|

Index

|

|||||||||||||||

|

2Q 2015 Supplemental

|

|||||||||||||||

|

Category

|

Page

|

||||||||||||||

|

Roseland Overview

|

3

|

||||||||||||||

|

Residential Portfolio Overview

|

4

|

||||||||||||||

|

Operating Communities (Stabilized)

|

5

|

||||||||||||||

|

Operating Communities (Lease-Up)

|

6

|

||||||||||||||

|

In-Construction Communities

|

7

|

||||||||||||||

|

Future Development Communities

|

8 - 9

|

||||||||||||||

|

Capitalization Highlights - Debt and Equity

|

10 - 11

|

||||||||||||||

|

Operating Communities - Repositioning Details

|

12

|

||||||||||||||

|

Appendix

|

13

|

||||||||||||||

|

This Supplemental Operating and Financial Data is not an offer to sell or solicitation to buy any securities of the Company. Any offers to sell or solicitations of the Company shall be made by means of a prospectus. The information in this Supplemental Package must be read in conjunction with, and is modified in its entirety by, the Quarterly on Form 10-Q (the “10-Q”) filed by the Company for the same period with the Securities and Exchange Commission (the “SEC”) and all of the Company’s other public filings with the SEC (the “Public Filings”). In particular, the financial information contained herein is subject to and qualified by reference to the financial statements contained in the 10-Q, the footnotes thereto and the limitations set forth therein. Investors may not rely on the Supplemental Package without reference to the 10-Q and the Public Filings. Any investors’ receipt of, or access to, the information contained herein is subject to this qualification.

|

|||||||||||||||

1

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

We consider portions of this information to be forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of such act. Such forward-looking statements relate to, without limitation, our future economic performance, plans and objectives for future operations and projections of revenue and other financial items. Forward-looking statements can be identified by the use of words such as “may,” “will,” “plan,” “potential,” “projected,” “should,” “expect,” “anticipate,” “estimate,” “continue” or comparable terminology. Forward-looking statements are inherently subject to risks and uncertainties, many of which we cannot predict with accuracy and some of which we might not even anticipate. Although we believe that the expectations reflected in such forward-looking statements are based upon reasonable assumptions at the time made, we can give no assurance that such expectations will be achieved. Future events and actual results, financial and otherwise, may differ materially from the results discussed in the forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements.

Among the factors about which the Company has made assumptions are:

|

·

|

risks and uncertainties affecting the general economic climate and conditions, which in turn may have a negative effect on the fundamentals of our business and the financial condition of our tenants and residents;

|

|

·

|

the value of our real estate assets, which may limit our ability to dispose of assets at attractive prices or obtain or maintain debt financing secured by our properties or on an unsecured basis;

|

|

·

|

the extent of any tenant bankruptcies or of any early lease terminations;

|

|

·

|

our ability to lease or re-lease space at current or anticipated rents;

|

|

·

|

changes in the supply of and demand for our properties;

|

|

·

|

changes in interest rate levels and volatility in the securities markets;

|

|

·

|

our ability to complete construction and development activities on time and within budget, including without limitation obtaining regulatory permits and the availability and cost of materials, labor and equipment;

|

|

·

|

forward-looking financial and operational information, including information relating to future development projects, potential acquisitions or dispositions, and projected revenue and income;

|

|

·

|

changes in operating costs;

|

|

·

|

our ability to obtain adequate insurance, including coverage for terrorist acts;

|

|

·

|

our credit worthiness and the availability of financing on attractive terms or at all, which may adversely impact our ability to pursue acquisition and development opportunities and refinance existing debt and our future interest expense;

|

|

·

|

changes in governmental regulation, tax rates and similar matters; and

|

|

·

|

other risks associated with the development and acquisition of properties, including risks that the development may not be completed on schedule, that the tenants or residents will not take occupancy or pay rent, or that development or operating costs may be greater than anticipated.

|

For further information on factors which could impact us and the statements contained herein, see Item 1A: Risk Factors in our Annual Report on Form 10-K for the year ended December 31, 2014. We assume no obligation to update and supplement forward-looking statements that become untrue because of subsequent events, new information or otherwise.

2

|

Roseland Overview

|

|||||||||||||||||||||||||||

|

2Q 2015 Supplemental

|

|||||||||||||||||||||||||||

|

Roseland, the Residential Division of Mack-Cali Realty Corporation (“MCRC” or the “Company”), serves as the Company’s platform for the strategic transformation of its real estate holdings into the multi-family sector. As reflected through the various components of the Roseland portfolio highlighted in this new Supplemental, the Company forecasts short- and long-term value creation through its multi-family investment. This distinct Supplemental was conceived in mid-June upon installation of new Company leadership, and we anticipate further enhancements and transparency over the coming quarters to allow for full appreciation of the Company’s multi-family expansion.

|

|||||||||||||||||||||||||||

|

Roseland’s exceptional track record and proven commitment to excellence has established it as one of the premier residential and mixed-use developers in the Northeast. Roseland has an industry leading reputation for successful and profitable conception, execution and management of Class A residential developments. Roseland’s entrepreneurial owner/developer approach is hands on from project conception to operations incorporating all responsibilities of development, construction, financing, marketing, leasing and on-going property management.

|

|||||||||||||||||||||||||||

|

Roseland, a full-service real estate company, has a scalable and integrated business platform overseeing operating and in-construction assets, a geographically desirable land portfolio (much of which benefits from historical low, below market land bases) and sourcing of new sites from both strategic Repurposing of MCRC’s office holdings (as further described herein) and new development and acquisition opportunities. We envision continuous annual production from Roseland’s owned/controlled land inventory, thereby generating ongoing value creation and cash flow growth from the Company’s Residential Division.

|

|||||||||||||||||||||||||||

|

Roseland Management Services, the property management division of Roseland, is a best-in class manager with a portfolio of approximately 10,100 apartments under management including properties owned by Roseland as well as third party, institutionally owned assets on a fee-management basis (approximately 4,500). Roseland Management Services’ active presence in the Washington, DC to Boston corridor provides invaluable market-based contributions as Roseland evaluates and develops new opportunities.

|

|||||||||||||||||||||||||||

|

Roseland executive leadership, a cohesive unit since 2003, has an average experience of 17 years at Roseland and 26 years in the industry.

|

|||||||||||||||||||||||||||

|

· Marshall Tycher

|

President

|

||||||||||||||||||||||||||

|

· Andrew Marshall

|

Executive Vice President, Chief Operating Officer

|

||||||||||||||||||||||||||

|

· Ivan Baron

|

Executive Vice President, Chief Legal Counsel

|

||||||||||||||||||||||||||

|

· Bob Cappy

|

Executive Vice President, Chief Financial Officer

|

||||||||||||||||||||||||||

|

· Brenda Cioce

|

President, Roseland Management Services

|

||||||||||||||||||||||||||

|

· Gabriel Shiff

|

Executive Vice President, Finance

|

||||||||||||||||||||||||||

3

|

Residential Portfolio Overview

|

|||||||||||||||||||||||||||

|

2Q 2015 Supplemental

|

|||||||||||||||||||||||||||

|

Overview

|

|||||||||||||||||||||||||||

|

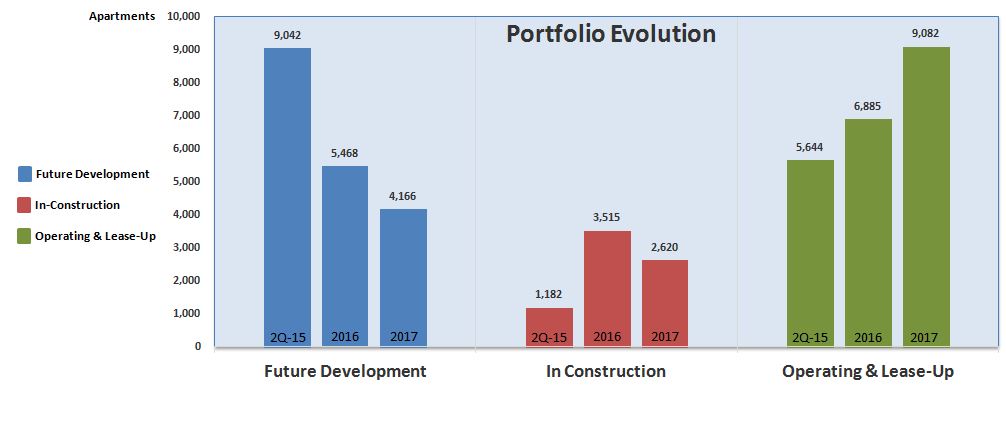

As of June 30, 2015, Roseland had a current Residential Portfolio, excluding communities under third party management contracts, comprised of:

|

|||||||||||||||||||||||||||

|

- Operating & Lease-Up Communities:

|

5,644 apartments

|

||||||||||||||||||||||||||

|

- In-Construction Communities:

|

1,182 apartments

|

||||||||||||||||||||||||||

|

- Future Development Communities:

|

9,042 apartments

|

||||||||||||||||||||||||||

|

Through continuous construction production from its Future Development portfolio, the Company envisions cash flow and value creation growth via expansion of its Operating and Lease-Up communities from 5,644 apartments to 9,082 apartments through year-end 2017 (61% increase). Further, at year-end 2017 we project 2,620 apartments will be in construction, with over 4,000 apartment development opportunities available for ongoing growth.

|

|||||||||||||||||||||||||||