UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrant x | |

| Filed by a Party other than the Registrant ¨ | |

| Check the appropriate box: | |

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material under §240.14a-12 |

|

MACK-CALI REALTY CORPORATION |

|

(Name of Registrant as Specified In Its Charter)

|

|

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

|

| Payment of Filing Fee (Check the appropriate box): |

| x | No fee required. | |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) |

Title of each class of securities to which transaction applies: | |

| (2) |

Aggregate number of securities to which transaction applies: | |

| (3) |

Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) |

Proposed maximum aggregate value of transaction: | |

| (5) |

Total fee paid: | |

| ¨ | Fee paid previously with preliminary materials. | |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) |

Amount Previously Paid: | |

| (2) |

Form, Schedule or Registration Statement No.: | |

| (3) |

Filing Party: | |

| (4) |

Date Filed: | |

|

DRAFT – FOR DISCUSSION PURPOSES ONLY Mack-Cali Realty May 2020 Corporation |

|

Disclaimer 2 This presentation should be read in connection with our Quarterly Report on Form 10-Q for the quarter ended March 31, 2020. Statements made in this presentation may be forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements can be identified by the use of words such as "may," "will," "plan," "potential," "projected," "should," "expect," "anticipate," "estimate," "target," "continue" or comparable terminology. Forward-looking statements are inherently subject to certain risks, trends and uncertainties, many of which we cannot predict with accuracy and some of which we might not even anticipate, and involve factors that may cause actual results to differ materially from those projected or suggested. Readers are cautioned not to place undue reliance on these forward-looking statements and are advised to consider the factors listed above together with the additional factors under the heading "Disclosure Regarding Forward-Looking Statements" and "Risk Factors" in our annual reports on Form 10-K, as may be supplemented or amended by our quarterly reports on Form 10-Q, which are incorporated herein by reference. We assume no obligation to update or supplement forward-looking statements that become untrue because of subsequent events, new information or otherwise. |

|

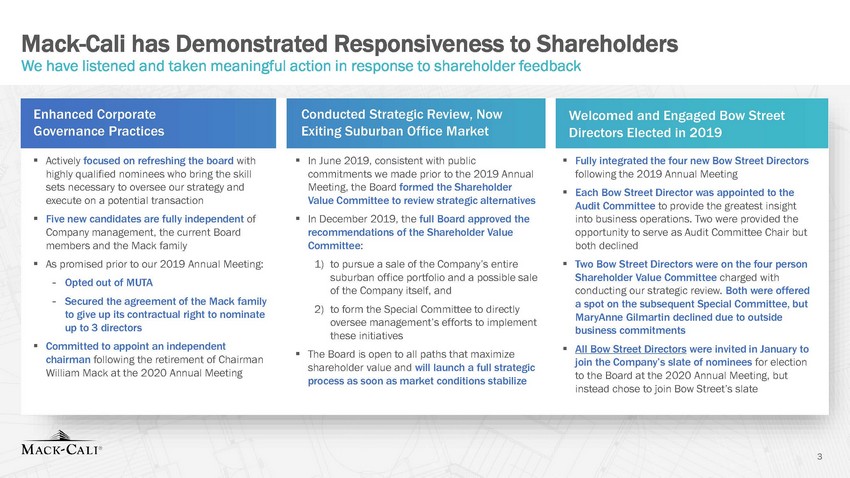

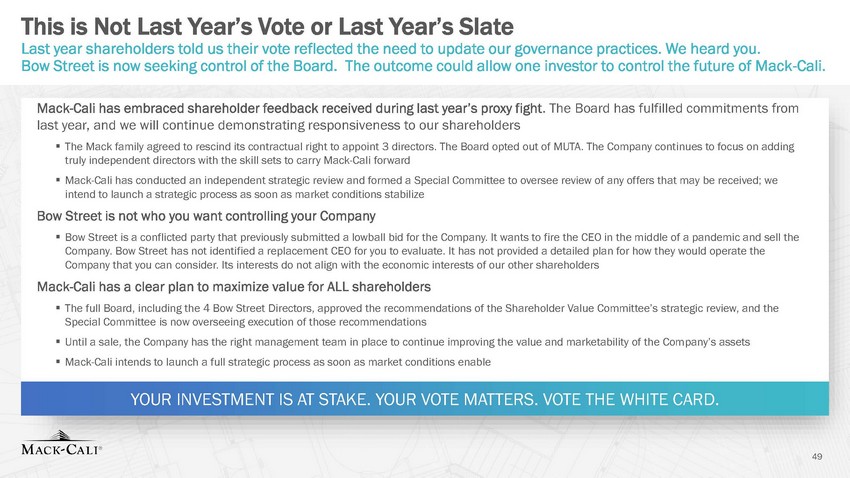

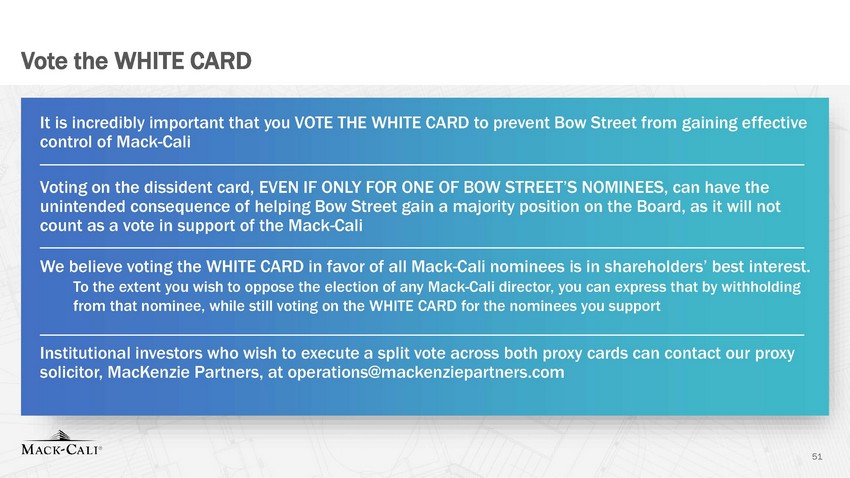

Mack-Cali has Demonstrated Responsiveness to Shareholders We have listened and taken meaningful action in response to shareholder feedback execute on a potential transaction Value Committee to review strategic alternatives Audit Committee to provide the greatest insight of the Company itself, and 2) to form the Special Committee to directly conducting our strategic review. Both were offered to give up its contractual right to nominate MaryAnne Gilmartin declined due to outside these initiatives ▪ The Board is open to all paths that maximize chairman following the retirement of Chairman join the Company’s slate of nominees for election process as soon as market conditions stabilize 3 Enhanced CorporateConducted Strategic Review, NowWelcomed and Engaged Bow Street Governance PracticesExiting Suburban Office MarketDirectors Elected in 2019 ▪ Actively focused on refreshing the board with▪ In June 2019, consistent with public▪ Fully integrated the four new Bow Street Directors highly qualified nominees who bring the skillcommitments we made prior to the 2019 Annualfollowing the 2019 Annual Meeting sets necessary to oversee our strategy andMeeting, the Board formed the Shareholder▪ Each Bow Street Director was appointed to the ▪ Five new candidates are fully independent of▪ In December 2019, the full Board approved theinto business operations. Two were provided the Company management, the current Boardrecommendations of the Shareholder Valueopportunity to serve as Audit Committee Chair but members and the Mack familyCommittee:both declined ▪ As promised prior to our 2019 Annual Meeting:1) to pursue a sale of the Company’s entire▪ Two Bow Street Directors were on the four person -Opted out of MUTAsuburban office portfolio and a possible saleShareholder Value Committee charged with -Secured the agreement of the Mack familya spot on the subsequent Special Committee, but up to 3 directorsoversee management’s efforts to implementbusiness commitments ▪ Committed to appoint an independent▪ All Bow Street Directors were invited in January to William Mack at the 2020 Annual Meetingshareholder value and will launch a full strategicto the Board at the 2020 Annual Meeting, but instead chose to join Bow Street’s slate |

|

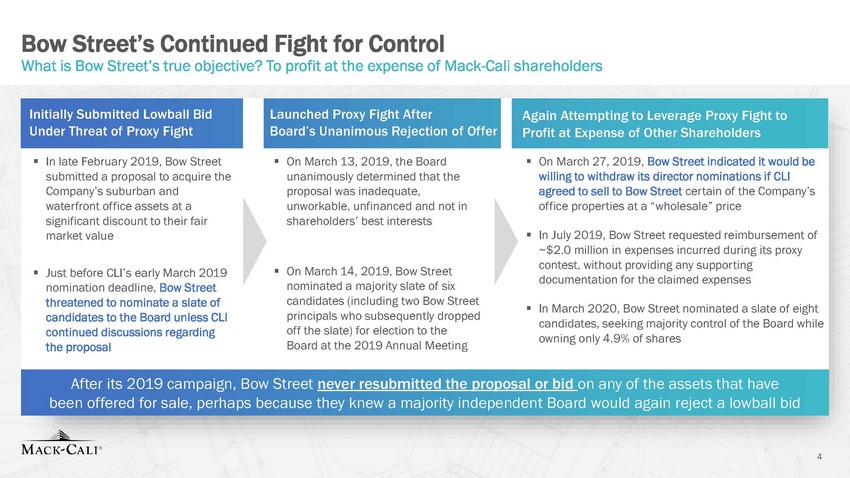

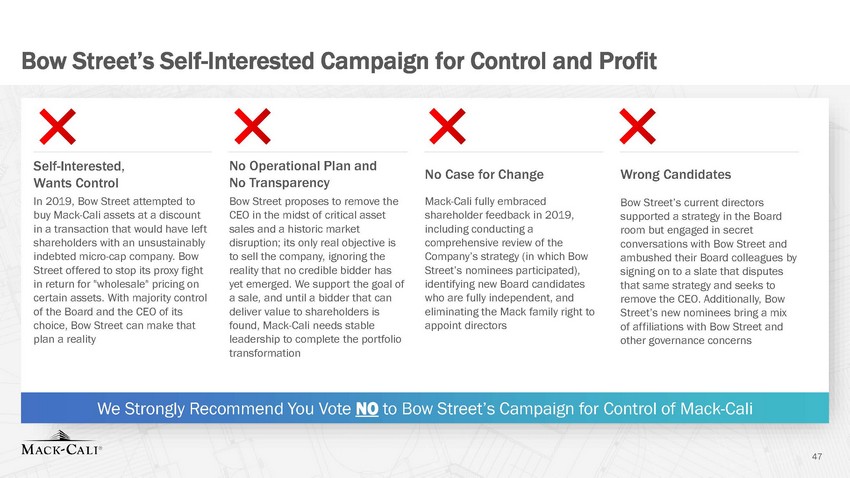

Bow Street’s Continued Fight for Control What is Bow Street’s true objective? To profit at the expense of Mack-Cali shareholders documentation for the claimed expenses nominated a majority slate of six nomination deadline, Bow Street principals who subsequently dropped candidates to the Board unless CLI candidates, seeking majority control of the Board while Board at the 2019 Annual Meeting the proposal 4 Initially Submitted Lowball BidLaunched Proxy Fight AfterAgain Attempting to Leverage Proxy Fight to Under Threat of Proxy FightBoard’s Unanimous Rejection of OfferProfit at Expense of Other Shareholders ▪ In late February 2019, Bow Street▪ On March 13, 2019, the Board▪ On March 27, 2019, Bow Street indicated it would be submitted a proposal to acquire theunanimously determined that thewilling to withdraw its director nominations if CLI Company’s suburban andproposal was inadequate,agreed to sell to Bow Street certain of the Company’s waterfront office assets at aunworkable, unfinanced and not inoffice properties at a “wholesale” price significant discount to their fairshareholders’ best interests market value▪ In July 2019, Bow Street requested reimbursement of ~$2.0 million in expenses incurred during its proxy ▪ Just before CLI’s early March 2019▪ On March 14, 2019, Bow Streetcontest, without providing any supporting threatened to nominate a slate ofcandidates (including two Bow Street▪ In March 2020, Bow Street nominated a slate of eight continued discussions regardingoff the slate) for election to theowning only 4.9% of shares After its 2019 campaign, Bow Street never resubmitted the proposal or bid on any of the assets that have been offered for sale, perhaps because they knew a majority independent Board would again reject a lowball bid |

|

A Walk Through Bow Street’s “Plan” Shows it is Not Grounded in Reality Bow Street’s “plan” is a mix of vague and flawed ideas. Although four Bow Street Directors spent a year on the Board, Bow Street is still not offering specifics about how it would maximize value for all shareholders suburban office assets and recycling capital into higher growth markets and more desirable residential reconsider? fair value residential platform also using $1.2bn in proceeds from asset sales to primarily repay corporate debt 5 “Three-Step Plan” Bow Street’s Vague & Flawed Ideas Mack-Cali’s Pragmatic Perspective 1 Re-align Mack-Cali Portfolio -------------WE ARE x Reconsider development portfolio in context of balance sheet and cash flow strain Create a simplified, more easily understood company with better growth prospects, pivoting away from assets Portfolio evolution has enabled us to dramatically shift the sustainability and quality of our NOI composition Residential developments were completed on time, on budget and leased quickly With only $31mm remaining to complete in-process pipeline, which developments would Bow Street x Restructure residential JV to enable spin-off JV allows spin-off; restructure transfers value away from shareholders and SpinCo would trade at a discount to JV structure enabled our company, which had little access to capital, to create a significant and valuable The terms of the JV are publically disclosed. How does Bow Street propose to restructure this vital and collaborative relationship? At a minimum, requires payment of Rockpoint’s full interest in Roseland plus prepayment penalty of $129mm x Deleverage balance sheet by using proceeds from asset sales to reduce debt Successfully transitioned leverage to primarily secured debt and improved interest coverage ratio, while Bow Street has not identified which additional assets would be targeted for sale |

|

A Walk Through Bow Street’s “Plan” Shows it is Not Grounded in Reality Bow Street’s “plan” is a mix of vague and flawed ideas. Although four Bow Street Directors spent a year on the Board, Bow Street is still not offering specifics about how it would maximize value for all shareholders engaging in discussions with Bow Street and agreeing to join its slate and lend their names to its agenda shareholders in 2019 never raised any concerns about the Company’s management or plan backbone required to challenge the Bow Street already has 4 directors who essentially control the Audit Committee. Shareholders deserve shareholder feedback; Bow Street’s baseless claim of entrenchment ignores that only 3 candidates have retire next year possible; an abrupt change in leadership would result in a demoralized workforce and disruption to serve on New Jersey’s Restart & Recovery Advisory Council to advise state leadership on economic matters period 6 “Three-Step Plan” Bow Street’s Vague & Flawed Ideas Mack-Cali’s Pragmatic Perspective 2 Reconstitute Board -------------WE HAVE 3 New CEO WHO? x Board attempted to unilaterally remove the directors elected by The Board invited all four Bow Street Directors to join the 2020 slate; all four accepted, while secretly x Bow Street’s nominees can effectuate meaningful change, and have the status quo Bow Street Directors voted with other Board members on every matter since their election to the Board and Bow Street’s new candidates have ties that call into question their independence from Bow Street directors who know how to raise issues in the boardroom, rather than only raising concerns from Bow Street in the context of a proxy contest x Legacy Board is entrenched and has gone to extraordinary lengths to protect DeMarco Board continues to improve governance practices and refresh board composition in response to served over 4 years, our Chairman is retiring this year, and two additional longer serving directors plan to x New leadership is required to create value Stability under Mr. DeMarco’s leadership is crucial to complete ongoing transformation as quickly as pending deals and operations x Several Bow Street nominees could serve as interim-CEO during transition Mr. DeMarco, in recognition for his leadership in the community, was appointed by Governor Phil Murphy to Bow Street has not presented any specific candidates for consideration or comparison; current market disruptions make it vital that Mack-Cali shareholders have an opportunity to evaluate a specific candidate |

|

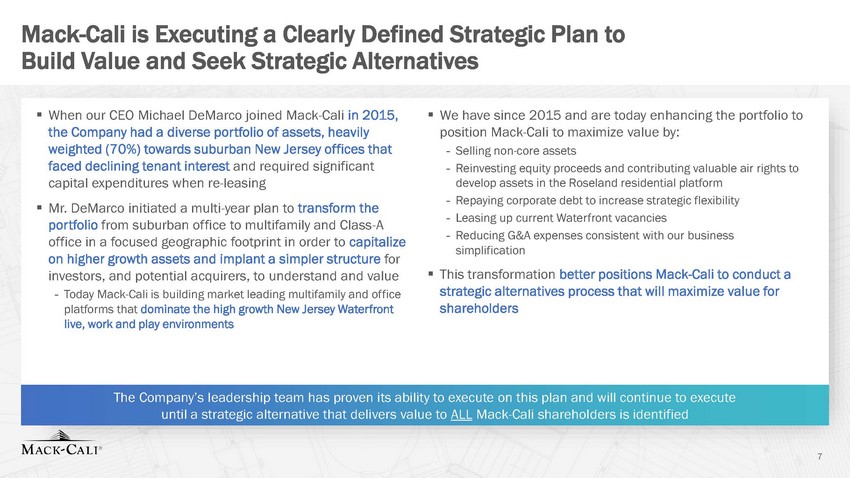

Mack-Cali is Executing a Clearly Defined Strategic Plan to Build Value and Seek Strategic Alternatives - Leasing up current Waterfront vacancies portfolio from suburban office to multifamily and Class-A simplification until a strategic alternative that delivers value to ALL Mack-Cali shareholders is identified 7 ▪ When our CEO Michael DeMarco joined Mack-Cali in 2015,▪ We have since 2015 and are today enhancing the portfolio to the Company had a diverse portfolio of assets, heavilyposition Mack-Cali to maximize value by: weighted (70%) towards suburban New Jersey offices that-Selling non-core assets faced declining tenant interest and required significant-Reinvesting equity proceeds and contributing valuable air rights to capital expenditures when re-leasingdevelop assets in the Roseland residential platform ▪ Mr. DeMarco initiated a multi-year plan to transform the-Repaying corporate debt to increase strategic flexibility office in a focused geographic footprint in order to capitalize-Reducing G&A expenses consistent with our business on higher growth assets and implant a simpler structure for investors, and potential acquirers, to understand and value▪ This transformation better positions Mack-Cali to conduct a - Today Mack-Cali is building market leading multifamily and officestrategic alternatives process that will maximize value for platforms that dominate the high growth New Jersey Waterfrontshareholders live, work and play environments The Company’s leadership team has proven its ability to execute on this plan and will continue to execute |

|

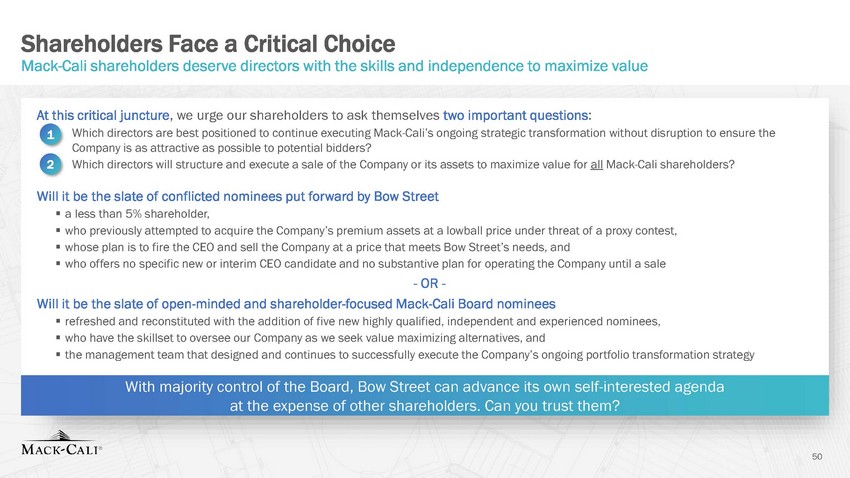

Vote For a Slate of Highly Qualified Directors Well-Positioned to Deliver Shareholder Value Mack-Cali’s full slate of directors is equipped to oversee strategic transactions CEO Experience and historical CEO, Mack-Cali, Delivering our REIT CFO experienced with Portfolio Manager for Real Estate Director since 2018 Visionary perspective on Extensive public company board Real estate development Director since 2016 experience | Director since 1994 8 Incumbent Directors Have Necessary Skills andNew Independent Nominees All Have Significant Prior Board Perspectives to Pursue Strategic AlternativesExperience and Expertise to Oversee A Strategic Process Alan BernikowMichael DeMarcoJamie BeharMichael Berman insights | Director since 2004strategy to build valueand Alternative Investmentsstrategic alternatives Lisa MyersLaura PomerantzHoward RothGail Steinel Investor view from both privateCommercial real estate expertReal estate transactionalLeadership skills built in equity and active fund seatsand seasoned public companyexpertise honed as an externalstrategy and operations Director since 2019director | Director since 2019accounting advisorconsulting Irvin ReidRebecca RobertsonLee Wielansky and economic developmentredevelopment opportunitiescompany CEO If the Company’s nominees are elected at the Annual Meeting: 8 of 11 directors5 of 11 directors4 of 11 directors will have joined since 2018will be experienced institutional investorswill have CEO or CFO experience, with Board will have average tenure of 4.6 yearswho bring a shareholder perspective3 at real estate companies ANTICIPATED BOARD REFRESHMENT Two directors expected to retire at 2021 AGM |

|

Agenda Mack-Cali’s Board has Listened and Been Responsive to Shareholders 1 Strategy, Execution & Performance Driving Growth and Portfolio Transformation 2 Bow Street is Seeking Control of Your Company to Pursue its Own Agenda 3 Shareholders Deserve Directors Maximize Value Best Positioned to 4 5 Appendix 9 |

|

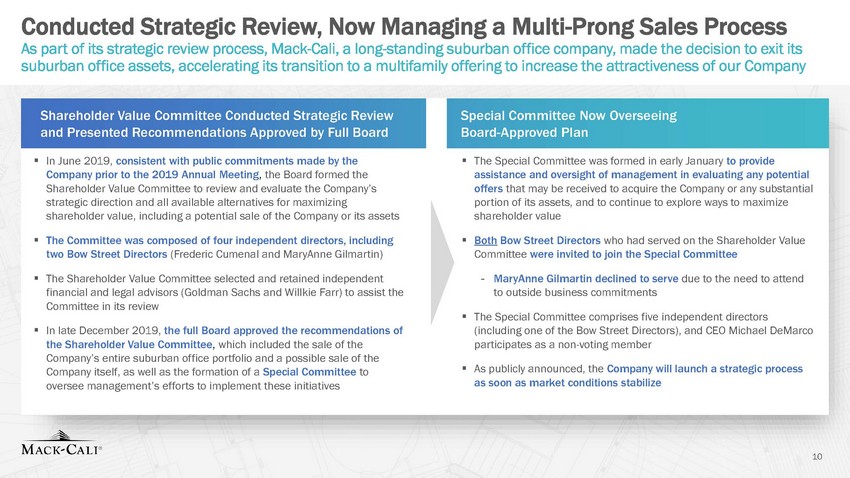

Conducted Strategic Review, Now Managing a Multi-Prong Sales Process As part of its strategic review process, Mack-Cali, a long-standing suburban office company, made the decision to exit its suburban office assets, accelerating its transition to a multifamily offering to increase the attractiveness of our Company ▪ The Special Committee comprises five independent directors ▪ As publicly announced, the Company will launch a strategic process Company itself, as well as the formation of a Special Committee to 10 Shareholder Value Committee Conducted Strategic ReviewSpecial Committee Now Overseeing and Presented Recommendations Approved by Full BoardBoard-Approved Plan ▪ In June 2019, consistent with public commitments made by the▪ The Special Committee was formed in early January to provide Company prior to the 2019 Annual Meeting, the Board formed theassistance and oversight of management in evaluating any potential Shareholder Value Committee to review and evaluate the Company’soffers that may be received to acquire the Company or any substantial strategic direction and all available alternatives for maximizingportion of its assets, and to continue to explore ways to maximize shareholder value, including a potential sale of the Company or its assetsshareholder value ▪ The Committee was composed of four independent directors, including▪ Both Bow Street Directors who had served on the Shareholder Value two Bow Street Directors (Frederic Cumenal and MaryAnne Gilmartin)Committee were invited to join the Special Committee ▪ The Shareholder Value Committee selected and retained independent-MaryAnne Gilmartin declined to serve due to the need to attend financial and legal advisors (Goldman Sachs and Willkie Farr) to assist theto outside business commitments Committee in its review ▪ In late December 2019, the full Board approved the recommendations of(including one of the Bow Street Directors), and CEO Michael DeMarco the Shareholder Value Committee, which included the sale of theparticipates as a non-voting member Company’s entire suburban office portfolio and a possible sale of the oversee management’s efforts to implement these initiativesas soon as market conditions stabilize |

|

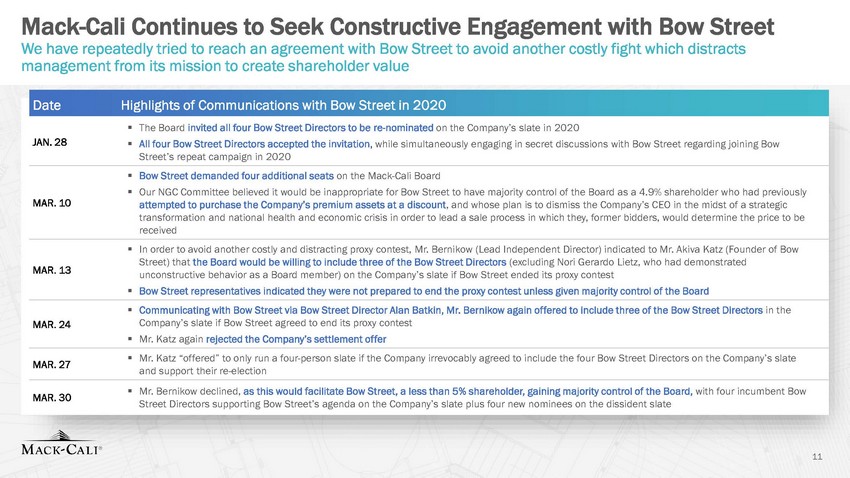

Mack-Cali Continues to Seek Constructive Engagement with Bow Street We have repeatedly tried to reach an agreement with Bow Street to avoid another costly fight which distracts management from its mission to create shareholder value MAR. 13 unconstructive behavior as a Board member) on the Company’s slate if Bow Street ended its proxy contest and support their re-election Street Directors supporting Bow Street’s agenda on the Company’s slate plus four new nominees on the dissident slate 11 DateHighlights of Communications with Bow Street in 2020 ▪ The Board invited all four Bow Street Directors to be re-nominated on the Company’s slate in 2020 JAN. 28▪ All four Bow Street Directors accepted the invitation, while simultaneously engaging in secret discussions with Bow Street regarding joining Bow Street’s repeat campaign in 2020 ▪ Bow Street demanded four additional seats on the Mack-Cali Board ▪ Our NGC Committee believed it would be inappropriate for Bow Street to have majority control of the Board as a 4.9% shareholder who had previously MAR. 10attempted to purchase the Company’s premium assets at a discount, and whose plan is to dismiss the Company’s CEO in the midst of a strategic transformation and national health and economic crisis in order to lead a sale process in which they, former bidders, would determine the price to be received ▪ In order to avoid another costly and distracting proxy contest, Mr. Bernikow (Lead Independent Director) indicated to Mr. Akiva Katz (Founder of Bow Street) that the Board would be willing to include three of the Bow Street Directors (excluding Nori Gerardo Lietz, who had demonstrated ▪ Bow Street representatives indicated they were not prepared to end the proxy contest unless given majority control of the Board ▪ Communicating with Bow Street via Bow Street Director Alan Batkin, Mr. Bernikow again offered to include three of the Bow Street Directors in the MAR. 24Company’s slate if Bow Street agreed to end its proxy contest ▪ Mr. Katz again rejected the Company’s settlement offer MAR. 27▪ Mr. Katz “offered” to only run a four-person slate if the Company irrevocably agreed to include the four Bow Street Directors on the Company’s slate MAR. 30▪ Mr. Bernikow declined, as this would facilitate Bow Street, a less than 5% shareholder, gaining majority control of the Board, with four incumbent Bow |

|

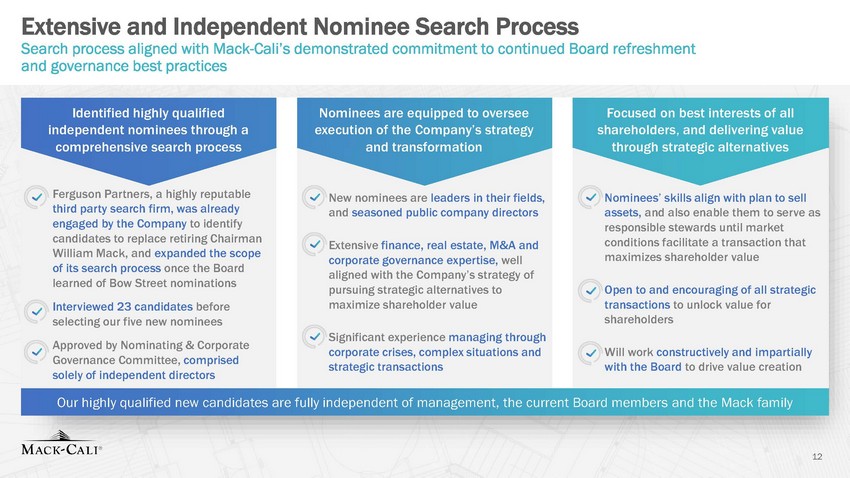

Extensive and Independent Nominee Search Process Search process aligned with Mack-Cali’s demonstrated commitment to continued Board refreshment and governance best practices third party search firm, was already candidates to replace retiring Chairman of its search process once the Board Governance Committee, comprised 12 Identified highly qualified Nominees are equipped to overseeFocused on best interests of all independent nominees through aexecution of the Company’s strategyshareholders, and delivering value through strategic alternatives Nominees’ skills align with plan to sell assets, and also enable them to serve as responsible stewards until market conditions facilitate a transaction that maximizes shareholder value Open to and encouraging of all strategic transactions to unlock value for shareholders Will work constructively and impartially with the Board to drive value creation comprehensive search process Ferguson Partners, a highly reputable engaged by the Company to identify William Mack, and expanded the scope learned of Bow Street nominations Interviewed 23 candidates before selecting our five new nominees Approved by Nominating & Corporate solely of independent directors Our highly qualified new candidates are fully independent of management, the current Board members and the Mack family and transformation New nominees are leaders in their fields, and seasoned public company directors Extensive finance, real estate, M&A and corporate governance expertise, well aligned with the Company’s strategy of pursuing strategic alternatives to maximize shareholder value Significant experience managing through corporate crises, complex situations and strategic transactions |

|

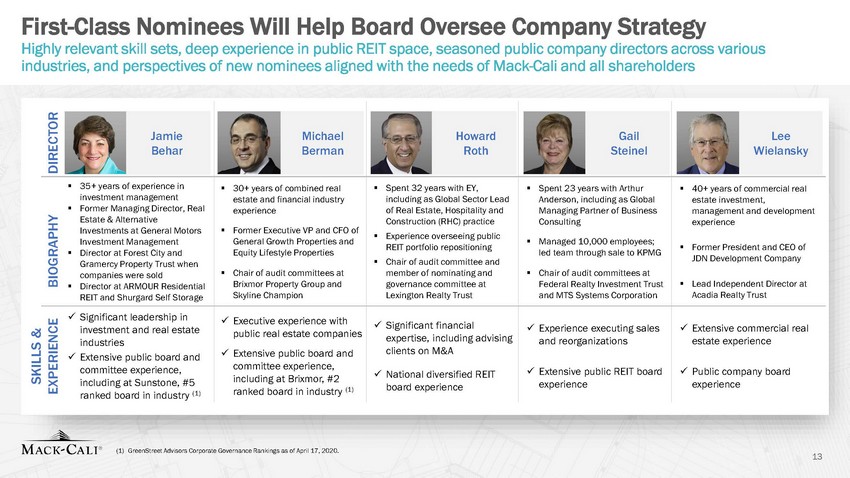

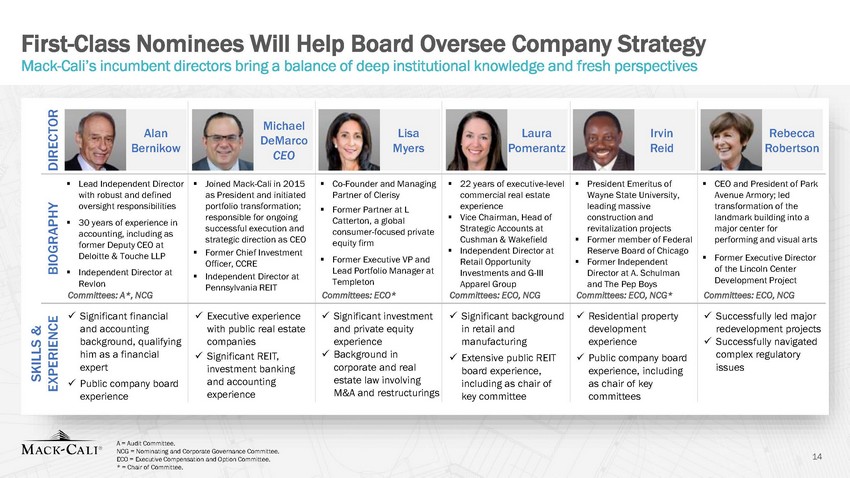

First-Class Nominees Will Help Board Oversee Company Strategy Highly relevant skill sets, deep experience in public REIT space, seasoned public company directors across various industries, and perspectives of new nominees aligned with the needs of Mack-Cali and all shareholders ▪ Experience overseeing public (1) GreenStreet Advisors Corporate Governance Rankings as of April 17, 2020. 13 SKILLS & EXPERIENCE BIOGRAPHY DIRECTOR estate investment, experience Acadia Realty Trust estate experience experience Jamie Behar Michael Berman Howard Roth Gail Steinel Lee Wielansky ▪ 35+ years of experience in investment management ▪ Former Managing Director, Real Estate & Alternative Investments at General Motors Investment Management ▪ Director at Forest City and Gramercy Property Trust when companies were sold ▪ Director at ARMOUR Residential REIT and Shurgard Self Storage ▪ 30+ years of combined real estate and financial industry experience ▪ Former Executive VP and CFO of General Growth Properties and Equity Lifestyle Properties ▪ Chair of audit committees at Brixmor Property Group and Skyline Champion ▪ Spent 32 years with EY, including as Global Sector Lead of Real Estate, Hospitality and Construction (RHC) practice REIT portfolio repositioning ▪ Chair of audit committee and member of nominating and governance committee at Lexington Realty Trust ▪ Spent 23 years with Arthur Anderson, including as Global Managing Partner of Business Consulting ▪ Managed 10,000 employees; led team through sale to KPMG ▪ Chair of audit committees at Federal Realty Investment Trust and MTS Systems Corporation ▪ 40+ years of commercial real management and development ▪ Former President and CEO of JDN Development Company ▪ Lead Independent Director at x Significant leadership in investment and real estate industries x Extensive public board and committee experience, including at Sunstone, #5 ranked board in industry (1) x Executive experience with public real estate companies x Extensive public board and committee experience, including at Brixmor, #2 ranked board in industry (1) x Significant financial expertise, including advising clients on M&A x National diversified REIT board experience x Experience executing sales and reorganizations x Extensive public REIT board experience x Extensive commercial real x Public company board |

|

First-Class Nominees Will Help Board Oversee Company Strategy Mack-Cali’s incumbent directors bring a balance of deep institutional knowledge and fresh perspectives as chair of key A = Audit Committee. NCG = Nominating and Corporate Governance Committee. ECO = Executive Compensation and Option Committee. * = Chair of Committee. 14 SKILLS & EXPERIENCE BIOGRAPHY landmark building into a performing and visual arts of the Lincoln Center Committees: ECO, NCG issues DIRECTOR Alan Bernikow Lisa Myers ▪ Lead Independent Director with robust and defined oversight responsibilities ▪ 30 years of experience in accounting, including as former Deputy CEO at Deloitte & Touche LLP ▪ Independent Director at Revlon Committees: A*, NCG ▪ Joined Mack-Cali in 2015 as President and initiated portfolio transformation; responsible for ongoing successful execution and strategic direction as CEO ▪ Former Chief Investment Officer, CCRE ▪ Independent Director at Pennsylvania REIT ▪ Co-Founder and Managing Partner of Clerisy ▪ Former Partner at L Catterton, a global consumer-focused private equity firm ▪ Former Executive VP and Lead Portfolio Manager at Templeton Committees: ECO* ▪ 22 years of executive-level commercial real estate experience ▪ Vice Chairman, Head of Strategic Accounts at Cushman & Wakefield ▪ Independent Director at Retail Opportunity Investments and G-III Apparel Group Committees: ECO, NCG ▪ President Emeritus of Wayne State University, leading massive construction and revitalization projects ▪ Former member of Federal Reserve Board of Chicago ▪ Former Independent Director at A. Schulman and The Pep Boys Committees: ECO, NCG* ▪ CEO and President of Park Avenue Armory; led transformation of the major center for ▪ Former Executive Director Development Project x Significant financial and accounting background, qualifying him as a financial expert x Public company board experience x Executive experience with public real estate companies x Significant REIT, investment banking and accounting experience x Significant investment and private equity experience x Background in corporate and real estate law involving M&A and restructurings x Significant background in retail and manufacturing x Extensive public REIT board experience, including as chair of key committee x Residential property development experience x Public company board experience, including committees x Successfully led major redevelopment projects x Successfully navigated complex regulatory Rebecca Robertson Michael DeMarco CEO Laura Pomerantz Irvin Reid |

|

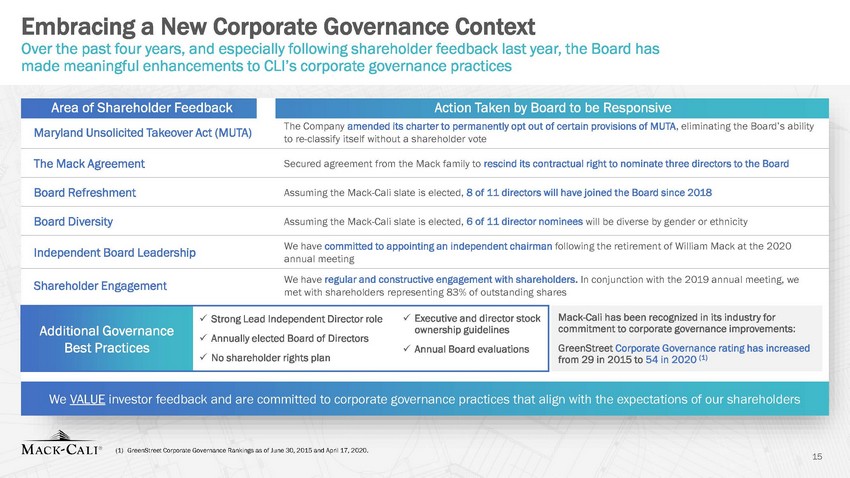

Embracing a New Corporate Governance Context Over the past four years, and especially following shareholder feedback last year, the Board has made meaningful enhancements to CLI’s corporate governance practices to re-classify itself without a shareholder vote annual meeting met with shareholders representing 83% of outstanding shares commitment to corporate governance improvements: from 29 in 2015 to 54 in 2020 (1) (1) GreenStreet Corporate Governance Rankings as of June 30, 2015 and April 17, 2020. 15 Area of Shareholder FeedbackAction Taken by Board to be Responsive Maryland Unsolicited Takeover Act (MUTA)The Company amended its charter to permanently opt out of certain provisions of MUTA, eliminating the Board’s ability The Mack AgreementSecured agreement from the Mack family to rescind its contractual right to nominate three directors to the Board Board RefreshmentAssuming the Mack-Cali slate is elected, 8 of 11 directors will have joined the Board since 2018 Board DiversityAssuming the Mack-Cali slate is elected, 6 of 11 director nominees will be diverse by gender or ethnicity Independent Board LeadershipWe have committed to appointing an independent chairman following the retirement of William Mack at the 2020 Shareholder EngagementWe have regular and constructive engagement with shareholders. In conjunction with the 2019 annual meeting, we x Strong Lead Independent Director rolex Executive and director stock Additional Governancex Annually elected Board of Directorsownership guidelines Best Practicesx Annual Board evaluations x No shareholder rights plan Mack-Cali has been recognized in its industry for GreenStreet Corporate Governance rating has increased We VALUE investor feedback and are committed to corporate governance practices that align with the expectations of our shareholders |

|

Agenda Mack-Cali’s Board has Listened and Been Responsive to Shareholders 1 Strategy, Execution and Performance Driving Growth and Portfolio Transformation 2 Bow Street is Seeking Control of Your Company to Pursue its Own Agenda 3 Shareholders Deserve Maximize Value Directors Best Positioned to 4 5 Appendix 16 |

|

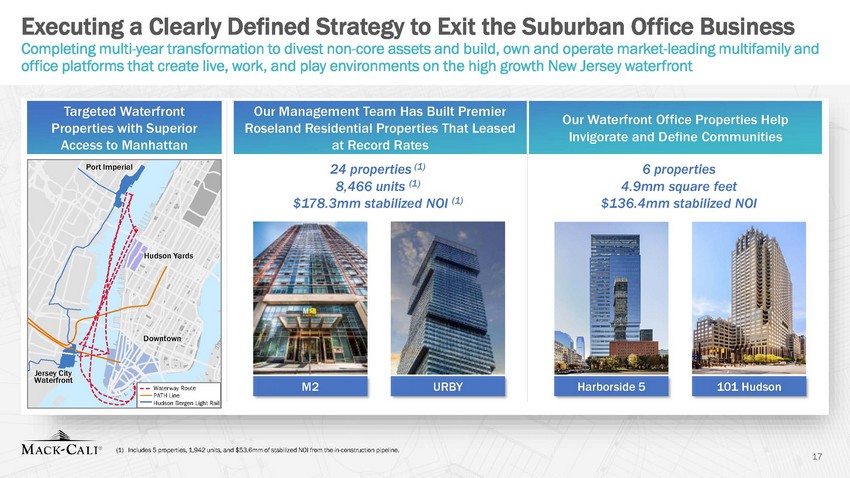

Executing a Clearly Defined Strategy to Exit the Suburban Office Business Completing multi-year transformation to divest non-core assets and build, own and operate market-leading multifamily and office platforms that create live, work, and play environments on the high growth New Jersey waterfront Properties with Superior Roseland Residential Properties That Leased Invigorate and Define Communities M2 URBY Harborside 5 101 Hudson (1) Includes 5 properties, 1,942 units, and $53.6mm of stabilized NOI from the in-construction pipeline. 17 Targeted WaterfrontOur Management Team Has Built PremierOur Waterfront Office Properties Help Access to Manhattanat Record Rates 24 properties (1) 6 properties 8,466 units (1) 4.9mm square feet $178.3mm stabilized NOI (1) $136.4mm stabilized NOI Waterfront NY008YXZ: 1301728_01.WOR Port Imperial Hudson Yards Downtown Jersey City Waterway Route PATH Line Hudson Bergen Light Rail |

|

Key Facets to Achieve the Goals of Mack-Cali’s Strategy When hired in 2015, Michael DeMarco devised a simplification strategy with the goal of fewer and larger multifamily and Class A office assets Creating Platform Value Selling the remaining suburban office portfolio Repaying corporate debt to increase strategic flexibility Developing core residential platform with control and scale Progressing non-core asset recycling efforts Leasing-up waterfront vacancy suburban office sales to indebtedness and complete borrowing strategy The execution of our strategy required significant time and expertise to orchestrate and we have successfully led the platform to the final phase and transformed Mack-Cali into the largest NJ Waterfront landlord (1) Rockpoint Group LLC’s investment includes the $300mm investment as per the Original Investment Agreement as of March 31, 2019. On June 28, 2019, Rockpoint Group LLC invested $100mm as per the Add On Investment Agreement. As of December 31, 2019, Rockpoint Group LLC’s investment totaled $400mm. 18 Deploy proceeds from repay remaining corporate the transition to a secured Lease the remaining 1.0MSF of waterfront vacancy (current vacancies and 2020 lease expirations) Disposed of $2.5bn of non-core assets, including 99 Flex buildings and 87 Suburban Office buildings in weaker markets In the process of selling the remaining 36 suburban office assets, with 17 currently under contract Created the Roseland Residential Trust joint-venture with Rockpoint Group LLC which has raised $400mm of growth equity at NAV to date (1) Asset Recycling: 90% of Regional Portfolio |

|

Mack-Cali has the Right Management Team in Place to Achieve its Goals The Board, including Bow Street’s nominees, unanimously endorsed Management’s current execution strategy Chief Executive Officer implementing a local market strategy with the scale of a public REIT ▪ ▪ CEO of Mack-Cali since April 2017 and Since 2015, Mr. DeMarco has led the Company’s current portfolio transformation Executive VP & Chief Administrative Officer marketing, human resources and Executive VP & Chief Investment Officer acquisitions and identifying opportunities repositioning or disposition ▪ Co-Founder and Chairman of Roseland ▪ President of Roseland Residential Trust Mack-Cali in October 2012 ▪ Responsible for Mack-Cali's leasing Company's in-house leasing team Chief Financial Officer ▪ CFO of Mack-Cali since 2018 and is financial planning analyst at Morgan Stanley for the Global Gary Wagner ▪ Responsible for corporate governance, overseeing risk management Company until its acquisition by Mack-Cali 19 Michael DeMarcoThe Mack-Cali team is expertlyDeidre Crockett previously held the role of President and COO▪ Responsible for public relations, development and execution of theinvestor relations Ricardo Cardoso Marshall B. Tycher▪ Responsible for sourcing new real estate Chairman, Roseland Residential Trustwithin the Company’s portfolio for asset Residential Trust from 1992 until Roseland’s acquisition byNicholas A. Hilton Executive VP, Leasing efforts and management of the David J. Smetana responsible for Mack-Cali's strategicGeneral Counsel & Secretary ▪ Former managing director and securitiessupervising outside legal counsel and Real Estate Securities business▪ Previously held roles at the Robert Martin 1Extensive Local Government Relations Support Value-Add Entitlements 2Finger on the Pulse of NJ Waterfront Market Leasing Demand 3Development Expertise on a Local Level Leading Landlord Supported by Strong 4Relationships with Leasing and Sales Brokers Actively Managing Corporate Costs (283 5current employees vs. 600 in 2015) |

|

The Street Supports Management and its Strategy Analysts recognize DeMarco’s strategic transformation creates long term value “We continue to like the shares of CLI, and view any pullback after earnings waterfront and JC residential mix. This should leave CLI more focused and incentives bill as an opportunity to buy the stock. We think management’s suburban dispositions can be made in a financially beneficial manner to their track record we have confidence in their ability to follow through on the double the size of its residential units over time.” Source: Wall Street research as of April 21, 2020. Permission to use quotations neither sought nor obtained. 20 “Despite no deal materializing, Mr. DeMarco has repeatedly stated his“Given how long we are in the current economic cycle, selling low quality willingness to pursue an entity-level transaction…should the company’s currentassets and paying down debt de-risks the company…There could be upside strategic direction ultimately fail to remedy the persistent discount to NAV atshould CLI make significant progress in leasing up its core Waterfront office which shares trade. Shareholders have seemingly been sympathetic as Mr. portfolio. A key upside risk to our thesis is the possibility of a transaction.” DeMarco received strong support during last year’s director election. As such, it would be both surprising and unwarranted in our view to see shareholders now support the removal of Mr. DeMarco as CEO.” February 25, 2020 March 12, 2020 “CLI has moved from a predominantly diversified suburban focused REIT, with high cap rate suburban office assets, to a lower cap [rate] profile core Jersey City in response to light NJ Waterfront leasing volume and uncertainty regarding thecleaner with an improved balance sheet…We see further upside if future strategy is the right approach to create a more desirable portfolio, and givenshareholders and CLI continues to tap its residential land bank that could nearly transactional components of the portfolio transformation.” February 2, 2020 February 16, 2020 |

|

Dominant Jersey City Waterfront Market Share Mack-Cali has developed the Jersey City waterfront to create an attractive and vibrant live / work / play community M2 311 Units Urby 1 Soho Lofts 377 Units Liberty Towers The Charlotte 107 Morgan Monaco Plaza Plaza 4a Plaza 1, 2, 3 412 Units Residential Units 2016 - 2019 Residential Future Residential Commercial 21 648 Units750 Units101 Hudson St.804 Units5762 Units523 Units(Remote)L I V E Whole FoodsMarbella URBY Lobby W O R K Total OperatingFood Hall at Jersey City Waterfront 2015 Residential P L AY The Lutze Biergarten Harborside 9 900 Units 935 Total + 2,098 Units | 3,033 Total The Lutze + 4,634 Units | 7,667 Total Hudson River 4.3 MSF Harborside 4 750 Units Harborside 8 680 Units Urby 2 750 Units |

|

Well-Located Port Imperial Residential Ecosystem Highly amenitized residential developments offer compelling value and convenient access to Hudson Yards 55 Riverwalk Place Riverbend 1 RiverHouse 11 +9MSF Net Office Leasing ~45k New Jobs (1) 2006 2000 2018 The Capstone Residence Inn Riverbend 2 And 3 At Port Imperial 2020 Delivery At Port Imperial 164 Keys 2002 316 Units 280 Units At Port Imperial 2003/2004 At Port Imperial Envue Autograph Garage 236 Units 208 Keys RiverHouse 9 South Ferry 250 Units Legend 3,035 Total (3) | + 1,34020U1n9its Future (1) Assumes density of 200SF per office job. (2) Represents 832 owned operating units and 863 managed operating units. (3) Represents 1,656 owned operating units and 1,379 managed operating units. (4) Represents 3,308 owned operating units and 1,379 managed operating units. 22 $25bn investment by Related / Oxford At Port ImperialAt Port ImperialAt Port Imperial 295 Units302 Units348 Units RiverTrace RiverParcPort ImperialAt Port ImperialAt Port Imperial2013 2014RiverHouse 9213 Units360 Units 2020 DeliveryThe ClubhouseHudson Yards RiversEdge313 UnitsAt Port Imperial 2009Hotel North Garage Park Parcel Future Development 302 Units Parcel 2 Future Development Hudson River EnVue Autograph Collection Hotel Terminal Parcel 6+1 Future Development 600 Units Total Owned & Managed Operating Residential Units Parcel 16Parcel 3 Future DevelopmentFuture Development 200 Units300 Units ~ 8 min. Ferry to Hudson Yards 2015 1,695 Total (2) 2016 - 20192015 Future 4,687 Total (4) | + 1,652 Units The Capstone |

|

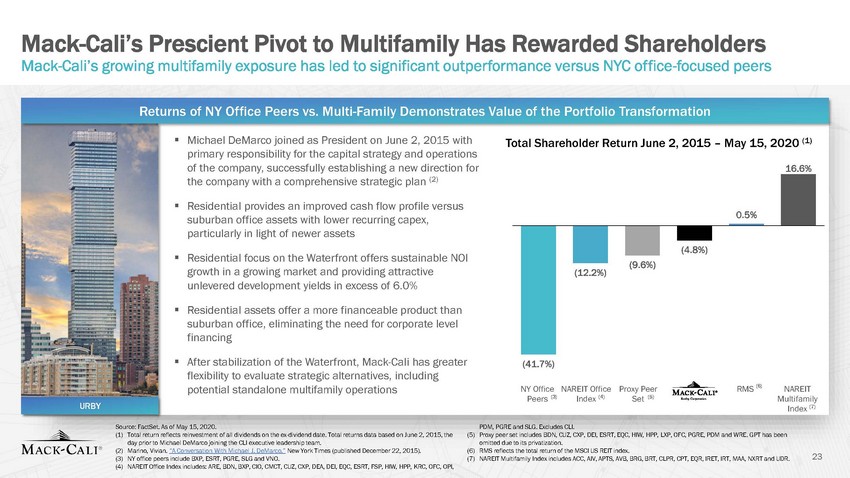

Mack-Cali’s Prescient Pivot to Multifamily Has Rewarded Shareholders Mack-Cali’s growing multifamily exposure has led to significant outperformance versus NYC office-focused peers primary responsibility for the capital strategy and operations suburban office assets with lower recurring capex, Peers (3) Index (4) Set (5) Multifamily Source: FactSet. As of May 15, 2020. (1) Total return reflects reinvestment of all dividends on the ex-dividend date. Total returns data based on June 2, 2015, the day prior to Michael DeMarco joining the CLI executive leadership team. (2) Marino, Vivian. “A Conversation With Michael J. DeMarco.” New York Times (published December 22, 2015). PDM, PGRE and SLG. Excludes CLI. (5) Proxy peer set includes BDN, CUZ, CXP, DEI, ESRT, EQC, HIW, HPP, LXP, OFC, PGRE, PDM and WRE. GPT has been omitted due to its privatization. (6) RMS reflects the total return of the MSCI US REIT index. (7) NAREIT Multifamily Index includes ACC, AIV, APTS, AVB, BRG, BRT, CLPR, CPT, EQR, IRET, IRT, MAA, NXRT and UDR. 23 (3) NY office peers include BXP, ESRT, PGRE, SLG and VNO. (4) NAREIT Office Index includes: ARE, BDN, BXP, CIO, CMCT, CUZ, CXP, DEA, DEI, EQC, ESRT, FSP, HIW, HPP, KRC, OFC, OPI, Returns of NY Office Peers vs. Multi-Family Demonstrates Value of the Portfolio Transformation ▪ Michael DeMarco joined as President on June 2, 2015 withTotal Shareholder Return June 2, 2015 – May 15, 2020 (1) of the company, successfully establishing a new direction for16.6% the company with a comprehensive strategic plan (2) ▪ Residential provides an improved cash flow profile versus particularly in light of newer assets ▪ Residential focus on the Waterfront offers sustainable NOI growth in a growing market and providing attractive unlevered development yields in excess of 6.0% ▪ Residential assets offer a more financeable product than suburban office, eliminating the need for corporate level financing ▪ After stabilization of the Waterfront, Mack-Cali has greater(41.7%) flexibility to evaluate strategic alternatives, including potential standalone multifamily operationsNY Office NAREIT Office Proxy PeerMack-Cali RMS (6)NAREIT URBYIndex (7) 0.5% (4.8%) (9.6%) (12.2%) |

|

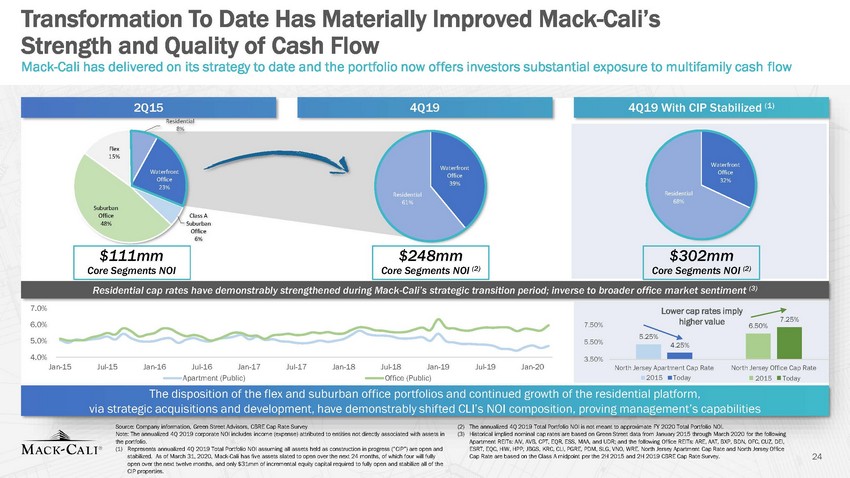

Transformation To Date Has Materially Improved Mack-Cali’s Strength and Quality of Cash Flow Mack-Cali has delivered on its strategy to date and the portfolio now offers investors substantial exposure to multifamily cash flow Office Suburban 6.50% 4.25% Source: Company information, Green Street Advisors, CBRE Cap Rate Survey Note: The annualized 4Q 2019 corporate NOI includes income (expense) attributed to entities not directly associated with assets in the portfolio. (1) Represents annualized 4Q 2019 Total Portfolio NOI assuming all assets held as construction in progress (“CIP”) are open and stabilized. As of March 31, 2020, Mack-Cali has five assets slated to open over the next 24 months, of which four will fully open over the next twelve months, and only $31mm of incremental equity capital required to fully open and stabilize all of the CIP properties. (2) (3) The annualized 4Q 2019 Total Portfolio NOI is not meant to approximate FY 2020 Total Portfolio NOI. Historical implied nominal cap rates are based on Green Street data from January 2015 through March 2020 for the following Apartment REITs: AIV, AVB, CPT, EQR, ESS, MAA, and UDR; and the following Office REITs: ARE, AAT, BXP, BDN, OFC, CUZ, DEI, ESRT, EQC, HIW, HPP, JBGS, KRC, CLI, PGRE, PDM, SLG, VNO, WRE. North Jersey Apartment Cap Rate and North Jersey Office Cap Rate are based on the Class A midpoint per the 2H 2015 and 2H 2019 CBRE Cap Rate Survey. 24 2Q154Q194Q19 With CIP Stabilized (1) Residential 8% Flex 15% Waterfro t Office 39% 61% Office Class A 48% Suburban Office 6% Waterfront 32% Residential 68% $111mm Core Segments NOI $248mm Core Segments NOI (2) $302mm Core Segments NOI (2) Residential cap rates have demonstrably strengthened during Mack-Cali’s strategic transition period; inverse to broader office market sentiment (3) 7.0% 6.0% 5.0% 4.0% Jan-15Jul-15Jan-16Jul-16Jan-17Jul-17Jan-18Jul-18Jan-19Jul-19Jan-20 Apartment (Public)Office (Public) 7.50% 5.50% 3.50% Lower cap rates imply higher value7.25% 5.25% North Jersey Apartment Cap RateNorth Jersey Office Cap Rate 2015Today2015Today The disposition of the flex and suburban office portfolios and continued growth of the residential platform, via strategic acquisitions and development, have demonstrably shifted CLI’s NOI composition, proving management’s capabilities Waterfr nt Offic 23% Residential |

|

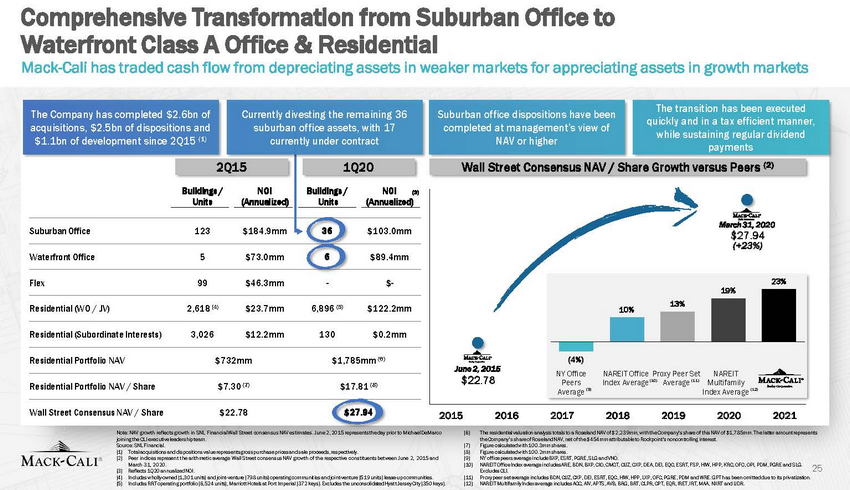

Comprehensive Transformation from Suburban Office to Waterfront Class A Office & Residential Mack-Cali has traded cash flow from depreciating assets in weaker markets for appreciating assets in growth marketsThe Company has completed $2.6bn of acquisitions, $2.5bn of dispositions and $1.1bn of development since 2Q15 (1)Currently divesting the remaining 36 suburban office assets, with 17 currently under contractSuburban office dispositions have been completed at management’s view of NAV or higherThe transition has been executed quickly and in a tax efficient manner, while sustaining regular dividend payments2Q15 1Q20Wall Street Consensus NAV / Share Growth versus Peers (2)Buildings /NOIBuildings /NOI(3)Units(Annualized)Units(Annualized)Suburban Office 123 $184.9mm 36 $103.0mmWaterfront Office 5 $73.0mm 6 $89.4mmMarch 31, 2020 $27.94 (+23%)Flex 99 $46.3mm - $- Residential (WO / JV) 2,618 (4) $23.7mm 6,896 (5) $122.2mm Residential (Subordinate Interests) 3,026 $12.2mm 130 $0.2mm13% 10%19%23%Residential Portfolio NAV $732mm $1,785mm (6)June 2, 2015(4%)NY OfficeNAREIT Office Proxy Peer SetNAREITCLIResidential Portfolio NAV / Share $7.30 (7) $17.81 (8)$22.78Peers Average (9)Index Average(10)Average (11)Multifamily Index Average (12)Wall Street Consensus NAV / Share $22.78 $27.942015 2016 2017 2018 20192020 2021Note: NAV growth reflects growth in SNL Financial Wall Street consensus NAV estimates. June 2, 2015 represents the day prior to Michael DeMarco joining the CLI executive leadership team. Source: SNL Financial. (1) Total acquisitions and dispositions value represents gross purchase prices and sale proceeds, respectively. (2) Peer indices represent the arithmetic average Wall Street consensus NAV growth of the respective constituents between June 2, 2015 and March 31, 2020. (3) Reflects 1Q20 annualized NOI. (4) Includes wholly-owned (1,301 units) and joint-venture (798 units) operating communities and joint-venture (519 units) lease-up communities. (5) Includes RRT operating portfolio (6,524 units), Marriott Hotels at Port Imperial (372 keys). Excludes the unconsolidated Hyat t Jersey City (350 keys).(6) The residential valuation analysis totals to a Roseland NAV of $2,239mm, with the Company’s share of this NAV of $1,785mm. Th e latter amount represents the Company’s share of Roseland NAV, net of the $454mm attributable to Rockpoint's noncontrolling interest. (7) Figure calculated with 100.3mm shares. (8) Figure calculated with 100.2mm shares. (9) NY office peers average include BXP, ESRT, PGRE, SLG and VNO. (10) NAREIT Office Index average includes ARE, BDN, BXP, CIO, CMCT, CUZ, CXP, DEA, DEI, EQC, ESRT, FSP, HIW, HPP, KRC, OFC, OPI, PDM, PGRE and SLG. Excludes CLI. (11) Proxy peer set average includes BDN, CUZ, CXP, DEI, ESRT, EQC, HIW, HPP, LXP, OFC, PGRE, PDM and WRE. GPT has been omitted due to its privatization. (12) NAREIT Multifamily Index average includes ACC, AIV, APTS, AVB, BRG, BRT, CLPR, CPT, EQR, IRET, IRT, MAA, NXRT and UDR. |

|

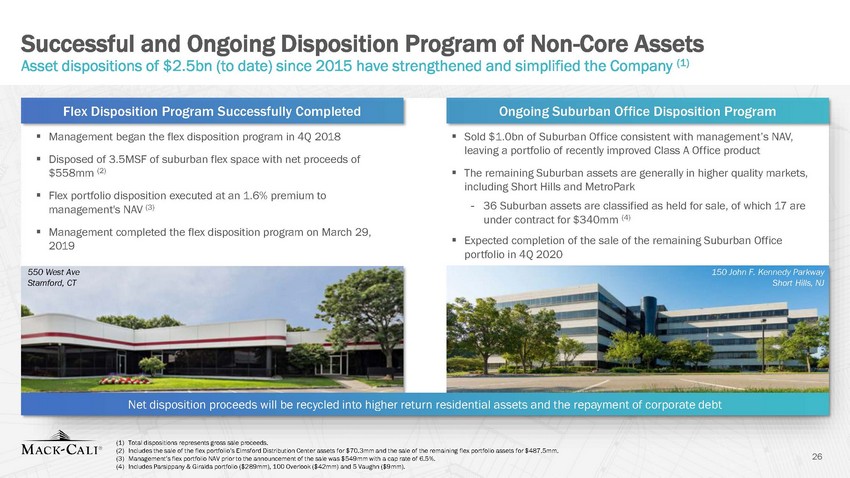

Successful and Ongoing Disposition Program of Non-Core Assets Asset dispositions of $2.5bn (to date) since 2015 have strengthened and simplified the Company (1) ▪ Disposed of 3.5MSF of suburban flex space with net proceeds of ▪ Flex portfolio disposition executed at an 1.6% premium to under contract for $340mm (4) Expected completion of the sale of the remaining Suburban Office ▪ 2019 (1) Total dispositions represents gross sale proceeds. (2) Includes the sale of the flex portfolio’s Elmsford Distribution Center assets for $70.3mm and the sale of the remaining flex portfolio assets for $487.5mm. (3) Management’s flex portfolio NAV prior to the announcement of the sale was $549mm with a cap rate of 6.5%. (4) Includes Parsippany & Giralda portfolio ($289mm), 100 Overlook ($42mm) and 5 Vaughn ($9mm). 26 Flex Disposition Program Successfully CompletedOngoing Suburban Office Disposition Program ▪ Management began the flex disposition program in 4Q 2018▪ Sold $1.0bn of Suburban Office consistent with management’s NAV, leaving a portfolio of recently improved Class A Office product $558mm (2) ▪ The remaining Suburban assets are generally in higher quality markets, including Short Hills and MetroPark management's NAV (3) -36 Suburban assets are classified as held for sale, of which 17 are ▪ Management completed the flex disposition program on March 29, portfolio in 4Q 2020 550 West Ave150 John F. Kennedy Parkway Stamford, CTShort Hills, NJ Net disposition proceeds will be recycled into higher return residential assets and the repayment of corporate debt |

|

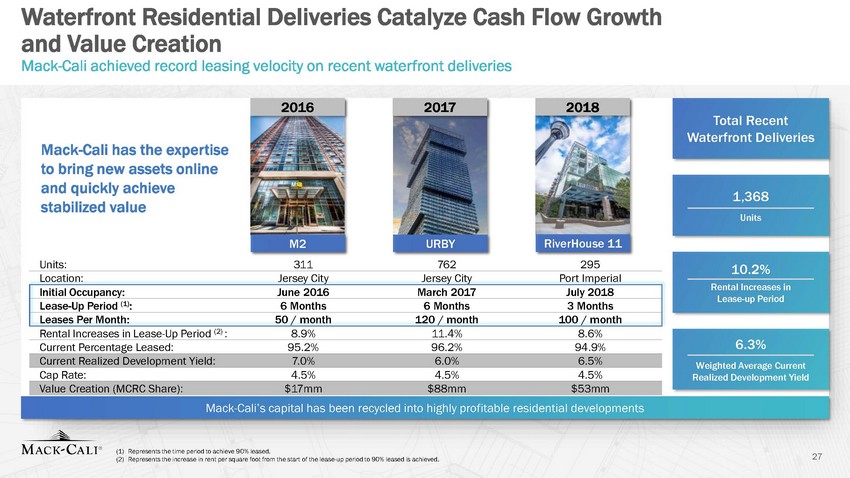

Waterfront Residential Deliveries Catalyze Cash and Value Creation Mack-Cali achieved record leasing velocity on recent waterfront deliveries Flow Growth Total Recent Mack-Cali has the expertise stabilized value Location: Jersey City Jersey City Port Imperial Lease-up Period 6.3% Current Percentage Leased: 95.2% 96.2% 94.9% Cap Rate: 4.5% 4.5% 4.5% Realized Development Yield (1) Represents the time period to achieve 90% leased. (2) Represents the increase in rent per square foot from the start of the lease-up period to 90% leased is achieved. 27 201620172018 Waterfront Deliveries to bring new assets online and quickly achieve1,368 Units M2URBYRiverHouse 11 Units: 311 762 295 10.2% Rental Increases in Rental Increases in Lease-Up Period (2) : 8.9%11.4%8.6% Weighted Average Current Mack-Cali’s capital has been recycled into highly profitable residential developments Value Creation (MCRC Share):$17mm$88mm$53mm Current Realized Development Yield:7.0%6.0%6.5% Initial Occupancy: June 2016 March 2017 July 2018 Lease-Up Period (1): 6 Months6 Months 3 Months Leases Per Month:50 / month120 / month100 / month |

|

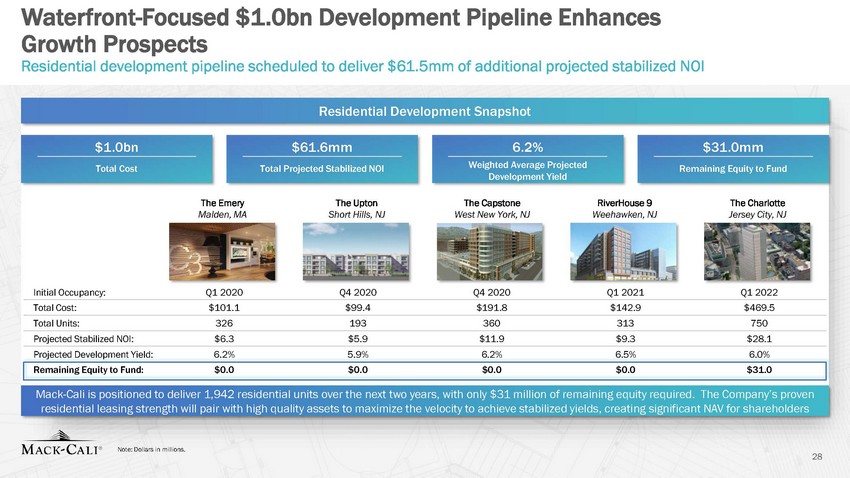

Waterfront-Focused $1.0bn Development Pipeline Enhances Growth Prospects Residential development pipeline scheduled to deliver $61.5mm of additional projected stabilized NOI Development Yield Note: Dollars in millions. 28 Residential Development Snapshot $1.0bn$61.6mm6.2%$31.0mm Total CostTotal Projected Stabilized NOIWeighted Average ProjectedRemaining Equity to Fund The EmeryThe UptonThe CapstoneRiverHouse 9The Charlotte Malden, MAShort Hills, NJWest New York, NJWeehawken, NJJersey City, NJ Initial Occupancy:Q1 2020Q4 2020Q4 2020Q1 2021Q1 2022 Total Cost:$101.1 $99.4$191.8 $142.9 $469.5 Total Units: 326193360313750 Projected Stabilized NOI:$6.3$5.9$11.9$9.3$28.1 Projected Development Yield:6.2%5.9%6.2%6.5%6.0% Remaining Equity to Fund:$0.0$0.0$0.0$0.0$31.0 Mack-Cali is positioned to deliver 1,942 residential units over the next two years, with only $31 million of remaining equity required. The Company’s proven residential leasing strength will pair with high quality assets to maximize the velocity to achieve stabilized yields, creating significant NAV for shareholders |

|

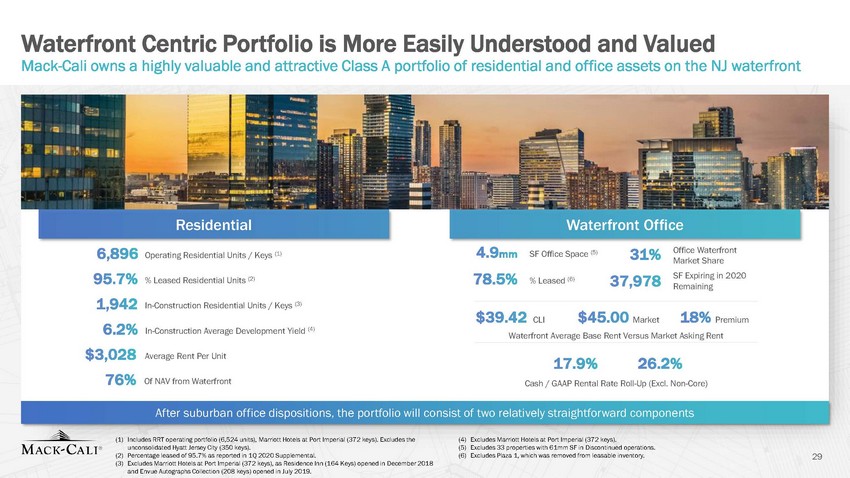

Waterfront Centric Portfolio is More Easily Understood and Valued Mack-Cali owns a highly valuable and attractive Class A portfolio of residential and office assets on the NJ waterfront Market Share Remaining After suburban office dispositions, the portfolio will consist of two relatively straightforward components (1) Includes RRT operating portfolio (6,524 units), Marriott Hotels at Port Imperial (372 keys). Excludes the unconsolidated Hyatt Jersey City (350 keys). (2) Percentage leased of 95.7% as reported in 1Q 2020 Supplemental. (3) Excludes Marriott Hotels at Port Imperial (372 keys), as Residence Inn (164 Keys) opened in December 2018 and Envue Autographs Collection (208 keys) opened in July 2019. (4) Excludes Marriott Hotels at Port Imperial (372 keys). (5) Excludes 33 properties with 61mm SF in Discontinued operations. (6) Excludes Plaza 1, which was removed from leasable inventory. 29 ResidentialWaterfront Office Operating Residential Units / Keys (1) SF Office Space (5) Office Waterfront % Leased Residential Units (2) % Leased (6) SF Expiring in 2020 In-Construction Residential Units / Keys (3) CLIMarketPremium In-Construction Average Development Yield (4) Waterfront Average Base Rent Versus Market Asking Rent Average Rent Per Unit Of NAV from WaterfrontCash / GAAP Rental Rate Roll-Up (Excl. Non-Core) |

|

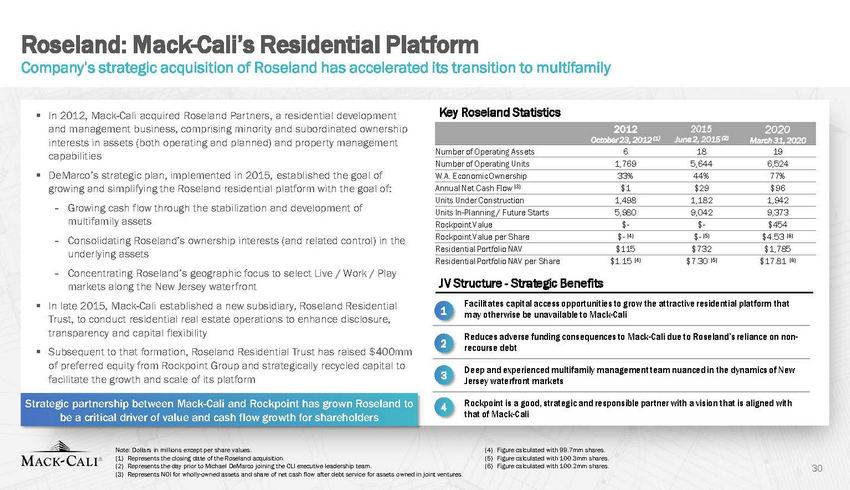

Roseland: Mack-Cali’s Residential Platform Company’s strategic acquisition of Roseland has accelerated its transition to multifamily In 2012, Mack-Cali acquired Roseland Partners, a residential development and management business, comprising minority and subordinated ownership interests in assets (both operating and planned) and property managementKey Roseland Statistics2012 October 23, 2012 (1)2015 June 2, 2015 (2)2020 March 31, 2020capabilities DeMarco’s strategic plan, implemented in 2015, established the goal of growing and simplifying the Roseland residential platform with the goal of:- Growing cash flow through the stabilization and development of multifamily assets- Consolidating Roseland’s ownership interests (and related control) in the underlying assets- Concentrating Roseland’s geographic focus to select Live / Work / Play markets along the New Jersey waterfront In late 2015, Mack-Cali established a new subsidiary, Roseland Residential Trust, to conduct residential real estate operations to enhance disclosure, transparency and capital flexibility Subsequent to that formation, Roseland Residential Trust has raised $400mm of preferred equity from Rockpoint Group and strategically recycled capital to facilitate the growth and scale of its platformStrategic partnership between Mack-Cali and Rockpoint has grown Roseland to be a critical driver of value and cash flow growth for shareholdersNumber of Operating Assets 6 18 19 Number of Operating Units 1,769 5,644 6,524 W.A. Economic Ownership 33% 44% 77% Annual Net Cash Flow (3) $1 $29 $96 Units Under Construction 1,498 1,182 1,942 Units In-Planning / Future Starts 5,980 9,042 9,373 Rockpoint Value $- $- $454 Rockpoint Value per Share $- (4) $- (5) $4.53 (6) Residential Portfolio NAV $115 $732 $1,785 Residential Portfolio NAV per Share $1.15 (4) $7.30 (5) $17.81 (6)JV Structure - Strategic BenefitsFacilitates capital access opportunities to grow the attractive residential platform that 1 may otherwise be unavailable to Mack-CaliReduces adverse funding consequences to Mack-Cali due to Roseland’s reliance on non- 2 recourse debt3 Deep and experienced multifamily management team nuanced in the dynamics of New Jersey waterfront markets4 Rockpoint is a good, strategic and responsible partner with a vision that is aligned with that of Mack-CaliNote: Dollars in millions except per share values. (1) Represents the closing date of the Roseland acquisition. (2) Represents the day prior to Michael DeMarco joining the CLI executive leadership team. (3) Represents NOI for wholly-owned assets and share of net cash flow after debt service for assets owned in joint ventures.(4) Figure calculated with 99.7mm shares. (5) Figure calculated with 100.3mm shares. (6) Figure calculated with 100.2mm shares. 30 |

|

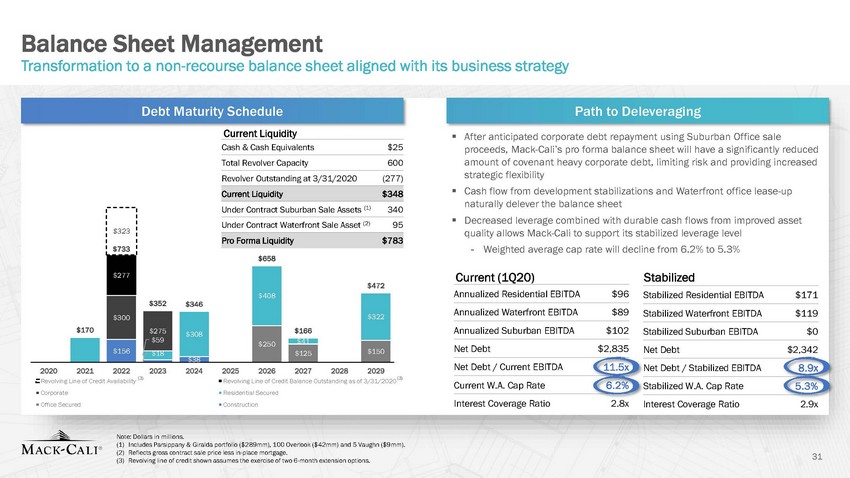

Balance Sheet Management Transformation to a non-recourse balance sheet aligned with its business strategy quality allows Mack-Cali to support its stabilized leverage level Revolving Line of Credit Availability Revolving Line of Credit Balance Outstanding as of 3/31/2020 Current W.A. Cap Rate 6.2% Stabilized W.A. Cap Rate 5.3% Note: Dollars in millions. (1) Includes Parsippany & Giralda portfolio ($289mm), 100 Overlook ($42mm) and 5 Vaughn ($9mm). (2) Reflects gross contract sale price less in-place mortgage. (3) Revolving line of credit shown assumes the exercise of two 6-month extension options. 31 Debt Maturity SchedulePath to Deleveraging Current Liquidity ▪ After anticipated corporate debt repayment using Suburban Office sale Cash & Cash Equivalents$25proceeds, Mack-Cali’s pro forma balance sheet will have a significantly reduced Total Revolver Capacity600amount of covenant heavy corporate debt, limiting risk and providing increased Revolver Outstanding at 3/31/2020(277)strategic flexibility ▪ Cash flow from development stabilizations and Waterfront office lease-up 340naturally delever the balance sheet 95▪ Decreased leverage combined with durable cash flows from improved asset -Weighted average cap rate will decline from 6.2% to 5.3% Current (1Q20)Stabilized Annualized Residential EBITDA$96Stabilized Residential EBITDA$171 Annualized Waterfront EBITDA$89Stabilized Waterfront EBITDA$119 Annualized Suburban EBITDA$102Stabilized Suburban EBITDA$0 Net Debt$2,835Net Debt$2,342 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 Net Debt / Current EBITDA11.5xNet Debt / Stabilized EBITDA8.9x (3) (3) Corporate Residential Secured Office Secured Construction Interest Coverage Ratio2.8xInterest Coverage Ratio2.9x $783 $170 $323 $733 Under Contract Suburban Sale Assets (1) Under Contract Waterfront Sale Asset (2) Pro Forma Liquidity $658 $277 $352 $346 $408 $472 $166 $322 $300 $308 $250 $156 $41 $150 $125 $38 $275 $59 $18 Current Liquidity$348 |

|

Mack-Cali is Poised to Complete its Strategic Transformation Remaining execution will address outstanding areas of investor concern Cali’s financing needs Cash Flow office capex and leasing costs at 24.8% of NOI (1) remaining Suburban Office assets (1) Figures represent recurring residential and recurring office capex and leasing costs as a percentage of residential and office NOI over the last 12 months, respectively. 32 Lease remaining Waterfront office vacancy Continue residential development program Execute remaining Suburban Office asset sales Repay corporate debt to increase strategic flexibility The Board remains open to potential opportunities ▪ The migration to secured project level financing has de-risked the balance sheet Balance Sheet▪ The multifamily financing market has enough scale and liquidity to support Mack-▪ Mack-Cali’s ample liquidity decreases risk of corporate level default ▪ Less capital intensive residential assets lead to greater cash flow generation -Recurring residential capex and leasing is 3.4% of NOI versus recurring ▪ With a transformed portfolio, Mack-Cali is better positioned to fund capital expenditures while servicing debt and sustaining its dividend ▪ Mack-Cali is sufficiently capitalized to fund its office lease-up opportunities ▪ Mack-Cali does not intend to raise corporate equity and will continue capital Dilutionrecycling to fund development ▪ Dilution from Suburban Office sales is offset by new residential development and NOI from higher quality assets Discount to NAV▪ The variation in ascribed valuations will diminish with the disposal of the and expects to launch a strategic process once market conditions improve |

|

Agenda Mack-Cali’s Board has Listened and Been Responsive to Shareholders 1 Strategy, Execution & Performance Driving Growth and Portfolio Transformation 2 Bow Street is Seeking Control of Your Company to Pursue its Own Agenda 3 Shareholders Deserve Directors Maximize Value Best Positioned to 4 5 Appendix 33 |

|

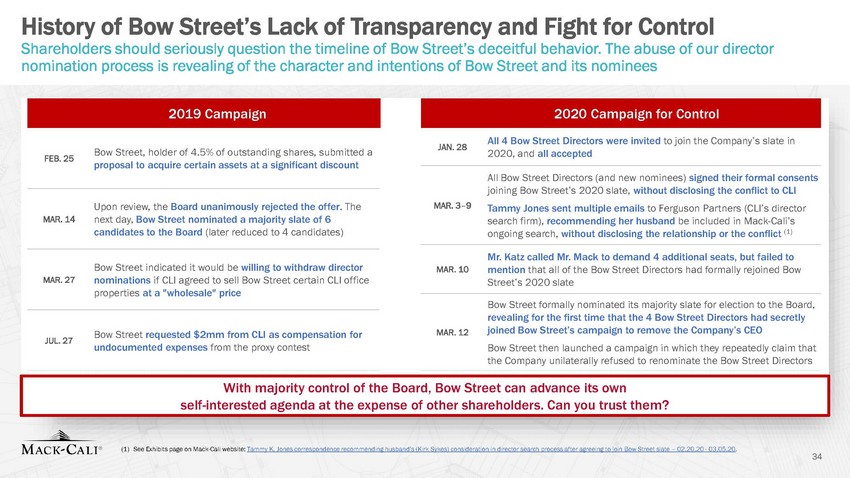

History of Bow Street’s Lack of Transparency and Fight for Control Shareholders should seriously question the timeline of Bow Street’s deceitful behavior. The abuse of our director nomination process is revealing of the character and intentions of Bow Street and its nominees JAN. 28 Bow Street, holder of 4.5% of outstanding shares, submitted a proposal to acquire certain assets at a significant discount 2020, and all accepted Bow Street indicated it would be willing to withdraw director mention that all of the Bow Street Directors had formally rejoined Bow MAR. 10 properties at a "wholesale" price JUL. 27 (1) See Exhibits page on Mack-Cali website: Tammy K. Jones correspondence recommending husband’s (Kirk Sykes) consideration in director search process after agreeing to join Bow Street slate – 02.20.20 - 03.05.20. 34 2019 Campaign 2020 Campaign for Control All 4 Bow Street Directors were invited to join the Company’s slate in FEB. 25 All Bow Street Directors (and new nominees) signed their formal consents joining Bow Street’s 2020 slate, without disclosing the conflict to CLI Upon review, the Board unanimously rejected the offer. TheMAR. 3–9Tammy Jones sent multiple emails to Ferguson Partners (CLI’s director MAR. 14next day, Bow Street nominated a majority slate of 6search firm), recommending her husband be included in Mack-Cali’s candidates to the Board (later reduced to 4 candidates)ongoing search, without disclosing the relationship or the conflict (1) Mr. Katz called Mr. Mack to demand 4 additional seats, but failed to MAR. 27nominations if CLI agreed to sell Bow Street certain CLI officeStreet’s 2020 slate Bow Street formally nominated its majority slate for election to the Board, revealing for the first time that the 4 Bow Street Directors had secretly Bow Street requested $2mm from CLI as compensation forMAR. 12joined Bow Street’s campaign to remove the Company’s CEO undocumented expenses from the proxy contestBow Street then launched a campaign in which they repeatedly claim that the Company unilaterally refused to renominate the Bow Street Directors With majority control of the Board, Bow Street can advance its own self-interested agenda at the expense of other shareholders. Can you trust them? |

|

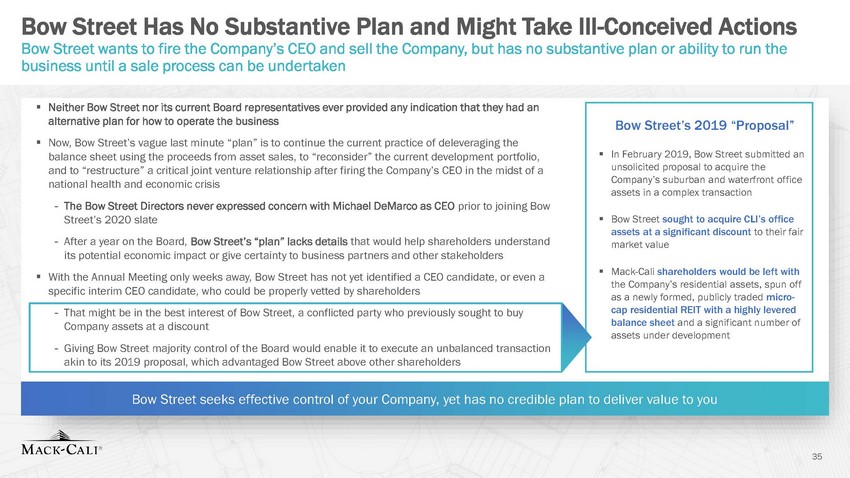

Bow Street Has No Substantive Plan and Might Take Ill-Conceived Actions Bow Street wants to fire the Company’s CEO and sell the Company, but has no substantive plan or ability to run the business until a sale process can be undertaken and to “restructure” a critical joint venture relationship after firing the Company’s CEO in the midst of a its potential economic impact or give certainty to business partners and other stakeholders specific interim CEO candidate, who could be properly vetted by shareholders 35 ▪ Neither Bow Street nor its current Board representatives ever provided any indication that they had an alternative plan for how to operate the business ▪ Now, Bow Street’s vague last minute “plan” is to continue the current practice of deleveraging the balance sheet using the proceeds from asset sales, to “reconsider” the current development portfolio, national health and economic crisis - The Bow Street Directors never expressed concern with Michael DeMarco as CEO prior to joining Bow Street’s 2020 slate - After a year on the Board, Bow Street’s “plan” lacks details that would help shareholders understand ▪ With the Annual Meeting only weeks away, Bow Street has not yet identified a CEO candidate, or even a Company assets at a discount Bow Street seeks effective control of your Company, yet has no credible plan to deliver value to you - That might be in the best interest of Bow Street, a conflicted party who previously sought to buy - Giving Bow Street majority control of the Board would enable it to execute an unbalanced transaction akin to its 2019 proposal, which advantaged Bow Street above other shareholders Bow Street’s 2019 “Proposal” ▪ In February 2019, Bow Street submitted an unsolicited proposal to acquire the Company’s suburban and waterfront office assets in a complex transaction ▪ Bow Street sought to acquire CLI’s office assets at a significant discount to their fair market value ▪ Mack-Cali shareholders would be left with the Company’s residential assets, spun off as a newly formed, publicly traded micro-cap residential REIT with a highly levered balance sheet and a significant number of assets under development |

|

Bow Street’s Nominees Are Not Right for Mack-Cali’s Board Nominees are not independent of Bow Street and are not suited to responsibly oversee the Company’s strategic transformation nominee premium for its shares (1) 2020 to serve as nominee search firm as a after she signed onto did not disclose with U.S. and greater NY committee (6) (1) Served as CEO of NorthStar Realty Europe (“NRE”) when Bow Street campaigned to buy the company – eventually Bow Street granted a standstill and sold its shares at a premium to NorthStar Realty Europe’s external manager, in a transaction that benefited Bow Street at the exclusion of other NRE shareholders (NRE Schedule 13D/A filed on (3) “Tiffany & Co. Announces Chief Executive Officer Transition.” Press Release (February 6, 2017). (4) Bagli, Charles. “Developer That ‘Cracked the Code’ on Modular Building Exits the Business.” The New York Times (published October 5, 2016). (5) Oder, Norman. “Documents Reveal Woes at Pioneering Atlantic Yards Building.” City Limits (published August 31, May 12, 2017). (2) See Exhibits page on Mack-Cali website: Tammy Jones email introducing husband (Kirk Sykes) to Ferguson 36 2015). (6) Monogram Residential Trust 2017 ISS Research Report. Partners – 03.05.20; Memo to Nori G. Lietz debunking her criticisms of board practices – 03.04.20. Alan BatkinFrederic CumenalNori Gerardo LietzMaryAnne GilmartinTammy JonesAkiva KatzMahbod NiaHoward Stern Relationship with Bow Street Investor in Bow Street’s fund Represented Bow Street in settlement negotiations Paid by Bow Street in 2019 to serve as nominee Board member at Blue Nile, a company Bow Street took private with Bain Capital Paid by Bow Street in 2019 to serve as nominee Paid by Bow Street in 2019 to serve as nominee Paid by Bow Street in 2019 to serve as nominee Paid by Bow Street in 2020 to serve as nominee Co-Founder and Managing Partner of Bow Street Personal interest in Bow Street’s control agenda CEO of NRE, where Bow Street campaigned against bad governance and exited after being paid a Paid by Bow Street in Paid by Bow Street in 2020 to serve as Failed to Act With Transparency and Good Faith as Candidate or Director Did not inform Board that he joined Bow Street’s slate; did not raise concerns in a timely manner, waited for proxy contest Did not inform Board that he joined Bow Street’s slate; did not raise concerns in a timely manner, waited for proxy contest Did not inform Board that she joined Bow Street’s slate; did not raise concerns in a timely manner, waited for proxy contest Did not inform Board that she joined Bow Street’s slate; did not raise concerns in a timely manner, waited for proxy contest Recommended her husband to CLI director candidate Bow Street’s slate; relationship (2) - - - - - - Other Concerns - - Abruptly left Tiffany & Co. as CEO in 2017 on the basis of disappointing financial results (3) Demonstrated unconstructive behaviors as a Director (2) Limited time to devote to Board service Led unsuccessful large scale development projects while CEO of Forest City Ratner (4), (5) Material governance concerns identified at her prior public board, where she served on the governance No executive or operating experience at a public company Spent entire career in Europe, no apparent professional experience real estate markets - - Prior Public Company Board Experience Yes Yes No Yes Yes No Only experience was as an insider Only experience was as an insider |

|

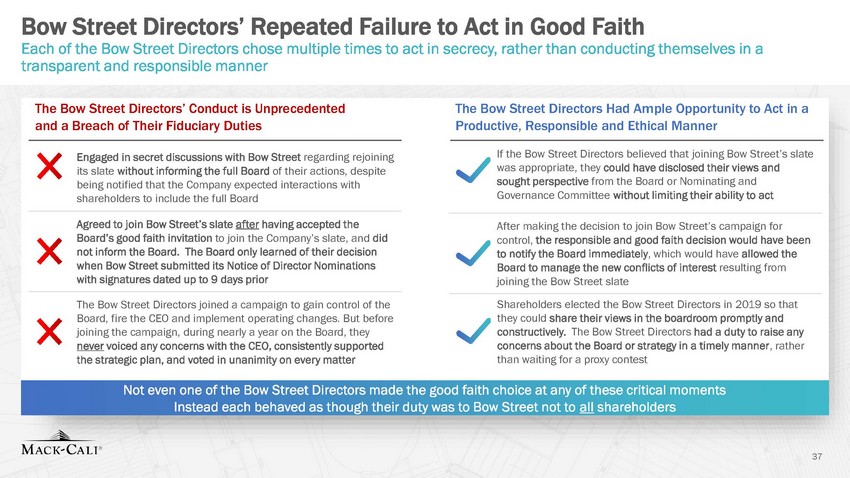

Bow Street Directors’ Repeated Failure to Act in Good Faith Each of the Bow Street Directors chose multiple times to act in secrecy, rather than conducting themselves in a transparent and responsible manner was appropriate, they could have disclosed their views and its slate without informing the full Board of their actions, despite Governance Committee without limiting their ability to act shareholders to include the full Board 37 The Bow Street Directors’ Conduct is UnprecedentedThe Bow Street Directors Had Ample Opportunity to Act in a and a Breach of Their Fiduciary DutiesProductive, Responsible and Ethical Manner Engaged in secret discussions with Bow Street regarding rejoininjpg the Bow Street Directors believed that joining Bow Street’s slate being notified that the Company expected interactions withsought perspective from the Board or Nominating and Agreed to join Bow Street’s slate after having accepted theAfter making the decision to join Bow Street’s campaign for Board’s good faith invitation to join the Company’s slate, and didcontrol, the responsible and good faith decision would have been not inform the Board. The Board only learned of their decisionto notify the Board immediately, which would have allowed the when Bow Street submitted its Notice of Director NominationsBoard to manage the new conflicts of interest resulting from with signatures dated up to 9 days priorjoining the Bow Street slate The Bow Street Directors joined a campaign to gain control of theShareholders elected the Bow Street Directors in 2019 so that Board, fire the CEO and implement operating changes. But beforethey could share their views in the boardroom promptly and joining the campaign, during nearly a year on the Board, theyconstructively. The Bow Street Directors had a duty to raise any never voiced any concerns with the CEO, consistently supportedconcerns about the Board or strategy in a timely manner, rather the strategic plan, and voted in unanimity on every matterthan waiting for a proxy contest Not even one of the Bow Street Directors made the good faith choice at any of these critical moments Instead each behaved as though their duty was to Bow Street not to all shareholders |

|

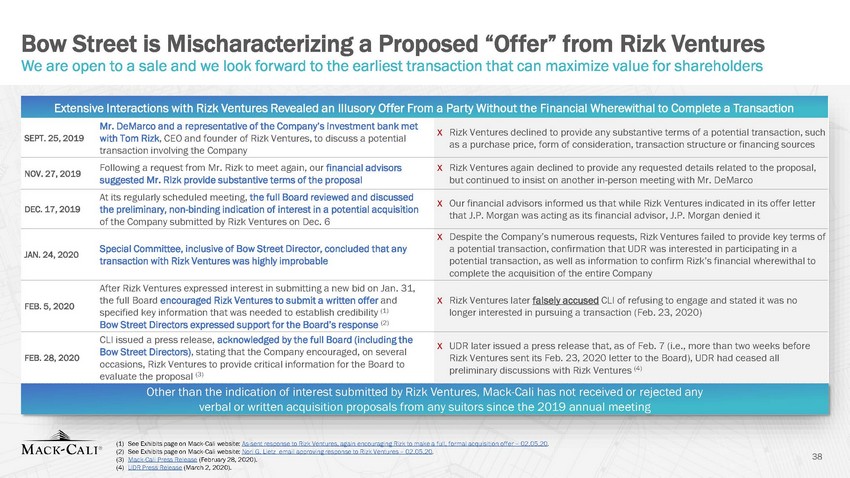

Bow Street is Mischaracterizing a Proposed “Offer” from Rizk Ventures We are open to a sale and we look forward to the earliest transaction that can maximize value for shareholders but continued to insist on another in-person meeting with Mr. DeMarco potential transaction, as well as information to confirm Rizk’s financial wherewithal to longer interested in pursuing a transaction (Feb. 23, 2020) Rizk Ventures sent its Feb. 23, 2020 letter to the Board), UDR had ceased all occasions, Rizk Ventures to provide critical information for the Board to (1) See Exhibits page on Mack-Cali website: As-sent response to Rizk Ventures, again encouraging Rizk to make a full, formal acquisition offer – 02.05.20. (2) See Exhibits page on Mack-Cali website: Nori G. Lietz email approving response to Rizk Ventures – 02.05.20. 38 (3) Mack-Cali Press Release (February 28, 2020). (4) UDR Press Release (March 2, 2020). Extensive Interactions with Rizk Ventures Revealed an Illusory Offer From a Party Without the Financial Wherewithal to Complete a Transaction Mr. DeMarco and a representative of the Company’s investment bank met SEPT. 25, 2019with Tom Rizk, CEO and founder of Rizk Ventures, to discuss a potential transaction involving the Company x Rizk Ventures declined to provide any substantive terms of a potential transaction, such as a purchase price, form of consideration, transaction structure or financing sources NOV. 27, 2019Following a request from Mr. Rizk to meet again, our financial advisors suggested Mr. Rizk provide substantive terms of the proposal x Rizk Ventures again declined to provide any requested details related to the proposal, At its regularly scheduled meeting, the full Board reviewed and discussed DEC. 17, 2019the preliminary, non-binding indication of interest in a potential acquisition of the Company submitted by Rizk Ventures on Dec. 6 x Our financial advisors informed us that while Rizk Ventures indicated in its offer letter that J.P. Morgan was acting as its financial advisor, J.P. Morgan denied it JAN. 24, 2020Special Committee, inclusive of Bow Street Director, concluded that any transaction with Rizk Ventures was highly improbable x Despite the Company’s numerous requests, Rizk Ventures failed to provide key terms of a potential transaction, confirmation that UDR was interested in participating in a complete the acquisition of the entire Company After Rizk Ventures expressed interest in submitting a new bid on Jan. 31, FEB. 5, 2020the full Board encouraged Rizk Ventures to submit a written offer and specified key information that was needed to establish credibility (1) Bow Street Directors expressed support for the Board’s response (2) x Rizk Ventures later falsely accused CLI of refusing to engage and stated it was no CLI issued a press release, acknowledged by the full Board (including the FEB. 28, 2020Bow Street Directors), stating that the Company encouraged, on several evaluate the proposal (3) x UDR later issued a press release that, as of Feb. 7 (i.e., more than two weeks before preliminary discussions with Rizk Ventures (4) Other than the indication of interest submitted by Rizk Ventures, Mack-Cali has not received or rejected any verbal or written acquisition proposals from any suitors since the 2019 annual meeting |

|

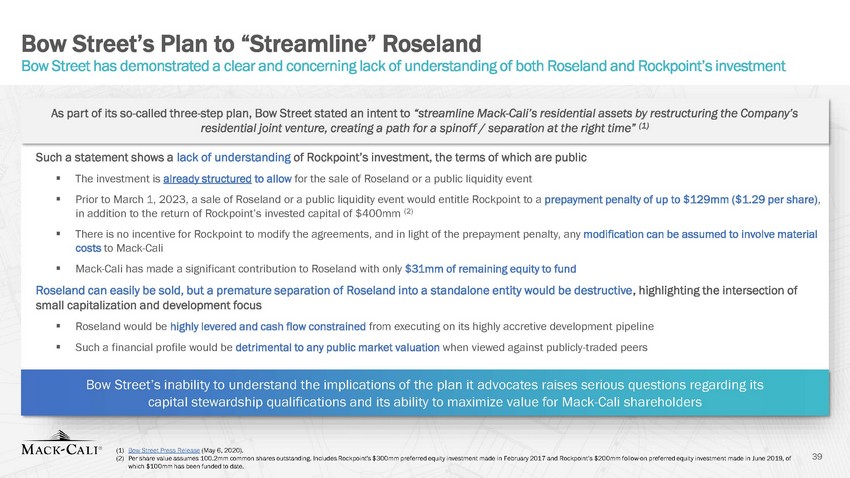

Bow Street’s Plan to “Streamline” Roseland Bow Street has demonstrated a clear and concerning lack of understanding of both Roseland and Rockpoint’s investment As part of its so-called three-step plan, Bow Street stated an intent to “streamline Mack-Cali’s residential assets by restructuring the Company’s residential joint venture, creating a path for a spinoff / separation at the right time” (1) (1) Bow Street Press Release (May 6, 2020). 39 (2) Per share value assumes 100.2mm common shares outstanding. Includes Rockpoint's $300mm preferred equity investment made in February 2017 and Rockpoint’s $200mm follow-on preferred equity investment made in June 2019, of which $100mm has been funded to date. Such a statement shows a lack of understanding of Rockpoint’s investment, the terms of which are public ▪ The investment is already structured to allow for the sale of Roseland or a public liquidity event ▪ Prior to March 1, 2023, a sale of Roseland or a public liquidity event would entitle Rockpoint to a prepayment penalty of up to $129mm ($1.29 per share), in addition to the return of Rockpoint’s invested capital of $400mm (2) ▪ There is no incentive for Rockpoint to modify the agreements, and in light of the prepayment penalty, any modification can be assumed to involve material costs to Mack-Cali ▪ Mack-Cali has made a significant contribution to Roseland with only $31mm of remaining equity to fund Roseland can easily be sold, but a premature separation of Roseland into a standalone entity would be destructive, highlighting the intersection of small capitalization and development focus ▪ Roseland would be highly levered and cash flow constrained from executing on its highly accretive development pipeline ▪ Such a financial profile would be detrimental to any public market valuation when viewed against publicly-traded peers Bow Street’s inability to understand the implications of the plan it advocates raises serious questions regarding its capital stewardship qualifications and its ability to maximize value for Mack-Cali shareholders |

|

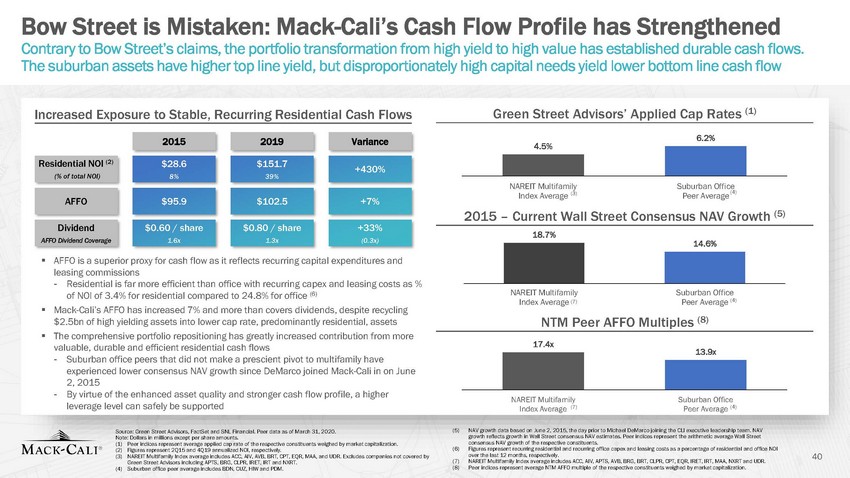

Bow Street is Mistaken: Mack-Cali’s Cash Flow Profile has Strengthened Contrary to Bow Street’s claims, the portfolio transformation from high yield to high value has established durable cash flows. The suburban assets have higher top line yield, but disproportionately high capital needs yield lower bottom line cash flow 4.5% 8% 39% Peer Average (4) Index Average (3) $0.60 / share 1.6x $0.80 / share 1.3x +33% (0.3x) 14.6% NAREIT Multifamily Suburban Office of NOI of 3.4% for residential compared to 24.8% for office (6) Mack-Cali’s AFFO has increased 7% and more than covers dividends, despite recycling ▪ 17.4x valuable, durable and efficient residential cash flows 13.9x leverage level can safely be supported Index Average (7) Peer Average (4) (5) NAV growth data based on June 2, 2015, the day prior to Michael DeMarco joining the CLI executive leadership team. NAV growth reflects growth in Wall Street consensus NAV estimates. Peer indices represent the arithmetic average Wall Street consensus NAV growth of the respective constituents. (6)Figures represent recurring residential and recurring office capex and leasing costs as a percentage of residential and office NOI over the last 12 months, respectively. (7)NAREIT Multifamily Index average includes ACC, AIV, APTS, AVB, BRG, BRT, CLPR, CPT, EQR, IRET, IRT, MAA, NXRT and UDR. (8)Peer indices represent average NTM AFFO multiple of the respective constituents weighed by market capitalization. Source: Green Street Advisors, FactSet and SNL Financial. Peer data as of March 31, 2020. Note: Dollars in millions except per share amounts. (1) (2) (3) Peer indices represent average applied cap rate of the respective constituents weighed by market capitalization. Figures represent 2Q15 and 4Q19 annualized NOI, respectively. NAREIT Multifamily Index average includes ACC, AIV, AVB, BRT, CPT, EQR, MAA, and UDR. Excludes companies not covered by Green Street Advisors including APTS, BRG, CLPR, IRET, IRT and NXRT. Suburban office peer average includes BDN, CUZ, HIW and PDM. 40 (4) Increased Exposure to Stable, Recurring Residential Cash FlowsGreen Street Advisors’ Applied Cap Rates (1) 6.2% $28.6$151.7+430% NAREIT MultifamilySuburban Office $95.9$102.5+7% 2015 – Current Wall Street Consensus NAV Growth (5) 18.7% ▪ AFFO is a superior proxy for cash flow as it reflects recurring capital expenditures and leasing commissions -Residential is far more efficient than office with recurring capex and leasing costs as % Index Average (7)Peer Average (4) $2.5bn of high yielding assets into lower cap rate, predominantly residential, assetsNTM Peer AFFO Multiples (8) ▪ The comprehensive portfolio repositioning has greatly increased contribution from more -Suburban office peers that did not make a prescient pivot to multifamily have experienced lower consensus NAV growth since DeMarco joined Mack-Cali in on June 2, 2015 -By virtue of the enhanced asset quality and stronger cash flow profile, a higherNAREIT MultifamilySuburban Office Dividend AFFO Dividend Coverage AFFO Residential NOI (2) (% of total NOI) Variance 2019 2015 |

|

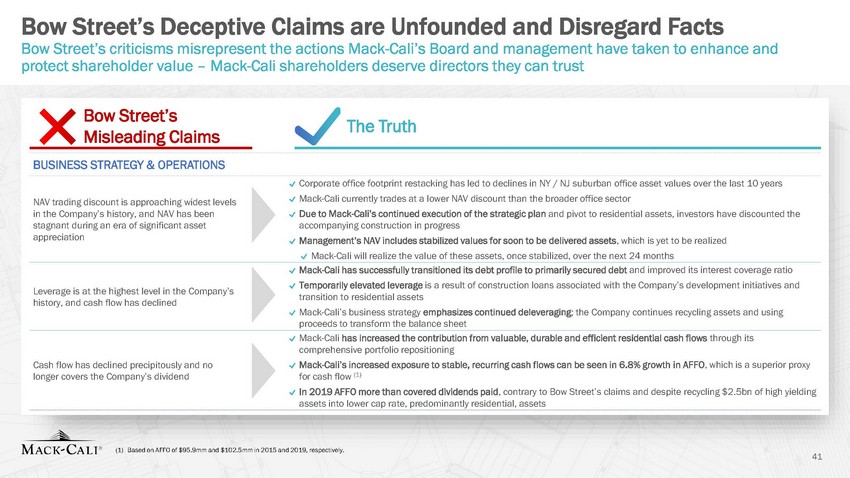

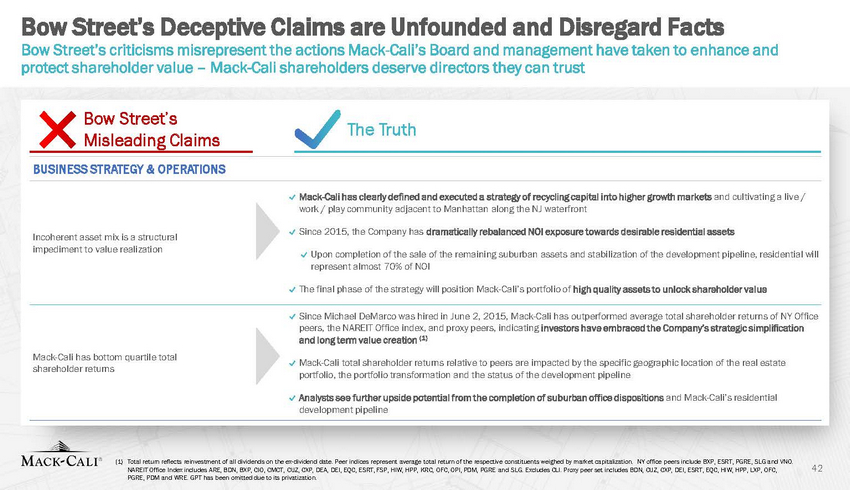

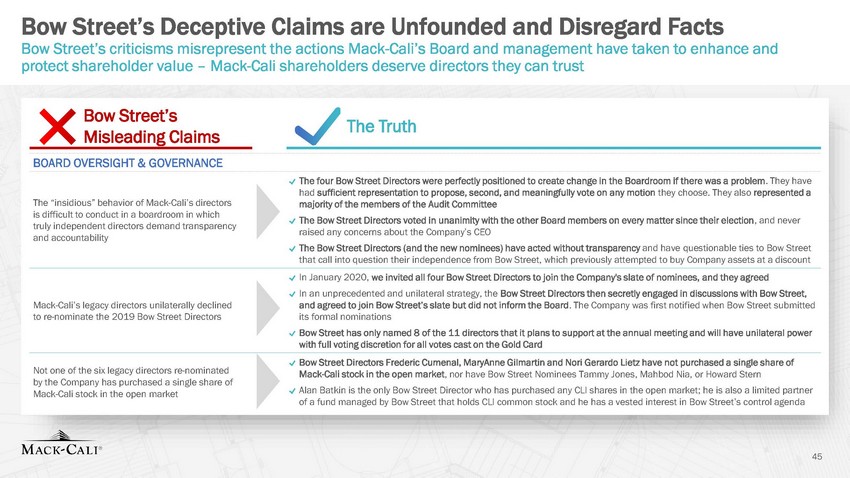

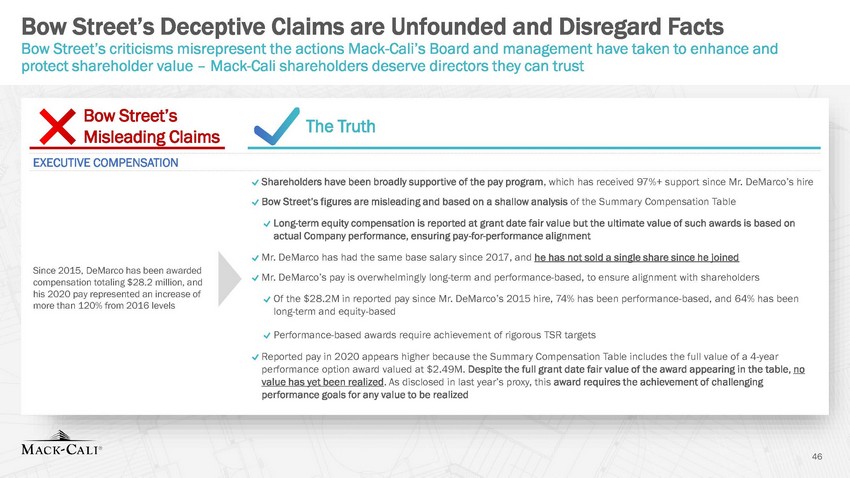

Bow Street’s Deceptive Claims are Unfounded and Disregard Facts Bow Street’s criticisms misrepresent the actions Mack-Cali’s Board and management have taken to enhance and protect shareholder value – Mack-Cali shareholders deserve directors they can trust The Truth Misleading Claims transition to residential assets history, and cash flow has declined (1) Based on AFFO of $95.9mm and $102.5mm in 2015 and 2019, respectively. 41 Bow Street’s BUSINESS STRATEGY & OPERATIONS Corporate office footprint restacking has led to declines in NY / NJ suburban office asset values over the last 10 years NAV trading discount is approaching widest levelsMack-Cali currently trades at a lower NAV discount than the broader office sector in the Company’s history, and NAV has beenDue to Mack-Cali’s continued execution of the strategic plan and pivot to residential assets, investors have discounted the stagnant during an era of significant assetaccompanying construction in progress appreciationManagement’s NAV includes stabilized values for soon to be delivered assets, which is yet to be realized Mack-Cali will realize the value of these assets, once stabilized, over the next 24 months Mack-Cali has successfully transitioned its debt profile to primarily secured debt and improved its interest coverage ratio Leverage is at the highest level in the Company’sTemporarily elevated leverage is a result of construction loans associated with the Company’s development initiatives and Mack-Cali’s business strategy emphasizes continued deleveraging; the Company continues recycling assets and using proceeds to transform the balance sheet Mack-Cali has increased the contribution from valuable, durable and efficient residential cash flows through its comprehensive portfolio repositioning Cash flow has declined precipitously and noMack-Cali’s increased exposure to stable, recurring cash flows can be seen in 6.8% growth in AFFO, which is a superior proxy longer covers the Company’s dividendfor cash flow (1) In 2019 AFFO more than covered dividends paid, contrary to Bow Street’s claims and despite recycling $2.5bn of high yielding assets into lower cap rate, predominantly residential, assets |

|