiring Leases ($) (3)(4) by Expiring Leases ($) Expiring Leases (%) 2020 Waterfront 3 23,686 0.4 1,082,210 45.69 0.5 Class A Suburban 4 23,521 0.4 853,763 36.30 0.4 Suburban 1 7,707 0.1 200,382 26.00 0.1 Subtotal 8 54,914 0.9 2,136,355 38.90 1.0 Non-Core 1 1,584 0.0 44,099 27.84 0.0 TOTAL – 2020 9 56,498 0.9 2,180,454 38.59 1.0 2021 Waterfront 18 375,614 5.9 13,811,510 36.77 6.2 Class A Suburban 13 107,157 1.7 4,658,591 43.47 2.1 Suburban 8 76,338 1.2 1,977,471 25.90 0.9 Subtotal 39 559,109 8.8 20,447,572 36.57 9.2 Non-Core 4 39,460 0.6 1,096,134 27.78 0.5 TOTAL – 2021 43 598,569 9.4 21,543,706 35.99 9.7 2022 Waterfront 12 102,307 1.6 3,992,132 39.02 1.8 Class A Suburban 15 141,154 2.2 4,989,197 35.35 2.3 Suburban 14 100,172 1.6 2,868,233 28.63 1.3 Subtotal 41 343,633 5.4 11,849,562 34.48 5.4 Non-Core 4 35,697 0.5 982,397 27.52 0.4 TOTAL – 2022 45 379,330 5.9 12,831,959 33.83 5.8 2023 Waterfront 11 324,360 5.1 12,309,082 37.95 5.6 Class A Suburban 17 340,122 5.3 13,195,641 38.80 6.0 Suburban 16 553,662 8.7 10,974,726 19.82 4.9 Subtotal 44 1,218,144 19.1 36,479,449 29.95 16.5 Non-Core - - - - - - TOTAL – 2023 44 1,218,144 19.1 36,479,449 29.95 16.5 2024 Waterfront 13 234,673 3.7 9,462,850 40.32 4.3 Class A Suburban 16 218,175 3.4 9,777,991 44.82 4.4 Suburban 16 177,463 2.8 5,185,307 29.22 2.4 Subtotal 45 630,311 9.9 24,426,148 38.75 11.1 Non-Core 1 28,040 0.4 701,000 25.00 0.3 TOTAL – 2024 46 658,351 10.3 25,127,148 38.17 11.4

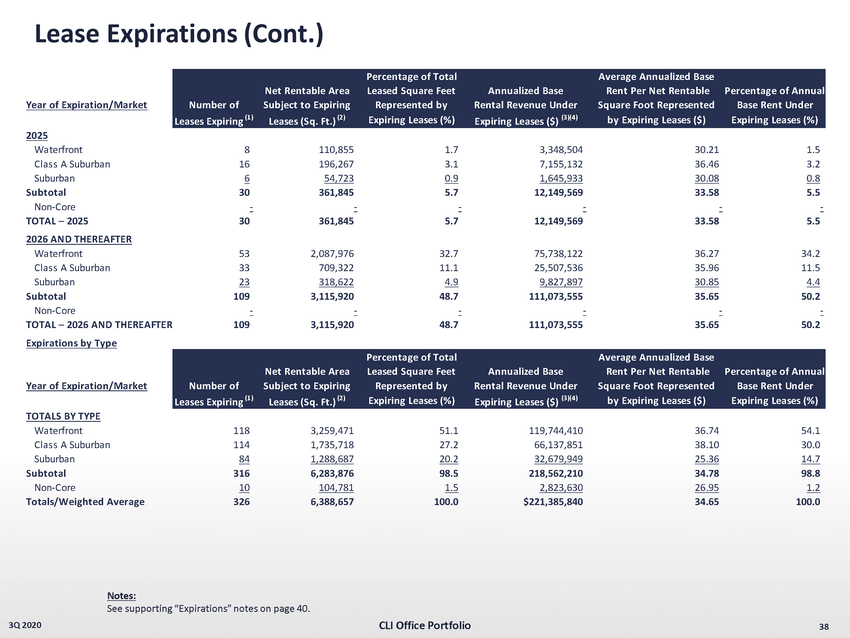

38 3Q 2020 Lease Expirations (Cont.) Notes: See supporting “Expirations” notes on page 40. CLI Office Portfolio Percentage of Total Average Annualized Base Net Rentable Area Leased Square Feet Annualized Base Rent Per Net Rentable Percentage of Annual Year of Expiration/Market Number of Subject to Expiring Represented by Rental Revenue Under Square Foot Represented Base Rent Under Leases Expiring (1) Leases (Sq. Ft.) (2) Expiring Leases (%) Expiring Leases ($) (3)(4) by Expiring Leases ($) Expiring Leases (%) 2025 Waterfront 8 110,855 1.7 3,348,504 30.21 1.5 Class A Suburban 16 196,267 3.1 7,155,132 36.46 3.2 Suburban 6 54,723 0.9 1,645,933 30.08 0.8 Subtotal 30 361,845 5.7 12,149,569 33.58 5.5 Non-Core - - - - - - TOTAL – 2025 30 361,845 5.7 12,149,569 33.58 5.5 2026 AND THEREAFTER Waterfront 53 2,087,976 32.7 75,738,122 36.27 34.2 Class A Suburban 33 709,322 11.1 25,507,536 35.96 11.5 Suburban 23 318,622 4.9 9,827,897 30.85 4.4 Subtotal 109 3,115,920 48.7 111,073,555 35.65 50.2 Non-Core - - - - - - TOTAL – 2026 AND THEREAFTER 109 3,115,920 48.7 111,073,555 35.65 50.2 Expirations by Type Percentage of Total Average Annualized Base Net Rentable Area Leased Square Feet Annualized Base Rent Per Net Rentable Percentage of Annual Year of Expiration/Market Number of Subject to Expiring Represented by Rental Revenue Under Square Foot Represented Base Rent Under Leases Expiring (1) Leases (Sq. Ft.) (2) Expiring Leases (%) Expiring Leases ($) (3)(4) by Expiring Leases ($) Expiring Leases (%) TOTALS BY TYPE Waterfront 118 3,259,471 51.1 119,744,410 36.74 54.1 Class A Suburban 114 1,735,718 27.2 66,137,851 38.10 30.0 Suburban 84 1,288,687 20.2 32,679,949 25.36 14.7 Subtotal 316 6,283,876 98.5 218,562,210 34.78 98.8 Non-Core 10 104,781 1.5 2,823,630 26.95 1.2 Totals/Weighted Average 326 6,388,657 100.0 $221,385,840 34.65 100.0

Appendix Key Financial Metrics - (Page 6 ) (1) Funds from operations (“FFO”) is calculated in accordance with the definition of the National Association of Real Estate Investment Trusts (NAREIT) . See p . 16 “Information About FFO, Core FFO & AFFO” . (2) Includes any outstanding preferred units presented on a converted basis into common units, noncontrolling interests in consolidated joint ventures and redeemable noncontrolling interests . (3) Net Debt to EBITDA results are represent completion of the Liberty Towers - Overlook Ridge 1031 exchange . Balance Sheet - (Page 9 ) (1) Includes mark - to - market lease intangible net assets of $ 75 , 610 and mark - to - market lease intangible net liabilities of $ 35 , 342 as of 3 Q 2020 . (2) Includes Prepaid Expenses and Other Assets attributable to Roseland of $ 26 , 647 as follows : ( i ) deposits of $ 9 , 695 , (ii) other receivable of $ 5 , 058 , (iii) pre - development costs of $ 4 , 718 , (iv) other prepaids/assets of $ 4 , 473 , and (v) prepaid taxes of $ 2 , 703 . Debt Summary & Future Repayments Schedule - (Page 19 ) (1) The actual weighted average LIBOR rate for the Company’s outstanding variable rate debt was 0 . 16 percent as of September 30 , 2020 , plus the applicable spread . (2) Excludes amortized deferred financing costs primarily pertaining to the Company’s unsecured revolving credit facility which amounted to $ 960 , 238 for the three months ended September 30 , 2020 . Debt Profile - (Pages 20 - 21) (1) Effective rate of debt, including deferred financing costs, comprised of the cost of terminated treasury lock agreements (if any ), debt initiation costs, mark - to - market adjustment of acquired debt and other transaction costs, as applicable. (2) Senior unsecured debt is rated BB - /Ba2/BB by S&P, Moody’s and Fitch respectively. (3) Cost of terminated treasury lock agreements (if any), offering and other transaction costs and the discount/premium on the no tes , as applicable. (4) Subsequent to quarter - end, the Company executed a term sheet for a new $165 million, seven - year loan with its current lender on the BLVD 475 ( f.k.a . Monaco) to replace its existing debt effective in 4Q20 Unconsolidated Joint Ventures - (Page 23) (1) Amounts represent the Company’s share based on ownership percentage. (2) Unconsolidated Joint Venture reconciliation is as follows: Operating Communities - (Page 26) (1) Unconsolidated joint venture income represented at 100% venture NOI. See Information on Net Operating Income (NOI) on page 42 . (2) As of September 30, 2020, Priority Capital included Metropolitan at $20,914,422 (Prudential). (3) Excludes approximately 128,000 SF of ground floor retail. In - Construction Communities - (Page 28) (1) Represents maximum loan proceeds. (2) Represents development costs funded with debt or capital as of September 30, 2020. Pipeline Activity and Future Development Starts - (Page 29) (1) Currently approved for approximately 290,000 square feet of office space. 39 3Q 2020 3Q 2020 Equity in Earnings of Unconsolidated Joint Ventures ($1,373) Unconsolidated Joint Venture Funds from Operations 5,364 Joint Venture Share of Add - Back of Real Estate - Related Depreciation 3,991 Minority Interest in Consolidated Joint Venture Share of Depreciation (661) EBITDA Depreciation Add - Back $3,330 $ in thousands

Appendix - Continued Property Listing - (Page 33) (1) Includes annualized base rental revenue plus escalations for square footage leased to commercial and retail tenants only. Ex clu des leases for amenity, parking and month - to - month tenants. Annualized base rental revenue plus escalations is based on actual September 2020 billings times 12. For leases whose rent commences after October 1, 2020 annualized base rental revenue is based on the first full month’s billing times 12. As annualized base rental revenue is not derived from historical GAAP results, historical results may differ from those set forth above. (2) Harborside 1 was taken out of service in 4Q19. (3) These assets, in addition to a 158,235 SF non - core asset, are under contract for sale for total gross proceeds in a range of $37 5 - $390 million. These assets total 1,826,197 square feet. (4) Subsequent to quarter - end, on October 21, 2020, the Company completed the sale of 5 Vaughn Drive, a 98,500 square - foot office building in Pri nceton, NJ, for a gross purchase price of $7.5 million (5) Average base rents + escalations reflect rental values on a triple net basis. (6) Excludes non - core holdings targeted for sale at 158,235 SF; excludes consolidated repositionings taken offline totaling 399,578 SF. Total consolidated office portfolio of 8,898,832 SF. Top 15 Tenants - (Page 36) (1) Annualized base rental revenue is based on actual September 2020 billings times 12. For leases whose rent commences after Oct obe r 1, 2020, annualized base rental revenue is based on the first full month’s billing times 12. As annualized base rental revenue is not derived from historical GAAP results, historical results may differ from t hos e set forth above. (2) Represents the percentage of space leased and annual base rental revenue to commercial tenants only. (3) 33,363 square feet expire in 2021; 388,207 square feet expire in 2027. (4) 5,004 square feet expire in 2021; 237,350 square feet expire in 2029. (5) 149,651 square feet expire December 31, 2020; 44,222 square feet expire December 31, 2021. (6) 5,256 square feet expire in 2022; 82,936 square feet expire in 2026; 56,360 square feet expire in 2030. (7) 66,606 square feet expire in 2024; 54,341 square feet expire in 2026. (8) Space expires December 31, 2036. (9) 63,372 square feet expire in 2023; 21,112 square feet expire in 2025; 37,387 square feet expire in 2033. (10) 8,014 square feet expire in December 31, 2026; 80,360 square feet expires in 2029. Expirations - (Pages 37 - 38) (1) Includes office & standalone retail property tenants only. Excludes leases for amenity, retail, parking & month - to - month tenants . Some tenants have multiple leases. (2) Reconciliation to Company’s total net rentable square footage is as follows: (3) Annualized base rental revenue is based on actual September 2020 billings times 12. For leases whose rent commences after Oct obe r 1, 2020 annualized base rental revenue is based on the first full month’s billing times 12. As annualized base rental revenue is not derived from historical GAAP results, historical results may differ from t hos e set forth above. (4) Includes leases in effect as of the period end date, some of which have commencement dates in the future, and leases expiring Se ptember 30, 2020 aggregating 25,712 square feet and representing annualized base rent of $811,762 for which no new leases were signed. 40 3Q 2020 Square Feet Square footage leased to commercial tenants 6,385,619 Square footage used for corporate offices, management offices, building use, retail tenants, food services, other ancillary service tenants and occupancy adjustments 243,158 Square footage unleased 1,870,477 Total net rentable square footage (excluding ground leases) 8,499,254