UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

| Filed by the Registrant x | |

| Filed by a Party other than the Registrant ¨ | |

| Check the appropriate box: | |

| x | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material under §240.14a-12 |

| MACK-CALI REALTY CORPORATION | ||

(Name of Registrant as Specified In Its Charter)

| ||

| (Name of Person(s) Filing Proxy Statement, if other than the Registrant) | ||

| Payment of Filing Fee (Check the appropriate box): | ||

| x | No fee required. | |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

| (1) | Title of each class of securities to which transaction applies: | |

| (2) | Aggregate number of securities to which transaction applies: | |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) | Proposed maximum aggregate value of transaction: | |

| (5) | Total fee paid: | |

| ¨ | Fee paid previously with preliminary materials. | |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |

| (1) | Amount Previously Paid: | |

| (2) | Form, Schedule or Registration Statement No.: | |

| (3) | Filing Party: | |

| (4) | Date Filed: | |

PRELIMINARY PROXY STATEMENT DATED APRIL 23, 2020

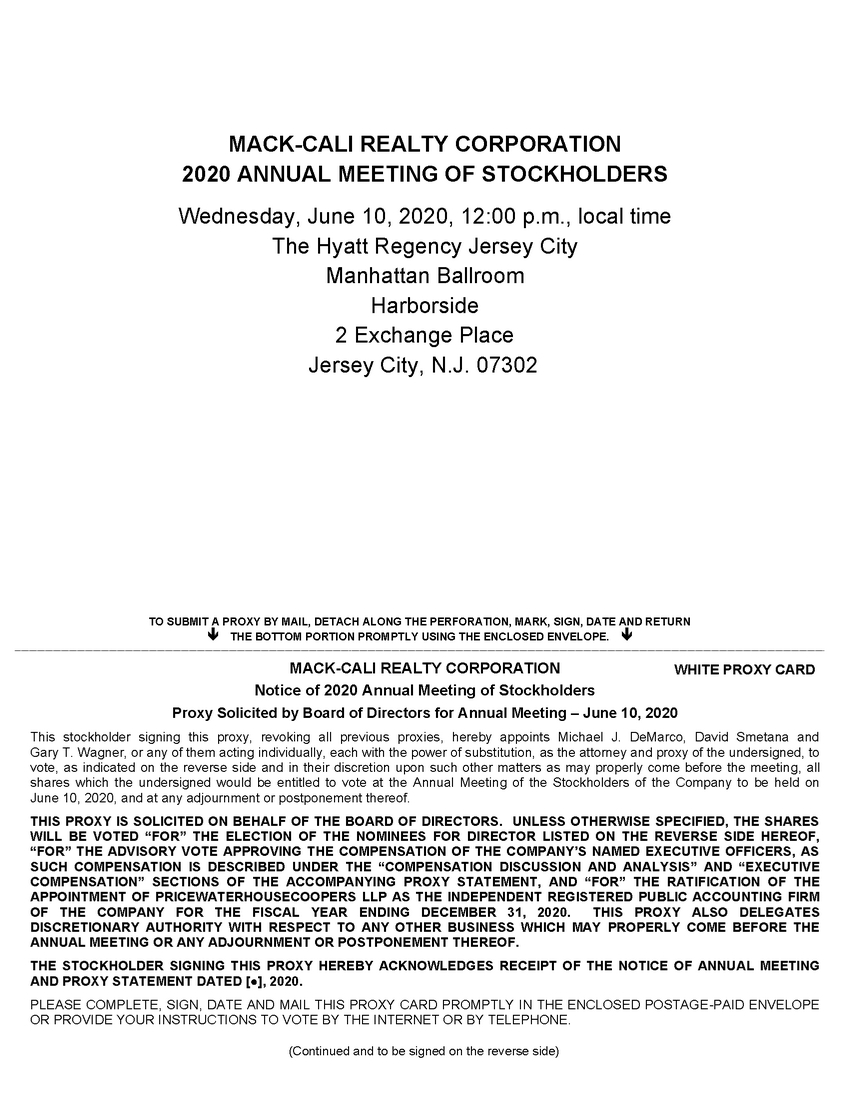

MACK-CALI REALTY CORPORATION

Harborside 3, 210 Hudson Street, Ste. 400

Jersey City, New Jersey 07311

Dear Stockholder:

You are cordially invited to attend the Annual Meeting of Stockholders (referred to as the “Annual Meeting”) of Mack-Cali Realty Corporation, a Maryland corporation (referred to as the “Company,” “we,” “our” or “us”), to be held in the Manhattan Ballroom of The Hyatt Regency Jersey City, Harborside, 2 Exchange Place, Jersey City, New Jersey 07302, on Wednesday, June 10, 2020, at 12:00 p.m., local time, for the following purposes:

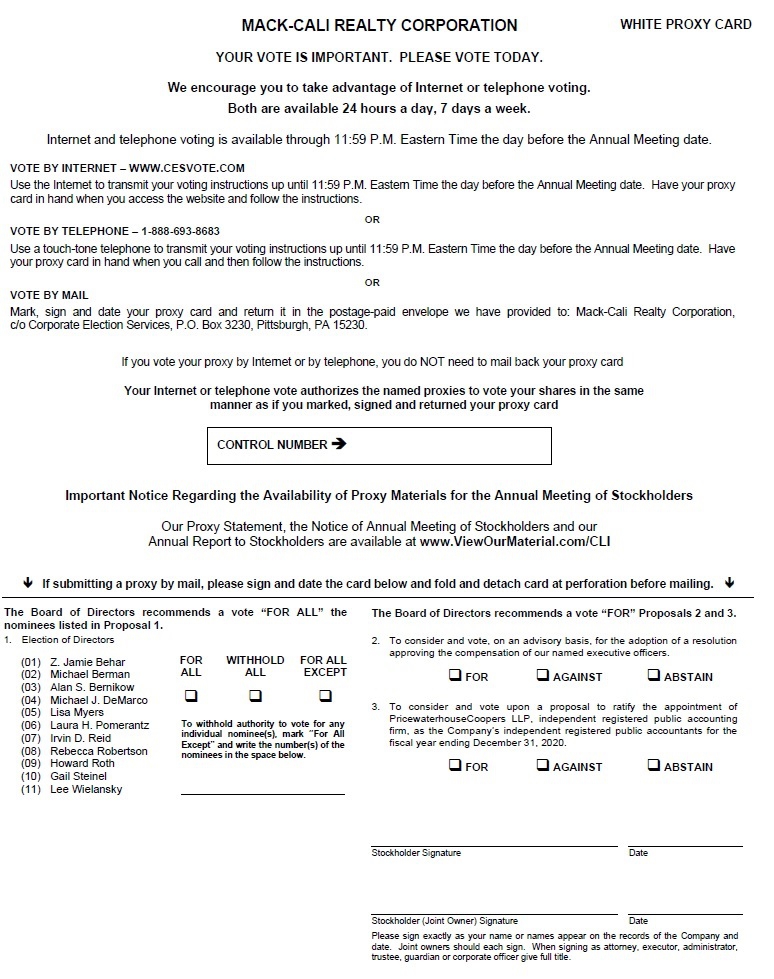

| 1. | To elect eleven persons to the Board of Directors of the Company (referred to as the “Board of Directors”), each to serve a one-year term and until their respective successors are elected and qualified. |

| 2. | To consider and vote, on an advisory basis, for the adoption of a resolution approving the compensation of our named executive officers. |

| 3. | To consider and vote upon a proposal to ratify the appointment of PricewaterhouseCoopers LLP, independent registered public accounting firm, as the Company’s independent registered public accountants for the fiscal year ending December 31, 2020. |

The accompanying Notice of Annual Meeting of Stockholders and proxy statement describe these matters in more detail. We urge you to read this information carefully.

The Board of Directors recommends a vote: FOR each of the Board of Directors’ eleven nominees for election to the Board of Directors named in the Company’s proxy statement, FOR the proposal to adopt, on an advisory basis, a resolution approving the compensation of our named executive officers, and FOR the proposal to ratify the appointment of PricewaterhouseCoopers LLP as the Company’s independent registered public accountants for the fiscal year ending December 31, 2020.

Bow Street Special Opportunities Fund XV, LP (referred to as “Bow Street”) has nominated eight director candidates, including four individuals currently serving on the Board of Directors, for election to the Board of Directors at the Annual Meeting in opposition to the nominees recommended by our Board of Directors. As a result, you may receive solicitation materials, including a Gold proxy card, from Bow Street seeking your proxy to vote for the Bow Street nominees. The Board of Directors has not approved or nominated, and does not endorse or support, any of Bow Street’s director nominees. WE URGE YOU NOT TO SIGN OR RETURN ANY GOLD PROXY CARD SENT TO YOU BY BOW STREET, EVEN AS A PROTEST VOTE AGAINST BOW STREET AND ITS DIRECTOR CANDIDATES. Instead, our Board of Directors recommends that you vote FOR each of the Board of Directors’ eleven director nominees named in the Company’s proxy statement.

If you have already voted using a Gold proxy card sent to you by Bow Street, you can revoke that proxy by voting FOR the Board of Directors’ nominees named in the Company’s proxy statement by using the enclosed WHITE proxy card. Only the latest dated and validly executed proxy that you submit will count at the Annual Meeting.

We recognize the difficulty of conducting the Annual Meeting as an in-person meeting during the current COVID-19 crisis. However, because the Annual Meeting is a contested election as a result of the proxy contest initiated by Bow Street, we are unable to conduct the Annual Meeting as a virtual meeting, as would otherwise be our preference. Your vote is very important. Whether or not you plan to attend the Annual Meeting in person, and regardless of the number of shares of the Company that you own, it is important that your shares be represented and voted at the Annual Meeting. Therefore, our Board of Directors urges you to vote your shares via the Internet or telephone or by mail by promptly marking, signing and dating the enclosed WHITE proxy card and returning it in the enclosed postage-paid envelope.

On behalf of the Board of Directors, we thank you for your support and participation.

| Sincerely, | |

|

Michael J. DeMarco Chief Executive Officer |

If you have questions or need assistance voting your shares, please contact:

1407 Broadway, 27th Floor

New York, New York 10018

proxy@mackenziepartners.com

Call Collect: (212) 929-5500

or

Toll-Free (800) 322-2885

PRELIMINARY PROXY STATEMENT DATED APRIL 23, 2020

MACK-CALI REALTY CORPORATION

Harborside 3, 210 Hudson Street, Ste. 400

Jersey City, New Jersey 07311

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON JUNE 10, 2020

To Our Stockholders:

Notice is hereby given that the Annual Meeting of Stockholders (referred to as the “Annual Meeting”) of Mack-Cali Realty Corporation, a Maryland corporation (referred to as the “Company,” “we,” “our” or “us”), will be held in the Manhattan Ballroom of The Hyatt Regency Jersey City, Harborside, 2 Exchange Place, Jersey City, New Jersey 07302 on Wednesday, June 10, 2020, at 12:00 p.m., local time, for the following purposes:

| 1. | To elect eleven persons to the Board of Directors of the Company (referred to as the “Board of Directors”), each to serve a one-year term and until their respective successors are elected and qualified. |

| 2. | To consider and vote, on an advisory basis, for the adoption of a resolution approving the compensation of our named executive officers, as such compensation is described under the “Compensation Discussion and Analysis” and “Executive Compensation” sections of the attached proxy statement. |

| 3. | To consider and vote upon a proposal to ratify the appointment of PricewaterhouseCoopers LLP, independent registered public accounting firm, as the Company’s independent registered public accountants for the fiscal year ending December 31, 2020. |

The attached proxy statement (referred to as the “Proxy Statement”), which forms a part of this Notice of Annual Meeting of Stockholders and is incorporated herein by reference, includes information relating to these proposals. Additional purposes of the Annual Meeting are to receive reports of officers (without taking action thereon) and to transact such other business as may properly come before the Annual Meeting or any adjournment or postponement thereof.

All stockholders of record as of the close of business on April 16, 2020 are entitled to notice of, and to vote at, the Annual Meeting or any continuation, adjournment or postponement thereof. At least a majority of the outstanding shares of common stock of the Company present in person or by proxy at the Annual Meeting is required for a quorum. You may vote electronically via the Internet or by telephone. The instructions on your enclosed WHITE proxy card describe how to use these convenient services. Of course, if you prefer, you can vote by mail by promptly marking, signing and dating the enclosed WHITE proxy card and returning it in the enclosed postage-paid envelope. If your shares are held by a bank, broker or other agent, please follow the instructions from your bank, broker or other agent to have your shares voted.

The Board of Directors recommends a vote: FOR each of the Board of Directors’ eleven nominees for election to the Board of Directors named in the Proxy Statement, FOR the proposal to adopt, on an advisory basis, a resolution approving the compensation of our named executive officers, and FOR the proposal to ratify the appointment of PricewaterhouseCoopers LLP as the Company’s independent registered public accountants for the fiscal year ending December 31, 2020.

Bow Street Special Opportunities Fund XV, LP (referred to as “Bow Street”) has nominated eight director candidates, including four individuals currently serving on the Board of Directors, for election to the Board of Directors at the Annual Meeting. Bow Street’s nominees are in opposition to the nominees recommended by our Board of Directors. As a result, you may receive solicitation materials, including a Gold proxy card, from Bow Street seeking your proxy to vote for the Bow Street nominees. THE BOARD OF DIRECTORS HAS NOT APPROVED OR NOMINATED, AND DOES NOT ENDORSE OR SUPPORT, ANY OF BOW STREET’S DIRECTOR NOMINEES. WE URGE YOU NOT TO SIGN OR RETURN ANY GOLD PROXY CARD SENT TO YOU BY BOW STREET, EVEN AS A PROTEST VOTE AGAINST BOW STREET AND ITS DIRECTOR CANDIDATES. Instead, our Board of Directors recommends that you vote FOR each of the Board of Directors’ eleven director nominees named in the Proxy Statement.

If you have already voted using a Gold proxy card sent to you by Bow Street, you can revoke that proxy by voting FOR the Board of Directors’ nominees named in the Proxy Statement by using the enclosed WHITE proxy card. Only the latest-dated and validly executed proxy that you submit will count at the Annual Meeting.

We recognize the difficulty of conducting the Annual Meeting as an in-person meeting during the current COVID-19 crisis. However, because the Annual Meeting is a contested election as a result of the proxy contest initiated by Bow Street, we are unable to conduct the Annual Meeting as a virtual meeting, as would otherwise be our preference. THE BOARD OF DIRECTORS APPRECIATES AND ENCOURAGES YOUR PARTICIPATION IN THE ANNUAL MEETING. WHETHER OR NOT YOU PLAN TO ATTEND THE ANNUAL MEETING IN PERSON, IT IS IMPORTANT THAT YOUR SHARES BE REPRESENTED. ACCORDINGLY, PLEASE AUTHORIZE A PROXY TO VOTE YOUR SHARES VIA THE INTERNET OR TELEPHONE OR BY MAIL USING THE ENCLOSED WHITE PROXY CARD. IF YOU ATTEND THE ANNUAL MEETING, YOU MAY WITHDRAW YOUR PROXY, IF YOU WISH, AND VOTE IN PERSON. YOUR PROXY IS REVOCABLE IN ACCORDANCE WITH THE PROCEDURES SET FORTH IN THE PROXY STATEMENT.

| By Order of the Board of Directors, | |

| |

|

Gary T. Wagner General Counsel and Secretary |

April [l], 2020

Jersey City, New Jersey

If you have questions or need assistance voting your shares, please contact:

1407 Broadway, 27th Floor

New York, New York 10018

proxy@mackenziepartners.com

Call Collect: (212) 929-5500

or

Toll-Free (800) 322-2885

TABLE OF CONTENTS

PRELIMINARY PROXY STATEMENT DATED APRIL 23, 2020

MACK-CALI REALTY CORPORATION

Harborside 3, 210 Hudson Street, Ste. 400

Jersey City, New Jersey 07311

PROXY STATEMENT FOR ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON JUNE 10, 2020

INFORMATION ABOUT THE ANNUAL MEETING

This Proxy Statement is furnished to stockholders of Mack-Cali Realty Corporation, a Maryland corporation (the “Company”), in connection with the solicitation by the Board of Directors of the Company (the “Board of Directors”) of proxies in the accompanying form for use in voting at the Annual Meeting of Stockholders of the Company (the “Annual Meeting”) to be held in the Manhattan Ballroom of The Hyatt Regency Jersey City, Harborside, 2 Exchange Place, Jersey City, New Jersey 07302 on Wednesday, June 10, 2020, at 12:00 p.m., local time, and any continuation, adjournment or postponement thereof.

We intend to mail this Proxy Statement, the Notice of Annual Meeting of Stockholders and the accompanying proxy card to all stockholders of record entitled to notice of, and to vote at, the Annual Meeting on or about May 1, 2020.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE ANNUAL MEETING OF STOCKHOLDERS TO BE HELD ON JUNE 10, 2020.

This Proxy Statement, the Notice of Annual Meeting of Stockholders and Our Annual Report to Stockholders are available at http://www.ViewOurMaterial.com/CLI

At the Annual Meeting, the stockholders will consider and vote on the following matters:

| 1. | To elect eleven persons to the Board of Directors, each to serve a one-year term and until their respective successors are elected and qualified. |

| 2. | To consider and vote, on an advisory basis, for the adoption of a resolution approving the compensation of our named executive officers, as such compensation is described under the “Compensation Discussion and Analysis” and “Executive Compensation” sections of this Proxy Statement. |

| 3. | To consider and vote upon a proposal to ratify the appointment of PricewaterhouseCoopers LLP, independent registered public accounting firm, as the Company’s independent registered public accountants for the fiscal year ending December 31, 2020. |

YOUR VOTE IS VERY IMPORTANT. THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” THE ELECTION OF EACH OF THE BOARD OF DIRECTORS’ ELEVEN DIRECTOR NOMINEES NAMED IN THIS PROXY STATEMENT. THE BOARD OF DIRECTORS ALSO RECOMMENDS A VOTE “FOR” THE PROPOSAL TO ADOPT, ON AN ADVISORY BASIS, A RESOLUTION APPROVING THE COMPENSATION OF OUR NAMED EXECUTIVE OFFICERS, AND “FOR” THE PROPOSAL TO RATIFY THE APPOINTMENT OF PRICEWATERHOUSECOOPERS LLP AS THE COMPANY’S INDEPENDENT REGISTERED PUBLIC ACCOUNTANTS FOR THE FISCAL YEAR ENDING DECEMBER 31, 2020. YOU CAN VOTE VIA THE INTERNET OR BY TELEPHONE OR BY MAIL BY COMPLETING, SIGNING AND DATING THE ENCLOSED WHITE PROXY CARD AND RETURNING IT IN THE POSTAGE-PAID ENVELOPE PROVIDED.

Bow Street Special Opportunities Fund XV, LP (“Bow Street”) has nominated eight director candidates, including four individuals currently serving on the Board of Directors, for election to the Board of Directors at the Annual Meeting. Bow Street’s nominees are in opposition to the nominees recommended by our Board of Directors. As a result, you may receive solicitation materials, including a Gold proxy card, from Bow Street seeking your proxy to vote for the Bow Street nominees. THE BOARD OF DIRECTORS HAS NOT APPROVED OR NOMINATED, AND DOES NOT ENDORSE OR SUPPORT, ANY OF BOW STREET’S DIRECTOR NOMINEES. WE URGE YOU NOT TO SIGN OR RETURN ANY GOLD PROXY CARD SENT TO YOU BY BOW STREET, EVEN AS A PROTEST VOTE AGAINST BOW STREET AND ITS DIRECTOR CANDIDATES. Instead, our Board of Directors recommends that you vote FOR each of the Board of Directors’ eleven director nominees named in the Proxy Statement.

1

If you have already voted using a Gold proxy card sent to you by Bow Street, you can revoke that proxy by voting FOR the Board of Directors’ nominees named in the Proxy Statement by using the enclosed WHITE proxy card. Only the latest-dated and validly executed proxy that you submit will count at the Annual Meeting.

Solicitation and Voting Procedures

Solicitation. The Board of Directors is soliciting proxies for the Annual Meeting from our stockholders, and the Company will bear all attendant costs. These costs will include the expense of preparing and mailing proxy materials for the Annual Meeting and reimbursements paid to brokerage firms and others for their expenses incurred in forwarding solicitation material regarding the Annual Meeting to beneficial owners of the Company’s common stock, par value $.01 per share (the “Common Stock”). The Company has retained MacKenzie Partners, Inc., 1407 Broadway, 27th Floor, New York, New York 10018 (“MacKenzie Partners”), to perform various proxy solicitation services in connection with the solicitation of proxies for the Annual Meeting. The Company will pay MacKenzie Partners a fee not to exceed $350,000, plus out-of-pocket expenses, for such services. MacKenzie Partners expects that approximately 30 of its employees will assist in the solicitation of proxies for the Annual Meeting. We may use several of our regular employees, who will not be specifically compensated, to solicit proxies from our stockholders, either personally or via the Internet or by telephone, facsimile or special delivery letter.

As a result of the proxy contest initiated by Bow Street, we may incur substantial additional costs in connection with the solicitation of proxies for the Annual Meeting. These additional solicitation costs are expected to include, among others, the fees and expenses of MacKenzie Partners, fees and expenses of our outside media and communications consulting firm, fees and expenses of outside counsel in connection with a contested election of the Company’s directors, costs associated with SEC filings, increased printing and mailing costs related to additional mailings of solicitation materials to stockholders, and the costs of retaining an independent inspector of elections. Our aggregate expenses related to our solicitation of proxies for the Annual Meeting, excluding salaries and wages of our regular employees, any costs related to any litigation in connection with the Annual Meeting and expenses that we would ordinarily incur in connection with an uncontested annual meeting, are expected to be approximately $[l], of which approximately $[l] has been incurred as of the date of this Proxy Statement.

Under applicable regulations of the Securities and Exchange Commission (the “SEC”), members of the Board of Directors and certain officers and employees of the Company may be deemed to be “participants” with respect to the Company’s solicitation of proxies in connection with the Annual Meeting by reason of their positions as directors and director nominees of the Company or because they may be soliciting proxies on our behalf. Certain information concerning such persons (the “Participants”) is set forth in this Proxy Statement and Annex A hereto.

Householding of Proxy Materials. In accordance with a notice sent previously to beneficial owners holding shares in street name (for example, through a bank, broker or other holder of record) who share a single address with other similar holders, only one Annual Report and Proxy Statement is being sent to that address unless contrary instructions were received from any stockholder at that address. This practice, known as “householding,” is designed to reduce printing and postage costs. Any of such beneficial owners may discontinue householding by writing to the address or calling the telephone number provided for such purpose by their holder of record. Any such stockholder may also request prompt delivery of a copy of the Annual Report or Proxy Statement by contacting the Company at (732) 590-1010 or by writing to Gary T. Wagner, General Counsel and Secretary, Mack-Cali Realty Corporation, Harborside 3, 210 Hudson Street, Ste. 400, Jersey City, New Jersey 07311. Other beneficial owners holding shares in street name may be able to initiate householding if their holder of record has chosen to offer such service, by following the instructions provided by the record holder.

Voting. Stockholders of record may authorize the proxies named in the enclosed WHITE proxy card to vote their shares of Common Stock in the following manner:

| • | by mail, by marking the enclosed WHITE proxy card, signing and dating it, and returning it in the postage-paid envelope provided; |

| • | by telephone, by dialing the toll-free telephone number indicated on the proxy card that you received in the mail with this Proxy Statement, within the United States or Canada, and following the instructions. Stockholders voting by telephone need not return the proxy card; and |

| • | through the Internet, by accessing the World Wide Web site indicated on the proxy card that you received in the mail with this Proxy Statement. Stockholders voting by the internet need not return the proxy card. |

2

Different Color Proxy Cards. Bow Street has nominated eight director candidates, including four individuals currently serving on the Board of Directors, for election to the Board of Directors at the Annual Meeting in opposition to the nominees recommended by our Board of Directors. As a result, you may receive solicitation materials, including a Gold proxy card, from Bow Street seeking your proxy to vote for the Bow Street nominees. The Company is not responsible for the accuracy of any information provided by or relating to Bow Street contained in any proxy solicitation materials filed or disseminated by or on behalf of Bow Street or any other statements that Bow Street may otherwise make.

THE BOARD OF DIRECTORS HAS NOT APPROVED OR NOMINATED, AND DOES NOT ENDORSE OR SUPPORT, ANY OF BOW STREET’S DIRECTOR NOMINEES. WE URGE YOU NOT TO SIGN OR RETURN ANY GOLD PROXY CARD SENT TO YOU BY BOW STREET. Instead, our Board of Directors recommends that you vote “FOR” each of the Board of Directors’ eleven director nominees named in this Proxy Statement.

Voting to “withhold authority” with respect to any of Bow Street’s nominees on its Gold proxy card is not the same as voting “FOR” the Board of Directors’ eleven director nominees. This is because a vote to “withhold authority” with respect to any of Bow Street’s nominees on its Gold proxy card will revoke any previous proxy submitted by you to vote “FOR” the Board of Directors’ eleven director nominees on a WHITE proxy card, as only your latest dated and signed proxy card will be counted at the Annual Meeting. DO NOT RETURN ANY GOLD PROXY CARD SENT TO YOU BY BOW STREET, EVEN AS A PROTEST VOTE AGAINST BOW STREET AND ITS DIRECTOR NOMINEES.

The Company has provided you with the enclosed WHITE proxy card. The Board of Directors recommends using the enclosed WHITE proxy card to vote “FOR” each of the Board of Directors’ eleven director nominees named in this Proxy Statement. If the Company receives a validly executed proxy card from you, your shares will be voted by the Company proxies as indicated in your voting preference selection. We encourage you to cast your vote “FOR” each of the proposals, following the instructions on your WHITE proxy card, as promptly as possible.

If you have already voted using a Gold proxy card sent to you by Bow Street, you have every right and the ability to change your vote. We urge you to revoke that proxy by voting “FOR” the Board of Directors’ eleven director nominees named in this Proxy Statement by using the enclosed WHITE proxy card. Only the latest-dated and validly executed proxy that you submit will count at the Annual Meeting.

Revocability of Proxies. Any proxy given pursuant to this solicitation may be revoked by the person giving it at any time before it is exercised in the same manner in which it was given or by taking any of the following actions:

| • | by delivering to our corporate secretary a written notice of revocation, bearing a date later than the date of the proxy, stating that the proxy is revoked; |

| • | by marking, signing and delivering a new WHITE proxy card, relating to the same shares and bearing a later date than the original proxy card; |

| • | submitting another proxy via the Internet or by telephone or by mail (your latest voting instructions will be followed); or |

| • | by attending the Annual Meeting and voting in person (although attendance at the Annual Meeting, will not, by itself, revoke a proxy, unless you vote in person at the Annual Meeting). |

Written notices of revocation and other communications with respect to the revocation of proxies should be addressed to:

Mack-Cali Realty Corporation

Harborside 3, 210 Hudson Street, Ste. 400

Jersey City, New Jersey 07311

Attention: Gary T. Wagner, General Counsel and Secretary

If your shares are held in “street name,” you may change your vote by submitting new voting instructions to your broker, bank or other nominee. You must contact your broker, bank or other nominee to find out how to do so.

3

If you have previously signed a Gold proxy card sent to you by Bow Street or otherwise voted according to instructions provided by Bow Street, you may change your vote and revoke your prior proxy by signing, dating and returning the enclosed WHITE proxy card in the accompanying envelope or by voting by telephone or via the Internet by following the instructions on the WHITE proxy card. DO NOT RETURN ANY GOLD PROXY CARD SENT TO YOU BY BOW STREET, EVEN AS A PROTEST VOTE AGAINST BOW STREET AND ITS DIRECTOR NOMINEES. Submitting a Gold proxy card sent to you by Bow Street (even if you withhold your vote on the Bow Street nominees) will revoke votes you have previously made via our WHITE proxy card.

Voting in Person. If you plan to attend the Annual Meeting and wish to vote in person, you will be given a ballot at the Annual Meeting. Stockholders who wish to attend the Annual Meeting will be required to present verification of ownership of our Common Stock, such as a bank or brokerage firm account statement, and will be required to present a valid government-issued picture identification, such as a driver’s license or passport, to gain admittance to the Annual Meeting. No cameras, recording equipment, electronic devices, large bags, briefcases or packages will be permitted in the Annual Meeting.

Record Date; Outstanding Shares. The close of business on April 16, 2020 has been fixed as the record date (the “Record Date”) for determining the holders of shares of Common Stock entitled to notice of, and to vote at, the Annual Meeting. Each share of Common Stock outstanding on the Record Date is entitled to one vote on all matters, and there are no cumulative voting rights. As of the Record Date, there were 90,596,547 shares of Common Stock issued and outstanding.

Voting Procedures; Quorum and Votes Required. Stockholder votes will be tabulated by the persons appointed by the Board of Directors to act as inspectors of election for the Annual Meeting. The inspectors of election will also determine whether a quorum is present. The presence at the Annual Meeting of a majority of the outstanding shares of Common Stock, represented either in person or by proxy, will constitute a quorum for the transaction of business at the Annual Meeting.

Shares represented by a properly executed and delivered proxy will be voted at the Annual Meeting and, when instructions have been given by the stockholder, will be voted in accordance with those instructions. If a properly executed and delivered WHITE proxy card does not provide instructions, then the shares represented by that proxy will be voted “FOR” the election of each of the Board of Directors’ eleven nominees for director named below, “FOR” the advisory approval of executive compensation, and “FOR” the ratification of the appointment of PricewaterhouseCoopers LLP as the Company’s independent registered public accounting firm for the fiscal year ending December 31, 2020.

If your shares are held in the name of a bank, broker or other nominees, you will receive instructions from such nominee that you must follow in order to vote your shares. If your shares are not registered in your own name and you plan to vote your shares in person at the Annual Meeting, you should contact your broker or agent to obtain a broker’s proxy card and bring it with you to the Annual Meeting in order to vote. Under New York Stock Exchange (the “NYSE”) Rules, only the ratification of the appointment of PricewaterhouseCoopers LLP as the Company’s independent auditors, as set forth in Proposal No. 3, is considered a “discretionary” item. This means that brokerage firms may vote in their discretion on Proposal No. 3 on behalf of beneficial owners who have not furnished a properly executed proxy card or delivered voting instructions to their broker at least ten days before the date of the Annual Meeting. In contrast, the election of directors as set forth in Proposal No. 1 and the advisory vote to approve executive compensation as set forth in Proposal No. 2 are considered non-discretionary items. This means that brokerage firms that have not received a properly executed proxy card or voting instructions from their clients may not vote on behalf of their clients with respect to Proposals Nos. 1 and 2. These so called “broker non-votes” will be included in the calculation of the number of shares considered to be present at the Annual Meeting for purposes of determining a quorum, but will not be included in the total number of votes cast for the election of directors or the advisory vote for approval of executive compensation.

Proposal No. 1: Election of Directors. A plurality of the votes cast by the holders of shares of Common Stock present in person or by proxy at the Annual Meeting and entitled to vote in the election of directors is required for the election of directors. Accordingly, the eleven director nominees that receive the greatest number of “FOR” votes will be elected to the Board of Directors. Abstentions, failures to vote and broker non-votes are not considered votes cast and, therefore, will have no effect on the outcome of the election of directors.

Proposal No. 2: Advisory Vote to Approve Executive Compensation. The affirmative vote of a majority of the votes cast by the holders of shares of our Common Stock present in person or by proxy at the Annual Meeting and entitled to vote on the proposal is required for the approval, on an advisory basis, of the compensation of the Company’s named executive officers. Abstentions, failures to vote and broker non-votes are not considered votes cast and, therefore, will have no effect on this proposal.

Proposal No. 3: Ratification of the Appointment of Independent Auditors. The affirmative vote of a majority of the votes cast by the holders of shares of our Common Stock present in person or by proxy at the Annual Meeting and entitled to vote on the proposal is required for the ratification of the appointment of PricewaterhouseCoopers LLP as the Company’s independent auditors. Abstentions and failures to vote are not considered votes cast and, therefore, will have no effect on this proposal. Because the ratification of the independent auditors is a discretionary item, we do not anticipate receiving any broker non-votes with respect to this proposal.

4

No Appraisal Rights. Under Maryland law, stockholders will not have appraisal or similar rights in connection with any proposal set forth in this Proxy Statement.

If you have questions or need assistance voting your shares, please contact:

1407 Broadway, 27th Floor

New York, New York 10018

proxy@mackenziepartners.com

Call Collect: (212) 929-5500

or

Toll-Free (800) 322-2885

Statements made in this Proxy Statement may be forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements can be identified by the use of words such as “may,” “will,” “plan,” “potential,” “projected,” “should,” “expect,” “anticipate,” “estimate,” “target,” “continue,” or comparable terminology. Such forward-looking statements are inherently subject to certain risks, trends and uncertainties, many of which the Company cannot predict with accuracy and some of which the Company might not even anticipate and involve factors that may cause actual results to differ materially from those projected or suggested. Readers are cautioned not to place undue reliance on these forward-looking statements and are advised to consider the factors listed above together with the additional factors under the heading “Disclosure Regarding Forward-Looking Statements” and “Risk Factors” in the Company’s Annual Report on Form 10-K, as may be supplemented or amended by the Company’s Quarterly Reports on Form 10-Q, which are incorporated herein by reference. The Company assumes no obligation to update or supplement forward-looking statements that become untrue because of subsequent events, new information or otherwise, except as required under applicable law.

BACKGROUND OF THE SOLICITATION

The following is a chronology of the material events leading up to the filing of this Proxy Statement:

In 2015, the Board of Directors determined that Mack-Cali needed to transform itself to remain competitive and continue to deliver value for its stockholders. To facilitate the changes needed, the Board of Directors installed a new management team, which began to implement a portfolio transformation strategy, led by Michael J. DeMarco, designed to reposition the Company’s asset portfolio around higher quality properties in key markets. Over the past four plus years, the Board of Directors and the management team have transformed Mack-Cali from a suburban real estate company operating in 27 disparate markets to a focused company with high-quality class A office and residential properties, primarily along the New Jersey waterfront. The Board of Directors continues to evaluate on an on-going basis the Company’s strategic direction and reviews alternatives for maximizing stockholder value, including potential strategic transactions.

In February 2019, Bow Street submitted to the Company an unsolicited proposal to acquire the Company’s suburban and waterfront office assets in a complex transaction in which the Company’s office assets would be acquired by Bow Street and its partners at a significant discount to their fair market value, and the Company’s residential assets would be spun off to the Company’s stockholders as a newly formed, publicly traded micro-cap residential REIT with a highly levered balance sheet.

5

On March 10, 2019, Bow Street informed the Company of its intent to nominate a slate of candidates for election to the Board of Directors at the Company’s 2019 annual meeting of stockholders (the “2019 Annual Meeting”) prior to the March 15, 2019 deadline for submitting director nominations under the Company’s bylaws, unless the Company agreed to extend such deadline to continue private discussions with Bow Street regarding its proposal.

In March 2019, the Board of Directors, after careful evaluation of Bow Street’s proposal, in consultation with its financial and legal advisors, unanimously determined that the proposal was inadequate, unworkable and not in the best interests of the Company’s stockholders.

On March 14, 2019, following the Company’s unanimous rejection of Bow Street’s inadequate acquisition proposal, Bow Street nominated a majority slate of six candidates (including two Bow Street principals) for election to the Board of Directors at the 2019 Annual Meeting. Bow Street subsequently reduced its slate to four nominees (eliminating the two Bow Street principals).

On June 12, 2019, four director candidates nominated by Bow Street, namely Alan R. Batkin, Frederic Cumenal, MaryAnne Gilmartin and Nori Gerardo Lietz (collectively, the “Bow Street Directors”), were elected to the Board of Directors at the 2019 Annual Meeting.

For more information relating to the events leading up to the 2019 Annual Meeting, please refer to the section entitled “Background of the Solicitation” in the Company’s definitive proxy statement filed in connection with the 2019 Annual Meeting.

Also on June 12, 2019, the Board of Directors adopted Articles Supplementary to the Company’s charter opting out of certain provisions of the Maryland Unsolicited Takeover Act (MUTA) to eliminate the Board of Directors’ ability to re-classify itself without a stockholder vote.

In June 2019, consistent with the commitments publicly made by the Company prior to and following the 2019 Annual Meeting, the Board of Directors formed a Strategic Review and Valuation Committee (the “Shareholder Value Committee”) comprised of four directors, including two Bow Street Directors, to review, evaluate and make a recommendation to the full Board of Directors regarding the Company’s strategic direction and all available alternatives for maximizing stockholder value, including a potential sale of the Company or its assets. The Shareholder Value Committee retained Goldman Sachs as its independent financial advisors and Willkie Farr & Gallagher LLP as its independent legal advisors to assist the committee in its review.

6

During the period from July 2019 to December 2019, the Shareholder Value Committee, with the assistance of its financial and legal advisors, conducted a comprehensive review of the Company’s strategic direction and all available alternatives for maximizing stockholder value, including a potential strategic transaction involving the Company or its assets.

On July 17, 2019, Bow Street sent a letter to the Board of Directors requesting reimbursement of costs and expenses, totaling approximately $2.0 million, that Bow Street claimed were incurred by Bow Street in connection with its proxy contest to elect directors at the 2019 Annual Meeting. Bow Street did not provide any supporting documentation for the claimed expenses.

On August 1, 2019, the Company and certain members of the Mack family (the “Mack Group”) amended the Contribution and Exchange Agreement, dated as of January 24, 1997, among the Company and members of the Mack Group to terminate the Mack Group members’ rights to designate or nominate members of the Board of Directors.

On August 5, 2019, the Nominating and Corporate Governance Committee of the Board of Directors (the “NCG Committee”) held a special meeting, at which it considered (in consultation with its legal advisors) Bow Street’s request for expense reimbursement. The NCG Committee unanimously determined that reimbursement of Bow Street’s costs and expenses relating to the proxy contest would not be appropriate or in the best interests of the Company and its stockholders. Accordingly, the NCG Committee recommended that the Board of Directors reject Bow Street’s request.

On August 6, 2019, the Board of Directors, acting upon the recommendation of the NCG Committee, determined to reject Bow Street’s request for expense reimbursement. Prior to the Board of Directors’ vote on the matter, the Bow Street Directors informed the Board of Directors that each of them had a conflict of interest due to their relationships with Bow Street and that they would recuse themselves from voting on the matter.

7

Also on August 6, 2019, the Company held an initial orientation session for the Bow Street Directors, at which the Lead Independent Director and other representatives of the Company discussed the plan for integrating the Bow Street Directors onto the Board and reviewed their duties and responsibilities as Mack-Cali directors. The Lead Independent Director also discussed the Bow Street Directors’ committee assignments.

On August 7, 2019, the Company sent a letter to Bow Street rejecting Bow Street’s request for expense reimbursement. The Company’s letter stated that the Board of Directors had considered Bow Street’s request and determined that reimbursement of Bow Street’s costs and expenses relating to the proxy contest would not be appropriate or in the best interests of the Company and its stockholders.

On August 9, 2019, Akiva Katz, Bow Street’s managing partner, sent an email to the Bow Street Directors, in which he expressed Bow Street’s continued interest in an immediate sale of the Company or its assets. Mr. Katz did not copy the Chairman of the Board, the Lead Independent Director, any other Board members or the Company’s General Counsel on his email.

On August 16, 2019, the Company, at the request of the Lead Independent Director and the Chair of the NCG Committee, sent an email to Mr. Katz, stating that it was inappropriate for Bow Street to communicate directly with just the four Bow Street Directors, leaving out all other members of the Board of Directors, and advising Mr. Katz that all future communications should be directed to the Company or the entire Board of Directors.

On September 25, 2019, Michael J. DeMarco and representatives of BofA Securities, Inc. (“BofA Securities”), the Company’s financial advisor, held an in-person meeting with Thomas Rizk, a former CEO of the Company and founder of Rizk Ventures, LLC (“Rizk Ventures”), at Mr. Rizk’s request. At the meeting, Mr. Rizk expressed an interest in a potential transaction involving the Company, but declined to provide any substantive terms of a potential transaction, such as purchase price, form of consideration, transaction structure or financing sources. Mr. Rizk indicated that Rizk Ventures would present a specific proposal for a potential transaction within approximately three weeks. However, no such proposal was delivered by Rizk Ventures to the Company or its financial advisors within such time period.

On October 25, 2019, Bow Street sent a letter to the Board of Directors expressing its desire for an immediate sale of the Company or its assets.

On November 27, 2019, Mr. Rizk contacted representatives of BofA Securities to request another in-person meeting with Mr. DeMarco to present an acquisition proposal. In response, representatives of BofA Securities suggested that Mr. Rizk provide the key substantive terms of the proposal that he wished to present, such as the proposed purchase price, form of consideration, transaction structure and financing sources, to facilitate his discussion with Mr. DeMarco at the meeting. However, Mr. Rizk again declined to provide any details relating to Rizk Ventures’ proposal, but continued to insist on an in-person meeting with Mr. DeMarco.

8

On December 2, 2019, Bow Street sent a letter to the Board of Directors, in which Bow Street indicated that it had “become aware” that a bidder had approached the Company regarding a potential acquisition of Mack-Cali, and expressed concern about the Company’s interactions with that bidder. Bow Street’s letter did not specify the source of Bow Street’s information relating to the bidder or explain how Bow Street became aware of the details of the Board of Directors’ communications with the bidder.

On December 3, 2019, representatives of BofA Securities, at the Company’s request, sent a letter to Rizk Ventures, in which they encouraged Rizk Ventures to submit a written proposal to acquire the Company that would address the key terms of the proposed transaction, including the proposed purchase price and underlying valuation assumptions, transaction structure, equity and debt financing sources, and the identity of any co-bidders or other partners expected to participate in the proposed transaction.

On December 6, 2019, Rizk Ventures delivered to the Company a preliminary, non-binding indication of interest in a potential acquisition of the Company. The indication of interest stated that Rizk Ventures and certain co-bidders would be prepared to acquire the Company for a purchase price in the range of $24.00 to $27.00 per share, which would be paid in a combination of cash and equity securities of UDR, Inc. (“UDR”), which Rizk Ventures described as its “anticipated co-bidder.” The indication of interest also stated that Rizk Ventures expected to secure debt financing from J.P. Morgan. However, the indication of interest did not include the critical information specified by BofA Securities in its December 3, 2019 letter, including, among other key terms, (i) the valuation assumptions underlying the proposed price (which effectively rendered the wide price range specified by Rizk Ventures meaningless), (ii) the proposed equity financing sources and their respective commitment amounts (including the amount of equity proposed to be funded by Rizk Ventures itself), (iii) confirmation from UDR that it was in fact prepared to participate in a potential transaction on the terms described in the indication of interest and (iv) the anticipated sources of debt financing, including confirmation from J.P. Morgan that it was prepared to provide a debt financing commitment for the proposed transaction.

In December 2019, on several occasions, BofA Securities advised Rizk Ventures that in order to present an offer that could be considered and evaluated by the Board of Directors, Rizk Ventures needed to provide the critical information about the proposed transaction that was omitted from its indication of interest. Such critical information was described in detail in two letters sent by BofA Securities, at the Company’s request, to Rizk Ventures. However, despite the detailed guidance provided by BofA Securities, Rizk Ventures never furnished such critical information to the Company or BofA Securities.

9

On December 17, 2019, at its regularly scheduled meeting, the Board of Directors received and discussed the recommendations of the Shareholder Value Committee and its financial advisors, Goldman Sachs, and the Company’s financial advisors, BofA Securities, which recommendations included the sale of the Company’s entire suburban office portfolio and a possible sale of the Company itself, as well as the formation of a special committee to oversee management’s efforts to implement these initiatives. Each of Goldman Sachs’ and BofA Securities’ presentations included a thorough review of the Company’s strategy, market position, asset values and general market conditions. As part of its presentation, each investment bank also discussed several potential bidders who might have interest in acquiring the Company or its individual divisions, if the Company chose to conduct a sale process. Each investment bank noted that despite its conversations with various potentially interested parties and the fact that the strategic review process was publicly announced by the Company, no party (other than Rizk Ventures) had come forth with a verbal or written offer for the Company. Based on the recommendations of the Shareholder Value Committee, the Board of Directors authorized the Company to proceed with the sale of its entire suburban office portfolio. The Board of Directors also authorized the NCG Committee to form a new special committee to provide assistance and oversight to management in reviewing any acquisition proposals that may be received by the Company. In the context of the presentations made by Goldman Sachs and BofA Securities, the Board of Directors also reviewed and discussed the indication of interest submitted by Rizk Ventures. Representatives of BofA Securities reported that even though BofA Securities, on behalf of the Company, had repeatedly encouraged Rizk Ventures to provide certain critical information necessary for the Board of Directors to review and consider the proposal, Rizk Ventures had failed to provide such information. Representatives of BofA Securities also noted that while Rizk Ventures indicated in one of its letters to the Company that J.P. Morgan was acting as its financial advisor, in their subsequent conversations with representatives of BofA Securities and the Company’s management, representatives of J.P. Morgan denied that they were acting as Rizk Ventures’ financial advisor.

On December 19, 2019, the Company issued a press release announcing that, based on the recommendations of the Shareholder Value Committee, the Board of Directors had determined to sell the Company’s entire suburban office portfolio. The press release disclosed that the Company expected to complete the sale of its suburban office portfolio in 2020 and planned to use the available sales proceeds to pay down its corporate-level, unsecured indebtedness.

On January 3, 2020, as directed by the Board of Directors, the NCG Committee formed a special committee (the “Special Committee”) to provide assistance and oversight to management in evaluating any potential offers that may be received to acquire the Company or any substantial portion of its assets, and continue to explore ways to maximize stockholder value. The Special Committee comprised five Mack-Cali directors (including one of the Bow Street Directors), as voting members, and Michael J. DeMarco, ex officio as CEO of the Company, as a non-voting member. Although the NCG Committee invited both Bow Street Directors who previously served on the Shareholder Value Committee to join the Special Committee, one of these directors declined to serve due to the need to attend to other, more pressing outside business matters.

On January 24, 2020, the NCG Committee held a special meeting, at which it formed a sub-committee consisting of Irvin D. Reid, Laura Pomerantz and Michael J. DeMarco (ex officio as CEO of the Company) to select, engage and oversee the work of a professional search firm to assist the NCG Committee in identifying qualified, independent director candidates to replace the Company’s retiring Chairman of the Board, William L. Mack, two additional current directors who will become subject to the Company’s retirement policy for directors in 2021, as well as any of the current directors who do not wish to stand for re-election at the Annual Meeting.

10

Also on January 24, 2020, the Special Committee held a special meeting, at which it received and discussed presentations prepared by BofA Securities and the Company’s management regarding the Company’s current strategy for maximizing stockholder value. In the context of these presentations, the Special Committee also discussed the indication of interest in a potential acquisition of the Company previously submitted by Rizk Ventures. The Special Committee concluded that any transaction with Rizk Ventures was highly improbable, given the absence of confirmation that UDR was in fact interested in participating in a potential transaction (which the Company had requested on three separate occasions) as well as Rizk Ventures’ failure to provide any information to confirm its financial wherewithal to complete the acquisition of the entire Company. The Special Committee also noted that, other than the Rizk Ventures indication of interest, the Company or its financial advisors had not received any acquisition proposals from any interested parties since the 2019 Annual Meeting, even after multiple conversations by BofA Securities and Goldman Sachs with various parties.

On January 28, 2020, the NCG Committee, on behalf of the Board of Directors, invited all of the Company’s current directors (other than Mr. Mack), including the four Bow Street Directors, to join the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting. Each of the Company’s current directors, including each of the four Bow Street Directors, accepted the NCG Committee’s invitation shortly thereafter.

On January 31, 2020, Rizk Ventures sent a letter to the Board of Directors, in which it indicated that it would be interested in submitting a new bid for the Company. The letter indicated that Rizk Ventures’ was no longer proposing a purchase price in the range of $24.00 to $27.00 per share and stated that the previously announced sale of the Company’s suburban office assets “would likely result in lowering its bid.” The letter also included a term sheet that purported to confirm that J.P. Morgan was prepared to provide $1.8 billion debt financing for the proposed transaction. However, the term sheet (which was marked as a “draft” and was missing all of its exhibits) did not indicate a commitment (or even a “highly confident” undertaking) by J.P. Morgan to provide debt financing for a potential acquisition of the whole Company. Rather, it merely summarized the “indicative” terms and conditions on which J.P. Morgan would provide a loan to Rizk Ventures to purchase a limited and unspecified set of assets (described as “property” in the term sheet), which terms and conditions appeared more appropriate for a real property transaction rather than a public company acquisition or a similar public M&A transaction. Nor did the January 31, 2020 letter include any of the other critical information that had been previously requested by BofA Securities on behalf of the Company on several occasions, including but not limited to the sources and amounts of Risk Ventures’ equity funding.

In February 2020, the Company engaged Ferguson Partners, a nationally recognized director search firm, to assist the NCG Committee in identifying qualified, independent director candidates to replace Mr. Mack as well as two additional current directors who will become subject to the Company’s retirement policy for directors in 2021.

11

On February 5, 2020, the Board of Directors sent a letter to Rizk Ventures, in which it again encouraged Rizk Ventures to submit a written offer to acquire the entire Company and comply with the Company’s previous information requests, which had been communicated to Rizk Ventures on several occasions. In particular, the Board of Directors’ letter stated that the Company would be prepared to discuss a fully financed offer to acquire the entire Company at an attractive price. The letter also reiterated that any proposal should specify the proposed equity and debt financing sources, transaction structure, and the identity of the members of the buyer group (including their written agreement to participate and their role in a potential transaction). The Board of Directors’ letter also stated that in addition to such critical information, which was missing from Rizk Ventures’ January 31, 2020 letter, Rizk Ventures had not provided to the Company any confirmation that UDR was prepared to participate in a potential transaction, any information about the amount of equity expected to be contributed by UDR, or evidence that UDR was aware of the fact that Rizk Ventures’ indication of interest described UDR as a potential acquiror. In addition, the Board of Directors’ letter stated that the J.P. Morgan term sheet provided by Rizk Ventures did not seem to contemplate the type of debt financing that would be appropriate for a whole-company acquisition.

Prior to sending the Board of Directors’ letter to Rizk Ventures on February 5, 2020, the Company circulated a draft of the letter to all Board members (including each of the Bow Street Directors) for their review and approval. Later that same day, Nori Gerardo Lietz sent a reply email to the Company (with copies to all other members of the Board of Directors), in which she expressed support for the draft letter and stated that she “agreed with the substance and tone of the letter.”

On February 23, 2020, Rizk Ventures sent a letter to the Board of Directors, in which it falsely accused the Company of refusing to engage with Rizk Ventures regarding its indication of interest and stated that it was no longer interested in pursuing a potential transaction with the Company.

On February 28, 2020, the Company issued a press release in which it publicly disclosed its February 5, 2020 letter to Rizk Ventures. The Company chose to publicly disclose its February 5, 2020 letter in response to two articles previously published by Bloomberg, which repeated the inaccurate and misleading statements made by Rizk Ventures in its February 23, 2020 letter to the Board of Directors. The Company’s press release made it clear that Mack-Cali never refused to engage with Rizk Ventures regarding its acquisition proposal. Rather, on several occasions, the Company and BofA Securities encouraged Rizk Ventures to provide certain critical information that was necessary for the Board of Directors to review and evaluate the proposal. However, Rizk Ventures never provided the requested information. The press release stated that the Company believed that Rizk Ventures’ unfounded accusations were nothing more than an attempt to disguise its own inability to provide satisfactory responses to the Company’s information requests and present a credible offer for the whole Company.

On March 2, 2020, UDR issued a press release indicating that any discussions that UDR may have had with Rizk Ventures regarding a potential transaction involving the Company were merely preliminary and that, as of February 7, 2020 (i.e., more than two weeks before Rizk Ventures sent its February 23, 2020 letter to the Board of Directors), UDR had ceased all such discussions with Rizk Ventures. UDR further confirmed that it had never engaged in direct dialogue or correspondence with the Board of Directors or management team of the Company.

12

From early to mid-March of 2020, the Bow Street Directors engaged in discussions with representatives of Bow Street regarding joining Bow Street’s majority slate of director nominees for election to the Board of Directors at the Annual Meeting. In the course of these discussions, each of the Bow Street Directors met with Bow Street’s legal counsel and executed a written consent to be nominated for election to the Board of Directors on Bow Street’s proxy card. The Bow Street directors chose to take this course of action without informing the Board of Directors or discussing their intentions with the Lead Independent Director, the Chair of the NCG Committee or any other members of the Board of Directors, even though each of them had previously accepted the Board of Directors’ good faith invitation to join the Company’s slate of nominees that was made on January 28, 2020.

On March 9, 2020, after several preliminary discussions by representatives of BofA Securities with representatives of a highly reputable potential bidder (“Party A”), representatives of the Special Committee, members of the Company’s management and representatives of BofA Securities met with representatives of Party A, at Party A’s request, to discuss the possibility of a strategic transaction involving the Company. While no offer was presented or discussed at the meeting, representatives of Party A expressed an interest in a potential strategic transaction with the Company. Although Party A’s representatives indicated that, given the current state of the stock and credit markets resulting from the COVID-19 pandemic, an offer would not be feasible at this time, they also indicated that, as the markets stabilize, Party A would revisit the possibility of making a proposal to acquire the Company. The Company’s representatives encouraged Party A to do so.

On March 10, 2020, Mr. Katz contacted Mr. Mack by telephone to demand that Bow Street be given four additional seats on the Board of Directors at the Annual Meeting (in addition to the four Bow Street Directors). In response, Mr. Mack indicated that he believed that it would be inappropriate for a less than 5% stockholder, such as Bow Street, to have such a vastly disproportionate representation on the Board of Directors. However, Mr. Mack stated that he would inform the Lead Independent Director and the Chair of NCG Committee of his conversation with Mr. Katz.

On March 11, 2020, Mr. Mack contacted Mr. Katz by telephone to advise him that, after discussing the views expressed by Mr. Katz during his telephone conversation with Mr. Mack on March 10, 2020, the NCG Committee continued to believe that Bow Street’s request for a majority control of the Board of Directors was inappropriate.

On March 12, 2020, Bow Street delivered to the Company a formal notice of its intent to nominate a majority slate of eight candidates, including all of the four Bow Street Directors, to stand for election to the Board of Directors at the Annual Meeting. On the same day, Bow Street issued, by press release, a public letter to Mack-Cali stockholders, in which Bow Street announced that it was nominating a majority slate of eight candidates, including the four Bow Street Directors and four additional candidates (including Mr. Katz), for election to the Board of Directors at the Annual Meeting. Bow Street’s letter also called for the removal of the Company’s CEO, Michael J. DeMarco.

13

Following the Company’s receipt of Bow Street’s nomination notice, in light of the Bow Street Directors’ decision to forego the opportunity to be re-nominated on the Company’s slate, the NCG Committee directed Ferguson Partners to expand its search for qualified, independent director candidates to replace the Bow Street Directors on the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting. The NCG Committee instructed Ferguson Partners to focus its search on candidates that had extensive finance, real estate, mergers and acquisitions and corporate governance experience, consistent with the Company’s strategy of selling its suburban office assets and pursuing strategic alternatives. The NCG Committee also emphasized the need for Ferguson Partners to evaluate potential candidates based on their board and leadership experience, diversity, cultural fit and credibility among REIT investors.

On March 13, 2020, Mr. Katz contacted Alan S. Bernikow, the Company’s Lead Independent Director, by telephone to discuss Bow Street’s proxy contest. In the course of their telephone conversation, Mr. Bernikow indicated that in order to avoid another costly and distracting proxy contest, the Board of Directors would be willing to include three of the Bow Street Directors in the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting, if Bow Street agreed to end its proxy contest. In response, Mr. Katz indicated that Bow Street was not prepared to end its proxy contest unless the Company offered Bow Street majority control of the Board of Directors.

On March 16, 2020, the Company issued a press release responding to Bow Street’s public letter to stockholders. The Company’s press release reiterated that the Board of Directors is open to all alternatives to maximize stockholder value, including a potential strategic transaction, and will consider all credible offers. The press release stated that the Board of Directors intends to launch a strategic process and that, in the meantime, the Special Committee will assist the Board of Directors and management in evaluating any acquisition proposals or inquiries that may be received from any interested parties. The press release also noted that, contrary to Bow Street’s allegations, other than the indication of interest submitted by Rizk Ventures in December 2019, which the Special Committee determined was an illusory offer from a party that did not have the financial wherewithal to complete a potential transaction, the Company has not received or rejected any verbal or written acquisition proposals from any suitors since the 2019 Annual Meeting.

On March 23, 2020, the Board of Directors, at its regularly scheduled quarterly meeting, formed a committee (the “Annual Meeting Committee”) consisting of all of the Company’s current directors other than the four Bow Street Directors to review and approve the recommendations of the NCG Committee for the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting and to determine all other matters relating to the proxy contest initiated by Bow Street.

On March 24, 2020, Mr. Bernikow held a telephone conversation with Alan Batkin, one of the Bow Street Directors, at Mr. Batkin’s request, in which Mr. Bernikow again offered to include three of the Bow Street Directors in the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting, if Bow Street agreed to end its proxy contest.

14

On March 27, 2020, Mr. Katz sent a letter to Mr. Bernikow, in which he rejected the Company’s settlement offer. Mr. Katz’s letter indicated that Bow Street was not willing to end its proxy contest for a majority of the Board of Directors, but would be willing to remove the four Bow Street Directors from its slate if the Company irrevocably agreed to include all four of them in the Company’s slate and support their re-election to the Board of Directors in the same manner as it supports the election of the Company’s other nominees. Through its demand for an irrevocable commitment by the Company to nominate and support the re-election of the Bow Street Directors, Bow Street effectively sought to ensure the election of four of its eight candidates, such that Bow Street could have eight seats on the Board of Directors if all Bow Street’s other nominees were elected at the Annual Meeting.

Also on March 27, 2020, Mr. DeMarco sent an email to Mr. Katz, in which he asked him to clarify whether Bow Street would be willing to end its proxy contest if the Company agreed to include all four of the Bow Street Directors in the Company’s slate. Later that same day, Mr. Katz sent a reply email to Mr. DeMarco, in which he indicated that Bow Street was not prepared to end its proxy contest and that it was proposing merely to reduce its slate from eight to four nominees if the Company agreed to include all four of the Bow Street Directors in the Company’s slate.

On March 30, 2020, Mr. Bernikow, on behalf of the Board of Directors, sent an email to Mr. Katz in response to his letter dated March 27, 2020. Mr. Bernikow’s email stated that, as the Company had previously stated, both publicly and privately, the Board of Directors does not believe it would be appropriate to give majority control of the Board of Directors to Bow Street, a less than 5% activist stockholder who previously attempted to purchase the Company’s premium assets at a discount, and whose platform is to dismiss the Company’s CEO and sell its business in the midst of a national health and economic crisis. However, Mr. Bernikow’s email stated that he would share Mr. Katz’s letter with the NCG Committee, which would consider Bow Street’s proposal and make the appropriate recommendation to the Annual Meeting Committee.

Also on March 30, 2020, the Company issued a press release announcing the formation of the Annual Meeting Committee. The Company also announced that the NCG Committee had retained Ferguson Partners to assist the NCG Committee in identifying qualified, independent director candidates to be nominated for election to the Board of Directors at the Annual Meeting to replace Mr. Mack as well as each of the Bow Street Directors, who had chosen to be nominated on Bow Street’s slate and endorsed and sought to advance Bow Street’s self-interested agenda, including gaining control of the Board and firing the Company’s CEO. The press release stated that the NCG Committee was conducting interviews of potential director candidates identified by Ferguson Partners and would make a recommendation to the Annual Meeting Committee with respect to the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting. The press release reiterated the Board of Directors’ openness to all alternatives to maximize stockholder value and confirmed its intent to conduct a strategic process as soon as market conditions improved.

15

On March 31, 2020, Bow Street issued a press release in which it criticized the Board of Directors’ decision not to re-nominate the Bow Street Directors for election to the Board of Directors at the Annual Meeting, despite the fact that these individuals had already agreed to join Bow Street’s slate.

Also on March 31, 2020, the NCG Committee held a special meeting, at which it discussed the results of the comprehensive search conducted by Ferguson Partners, under the supervision of the sub-committee formed by the NCG Committee at its previous meeting (the “Sub-Committee”), over the preceding several weeks to identify potential director candidates to be nominated by the Company for election to the Board of Directors at the Annual Meeting. The NCG Committee reviewed the qualifications, experience and background of approximately 23 potential director candidates identified by Ferguson Partners and interviewed by the Sub-Committee. Based on the recommendations of the Sub-Committee and Ferguson Partners, the NCG Committee selected eight highly qualified, independent director candidates to be invited for an additional round of interviews with members of the Board of Directors and the NCG Committee, upon completion of which the NCG Committee would select and recommend five candidates to the Annual Meeting Committee for inclusion in the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting.

Later in the day on March 31, 2020, the Annual Meeting Committee held a special meeting, at which it discussed the eight director candidates selected by the NCG Committee, including their background, experience and qualifications. The Annual Meeting Committee concluded that each of the eight individuals selected by the NCG Committee is a highly qualified director candidate and determined that each of them should be invited to participate in a second round of interviews with members of the Annual Meeting Committee and the NCG Committee. The Annual Meeting Committee also discussed and approved the recommendation of the NCG Committee to not re-nominate the Bow Street Directors for election to the Board of Directors on the Company’s slate. In making its determination, the Annual Meeting Committee considered the fact that each of the Bow Street Directors had chosen to join the slate of a dissident stockholder who previously attempted to purchase the Company’s premium assets at a discount under threat of a proxy contest and subsequently demanded a $2.0 million fee from the Company, as well as the fact that each of the Bow Street Directors endorsed and sought to advance Bow Street’s self-interested agenda, including gaining control of the Board of Directors, firing the Company’s CEO and forcing an immediate sale of the Company at any price.

During the period from March 31, 2020 through April 5, 2020, members of the Annual Meeting Committee and the NCG Committee conducted interviews of the eight director candidates selected by the NCG Committee.

On April 6, 2020, the Company issued a press release regarding the Board of Directors’ decision not to include the four Bow Street Directors on the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting. The Company’s press release stated that although each of the Bow Street Directors accepted the Board of Directors’ invitation to be included in the Company’s slate of nominees, these directors simultaneously and secretly engaged in discussions with Bow Street regarding joining Bow Street’s slate of nominees for election at the Annual Meeting, and ultimately agreed to join Bow Street’s new 2020 proxy contest to gain control of the Board of Directors by seeking eight seats on the Board of Directors (including the four seats currently held by the Bow Street Directors), remove the CEO and force an immediate sale of the Company at a price acceptable to Bow Street, rather than on terms that maximize value for all stockholders. The Company’s press release explained that, under such circumstances, the NCG Committee had no choice but to withdraw its invitation for the Bow Street Directors to join the Company’s slate, because to do otherwise would assist Bow Street, a less than 5% stockholder, in its efforts to take control of the Company to pursue its own agenda.

16

Also on April 6, 2020, Bow Street issued a press release publicly disclosing the letter sent by Mr. Katz to Mr. Bernikow on March 27, 2020.

Later in the day on April 6, 2020, the Annual Meeting Committee and the NCG Committee held a joint special meeting, at which they discussed the eight director candidates selected by the NCG Committee based on the recommendations of Ferguson Partners, whose interviews had been completed by the Annual Meeting Committee and the NCG Committee prior to the meeting. After an extensive discussion of the background, experience and qualifications of the candidates, as well as their independence as potential Mack-Cali directors, the Annual Meeting Committee, acting upon the recommendation of the NCG Committee, determined to invite the following individuals to join the Company’s slate of nominees for election to the Board of Directors at the Annual Meeting: Z. Jamie Behar, Michael Berman, Howard Roth, Gail Steinel and Lee Wielansky. Each of these individuals subsequently accepted the Annual Meeting Committee’s invitation to join the Company’s slate of nominees.

On April 8, 2020, Mr. Bernikow, on behalf of the Board of Directors, sent a letter to Bow Street, again indicating that the Annual Meeting Committee would be willing to include three of the Bow Street Directors in the Company’s slate, if Bow Street agreed to withdraw all of its director nominations and discontinue its proxy contest. Mr. Bernikow’s letter indicated that the inclusion of the Bow Street Directors in the Company’s slate while Bow Street continues to wage a proxy contest for four additional Board seats would only assist Bow Street, a less than 5% stockholder, to achieve its goal of taking control of the Company in order to pursue its own agenda.

On April 13, 2020, the Annual Meeting Committee held a special meeting, at which the Annual Meeting Committee, acting upon the recommendation of the NCG Committee, approved the Company’s slate of eleven nominees for election to the Board of Directors at the Annual Meeting. In addition to the Company’s incumbent directors – Alan S. Bernikow, Michael J. DeMarco, Lisa Myers, Laura Pomerantz, Rebecca Robertson and Dr. Irvin D. Reid – the Company’s slate of nominees approved by the Annual Meeting Committee includes five new highly qualified, independent nominees: Z. Jamie Behar, Michael Berman, Howard Roth, Gail Steinel and Lee Wielansky.

On April 14, 2020, the Company issued a press release announcing its slate of eleven nominees for election to the Board of Directors at the Annual Meeting.

On April 15, 2020, the Bow Street Directors sent a letter to Messrs. Mack, Bernikow and DeMarco, in which they disputed the view previously publicly expressed by the Company that the Bow Street Directors abdicated their fiduciary duties by agreeing to be named on Bow Street’s slate.

On April 17, 2020, Bow Street filed its preliminary proxy statement in connection with the Annual Meeting.

On April 18, 2020, the Company sent a letter to the Bow Street Directors in response to their April 15, 2020 letter to Messrs. Mack, Bernikow and DeMarco. The Company’s letter reiterated the Company’s view that the Bow Street Directors’ decision to support Bow Street’s campaign to gain control of the Board of Directors, remove the Company’s CEO and pursue an immediate sale of the Company or its assets at a price acceptable to Bow Street, rather than on terms that maximize value for all stockholders, was inconsistent with their fiduciary duties as Mack-Cali directors. The Company’s letter also pointed out that the surreptitious manner in which the Bow Street Directors chose to conduct their discussions with Bow Street regarding joining its slate of nominees, even though each of them had previously accepted the Board of Directors’ invitation to join the Company’s slate of nominees, was inconsistent with the basic principles of director collegiality and good corporate governance. The Company’s letter noted that the actions of the Bow Street Directors were particularly inappropriate in light of the fact that each of them had voted in unanimity with the other Board members on almost every matter over the past year, never raised any concerns with the Company’s CEO and expressed support for the Company’s strategy, as approved by the Board of Directors and carried out by the Company’s management team.

17

VOTING SECURITIES AND PRINCIPAL HOLDERS

Unless otherwise indicated, the following table sets forth information as of February 14, 2020 with respect to each person or group who is known by the Company, in reliance on Schedules 13D and 13G reporting beneficial ownership and filed with the SEC, to beneficially own more than 5% of the Company’s outstanding shares of Common Stock. Except as otherwise noted below, all shares of Common Stock are owned beneficially by the individual or group listed with sole voting and/or investment power.

| Name of Beneficial Owner | Amount and Nature of Beneficial Ownership | Percent of Class (%)(1) | ||||

| The Vanguard Group, Inc.(2) | 12,791,356 | 14.1 | % | |||

| BlackRock, Inc.(3) | 12,632,224 | 14.0 | % | |||

| The Mack Group(4) | 7,475,997 | 7.6 | % | |||

| FMR LLC(5) | 5,575,245 | 6.2 | % | |||

| Madison International Realty Holdings, LLC(6) | 4,746,074 | 5.2 | % | |||

| State Street Corporation(7) | 4,662,489 | 5.2 | % |

| (1) | This percentage was calculated based on 90,595,176 shares of Common Stock issued and outstanding as of December 31, 2019. Unless otherwise noted, the total number of shares outstanding used in calculating this percentage does not include 11,938,395 shares reserved for issuance upon redemption or conversion of outstanding units of limited partnership interest (“Units”) in Mack-Cali Realty, L.P., a Delaware limited partnership (the “Operating Partnership”) through which the Company conducts its real estate activities (including 1,949,601 LTIP Units), or 2,134,246 shares reserved for issuance upon the exercise of stock options granted or reserved for possible grant to certain employees and directors of the Company, except in all cases where such Units or stock options are owned by the reporting person or group. |