SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant ¨

Filed by a Party other than the Registrant þ

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☐ | Definitive Proxy Statement |

| þ | Definitive Additional Materials |

| ☐ | Soliciting Material Under Rule 14a-12 |

Mack-Cali Realty Corporation

(Name of Registrant as Specified In Its Charter)

Bow Street LLC

Bow Street Special Opportunities Fund XV, LP

A. Akiva Katz

Howard Shainker

Alan R. Batkin

Frederic Cumenal

MaryAnne Gilmartin

Nori Gerardo Lietz

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (check the appropriate box):

| þ | No fee required. |

| ☐ | Fee computed on table below per Exchange Act Rule 14a-6(i)(4) and 0-11. |

| 1) | Title of each class of securities to which transaction applies: | |

| 2) | Aggregate number of securities to which transaction applies: | |

| 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| 4) | Proposed maximum aggregate value of transaction: | |

| 5) | Total fee paid: | |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| 1) | Amount Previously Paid: | |

| 2) | Form, Schedule or Registration Statement No.: | |

| 3) | Filing Party: | |

| 4) | Date Filed: |

BOW STREET SENDS LETTER TO MACK-CALI SHAREHOLDERS HIGHLIGHTING BOARD’S LACK OF OVERSIGHT, BROKEN PROMISES AND DEEP LOYALTY TO CHAIRMAN WILLIAM MACK

Board Change is Desperately

Needed to End Decades-long Underperformance and

Weak Governance Practices Overseen by Chairman Mack and his Hand-Picked Directors

Bow Street’s Director Nominees Will Bring Fresh Perspectives and True Independence to the Board

Urges Mack-Cali Shareholders to VOTE the GOLD Proxy Card FOR the Election of Bow Street’s Four Highly-Qualified, Independent Director Nominees

NEW YORK – May 29, 2019 – Bow Street LLC ("Bow Street"), a New York-based investment firm that beneficially owns approximately 4.5% of the outstanding shares of common stock of Mack-Cali Realty Corporation (“Mack-Cali” or the “Company”) (NYSE: CLI), is today sending a letter to Mack-Cali shareholders highlighting the need for fresh perspectives and rigorous independent oversight in the Mack-Cali Boardroom to end the value destructive and weak governance practices overseen by the Mack-Cali Board of Directors (the “Board”).

Bow Street urges shareholders to protect their investment by voting the GOLD proxy card FOR the election of its four highly-qualified, independent director nominees – Alan Batkin, Frederic Cumenal, MaryAnne Gilmartin, and Nori Gerardo Lietz – in connection with the Company’s Annual Meeting of Shareholders to be held on June 12, 2019. If elected, Bow Street’s nominees will be fierce advocates for shareholders by exploring all meaningful solutions to address the Company’s structural and governance issues and create value for all shareholders.

The full text of the letter is below and available at: http://bowstreetllc.com/mack-cali/.

May 29, 2019

Dear Fellow Mack-Cali Shareholder:

As shareholders of Mack-Cali Realty Corporation (“Mack-Cali” or the “Company”), we have trusted its long-tenured Board of Directors (the “Board”) to steward our capital. However, this Board has failed us. Since taking over as Chairman in 2000, and particularly over the past 15 years, William Mack has overseen strategies that have resulted in a ~70% decrease in dividends and a ~50% share price decline[1]. Over this period, debt has increased from ~4.5x Debt/EBITDA[2] to over 9x Debt/EBITDA[3], reducing Mack-Cali’s financial flexibility and leaving our Company lacking any credible standalone path to the creation of durable shareholder value.

Even over the last several weeks, when presented with credible third-party proposals to acquire all or meaningful portions of Mack-Cali for all-cash consideration, the Board explicitly discouraged suitors, once again thwarting opportunities to create shareholder value. We have repeatedly called on the Board to establish a truly independent committee tasked with evaluating all strategic alternatives for Mack-Cali, including whether and how to pursue a sale of the Company. In response, the Board proposed “window

_________________________________________________

[1] Bloomberg data from 2004 to 2019

[2] Using Citi Group calculation of EBITDA from report dated 11/29/2004 and 3/3/2005

[3] Company disclosed Debt / EBITDA of 9.5x as of 3/31/2019

dressing” – a toothless strategic review committee staffed by directors loyal to Chairman Mack, expressly prohibited from speaking with prospective acquirers or consulting an investment bank. Such a committee lacks both the tools and mandate to create value for Mack-Cali shareholders; its only purpose would be to perpetuate and legitimize the broken status quo.

As the owners of Mack-Cali, we deserve better. We deserve directors who will work to create value for ALL shareholders. We deserve directors who will explore ALL meaningful solutions to address the structural and governance issues that have plagued the Company for decades. This Board must be held accountable for its lack of oversight, broken promises and failed strategies. After decades of poor returns, shareholders finally have a choice. You can vote for four new, highly-qualified independent director nominees or you can support the same four individuals who have overseen 20 years of dividend cuts and share price declines. Please vote today on the GOLD proxy card FOR Bow Street’s four director nominees, who, if elected, will be committed to fixing the Company’s broken structure to benefit ALL shareholders.

The Board is Riddled with Conflicts; “Mack Agreement” Subordinates Common Shareholders

Mack-Cali was established in 1997 through a combination of the Mack Family’s real estate holdings with Cali Realty Corp, a New Jersey REIT. As a result, the Company’s existing governance structure is predicated on an asymmetric agreement that affords the Mack Family control far in excess of its ownership, and significant benefits at the direct expense of common shareholders. In hindsight, this agreement made Mack-Cali’s decades-long underperformance an inevitability.

Known as the “Mack Agreement,” it permits the following:

| · | the Mack family to nominate 3 directors to the Board, which could ultimately result in their control of ~27%[4] of the Board despite owning a mere ~7.7% of the Company; and |

| · | the Company to use commercially reasonable efforts to protect Chairman Mack’s tax position, which has proven to be in direct conflict with shareholder interests. |

Furthermore, the Company, under certain conditions, expressly permits Chairman Mack to transact in real estate deals in direct competition with Mack-Cali; a right he has exercised consistently throughout his long career managing private capital.

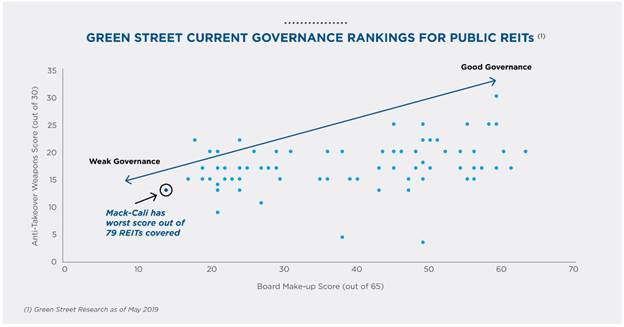

Indeed, throughout his nearly 20-year tenure as Board Chairman, Mr. Mack has competed directly against Mack-Cali for assets – first as Chairman and Founder of Apollo Real Estate Advisors and AREA Property Partners, and currently through Mack Real Estate Group. Mack-Cali’s weak governance policies have persisted for over two decades and have been preserved by an entrenched Board that is blindly loyal to its Chairman. Wall Street research analysts concur. As recently as last month, Mack-Cali received the WORST CORPORATE GOVERNANCE SCORE of the 79 REITs ranked by Green Street research.[5]

________________________________________________

[4] Based on today’s 11 member Board

[5] Green Street Research as of May 2019

Why is the Board so Opposed to a Sale?

Mack-Cali has been rumored to have rebuffed numerous prospective suitors, and is believed to have discouraged credible acquirer interest as recently as three weeks ago. As shareholders, we must ask: why is the Mack-Cali Board so opposed to a sale of the Company?

Our diligence suggests misaligned incentives may be to blame. Here are the facts:

| · | The Mack Family’s investment in the Company is not in common shares, but rather in Mack-Cali’s Operating Partnership units; these units have vastly different tax characteristics than common shares. |

| · | Upon a sale of the Company, common shareholders would be taxed on gains at their outside basis – i.e., stock purchase price. |

| · | Upon a sale of the Company, the Mack Family’s tax liability would likely be significantly higher than that of common shareholders. |

These tax issues precipitate a direct conflict of interest between common shareholders and Operating Partnership unit holders like the Mack Family. We deserve directors who are free of conflicts, and who will exercise their fiduciary duty by exploring all strategic alternatives to create value for all shareholders.

Fresh Perspectives and True Independence Are Desperately Needed in the Boardroom

Mack-Cali’s directors – the majority of whom have served on the Board for over 15 years – have prioritized loyalty to Chairman Mack over their stewardship of your investment. These incumbent directors have preserved their jobs through a complex web of dated corporate defenses, such as limitations that prevent shareholders from acting outside of an annual meeting. Additionally, and perhaps most importantly, this Board has the sole and exclusive power to unilaterally increase the size of the Board and appoint directors to fill vacancies – each without any shareholder approval.

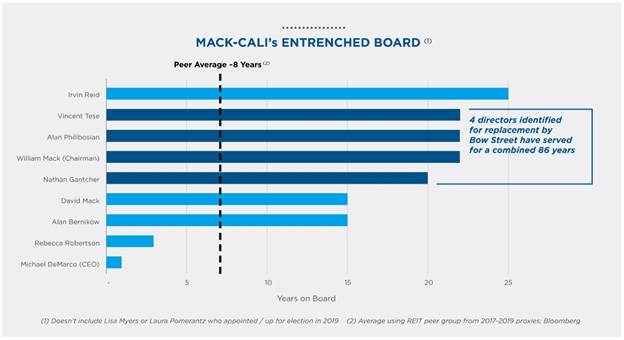

In absence of proper oversight and Board independence, your investment continues to be at risk. As such, Bow Street is nominating four independent director candidates to replace Chairman Mack, Nathan Gantcher, Alan Philibosian and Vincent Tese, who have SERVED A COMBINED 86 YEARS on the Board. In addition to the corporate missteps attributable to these directors inside and beyond the Mack-Cali Boardroom, their long-standing relationships with Chairman Mack suggest they are far from independent and ultimately unfit to serve on any corporate board.

Furthermore, the Board’s lack of independence extends well beyond the directors we are seeking to replace. Other directors include David S. Mack (Chairman Mack’s brother), and current Board nominee Laura H. Pomerantz, who not only served on the Board of Chairman Mack’s AREA Properties, but also was a “Founding” shareholder in NRDC Acquisition Corp., together with Chairman Mack and Mr. Tese.

It is clear: change is required in the Mack-Cali Boardroom to reverse the status quo. Don’t just take our word for it; independent third-parties and other Mack-Cali shareholders agree and have clamored for change:

| · | “Similar to the nine member U.S. Supreme Court…CLI Board of Directors appears to have a ‘for life’ appointment.” (Stifel, 5/7/18) |

| · | “As we have long referenced, we think the CLI Board is too entrenched and in need of an overhaul. Therefore, a new slate would be easily supported by [ISS] and Glass Lewis, and easily approved by shareholders. If something positive does not happen to realize shareholder value soon, the CLI share price will likely head south of $20/sh.” (Stifel, 4/16/19) |

| · | “The Board has overseen exceptionally poor relative stock performance…We think it is no secret that CLI’s Board is long overdue for a refresh. Eight of the 10 current directors have been on the Board since 2005 or earlier, and we think investors might understandably be happy to see all of those directors replaced, given the stock’s performance.” (SunTrust Robinson Humphrey, 5/1/19) |

| · | “…ultimately, the proof is in the pudding, right. And if the stock is where the stock is, at this point, perhaps fresh perspectives are needed in the boardroom …Shareholders are not happy.” (Citi, Q3 2018 Earnings Call, 11/1/18) |

| · | “…board oversight, board leadership, board composition has to change alongside management for the better of shareholders that own your stock.” (Citi, Q4 2017 Earnings Call, 2/22/18) |

| · | “The Company’s board has been pretty ineffective over time.” (JP Morgan, 3/27/19) |

| · | “CalPERS staff attends the Mack-Cali AGM; votes “against” Co. chairman W. Mack…” (@CalPERS, May 2014) |

Bow Street’s Nominees Will Bring Fresh Perspectives and Rigorous, Independent Oversight to the Boardroom

Two decades of failed strategies have left Mack-Cali lacking any credible standalone path to sustainable shareholder value creation. It is time to put an end to the value destructive and weak governance practices overseen by Chairman Mack and his hand-picked directors.

It is time for a reconstituted Board capable of providing truly independent oversight and willing to evaluate all opportunities to unlock shareholder value.

Bow Street’s four independent director nominees – Alan Batkin, Frederic Cumenal, MaryAnne Gilmartin, and Nori Gerardo Lietz – are accomplished business leaders with deep board and governance experience, and real estate operations, development and investment expertise. If elected, Bow Street’s nominees will be fierce advocates for all shareholders.

A NEW DAY AT MACK-CALI must begin at the very top. New oversight is needed to assure the Company’s future.

Join us in VOTING THE GOLD PROXY CARD for Bow Street’s nominees today.

Respectfully,

|

|

|

Akiva Katz Managing Partner |

Howard Shainker Managing Partner |

Bow Street encourages all Mack-Cali shareholders to visit http://bowstreetllc.com/mack-cali/ to review additional information about THE CASE FOR CHANGE AT MACK-CALI.

| Your Vote Is Important, No Matter How Many or How Few Shares You Own! |

| Please vote today by telephone, via the Internet or |

| by signing, dating and returning the enclosed GOLD proxy card. |

| Simply follow the easy instructions on the GOLD proxy card. |

| If you have questions about how to vote your shares, please contact: |

| INNISFREE M&A INCORPORATED |

| Shareholders May Call Toll-free: (877) 800-5182 |

| Banks and Brokers May Call Collect: (212) 750-5833 |

| REMEMBER: |

| Please simply discard any White proxy card that you may receive from Mack-Cali. Returning a |

| White proxy card – even if you “withhold” on the Company's nominees –will revoke any vote |

| you had previously submitted on Bow Street’s GOLD proxy card. |

About Bow Street LLC

Founded in 2011, Bow Street is a New York-based investment manager that partners with institutional investors and family offices globally to invest opportunistically across public and private securities.

Media Contacts

Gasthalter & Co.

Jonathan Gasthalter/Amanda Klein

(212) 257 4170

Investor Contacts

Innisfree M&A Incorporated

Scott Winter/Gabrielle Wolf

(212) 750 5833

Important Information

Bow Street LLC ("Bow Street"), A. Akiva Katz, Howard Shainker, Alan R. Batkin, Frederic Cumenal, MaryAnne Gilmartin, and Nori Gerardo Lietz (collectively, the "Participants") have filed with the Securities and Exchange Commission (the "SEC") a definitive proxy statement and accompanying form of proxy to be used in connection with the solicitation of proxies from shareholders of Mack-Cali Realty Corporation (the "Company"). All shareholders of the Company are advised to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants, as they contain important information, including additional information related to the Participants. The definitive proxy statement and an accompanying proxy card is being furnished to some or all of the Company's shareholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov/ or from the Participants' proxy solicitor, Innisfree M&A Incorporated.

Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the definitive proxy statement on Schedule 14A filed by Bow Street with the SEC on May 1, 2019. This document is available free of charge from the sources indicated above.

Disclaimer

This material does not constitute an offer to sell or a solicitation of an offer to buy any of the securities described herein in any state to any person. In addition, the discussions and opinions in this press release are for general information only, and are not intended to provide investment advice. All statements contained in this press release that are not clearly historical in nature or that necessarily depend on future events are “forward-looking statements,” which are not guarantees of future performance or results, and the words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” and similar expressions are generally intended to identify forward-looking statements. The projected results and statements contained in this press release that are not historical facts are based on current expectations, speak only as of the date of this press release and involve risks that may cause the actual results to be materially different. Certain information included in this material is based on data obtained from sources considered to be reliable. No representation is made with respect to the accuracy or completeness of such data, and any analyses provided to assist the recipient of this presentation in evaluating the matters described herein may be based on subjective assessments and assumptions and may use one among alternative methodologies that produce different results. Accordingly, any analyses should also not be viewed as factual and also should not be relied upon as an accurate prediction of future results. All figures are unaudited estimates and subject to revision without notice. Bow Street disclaims any obligation to update the information herein and reserves the right to change any of its opinions expressed herein at any time as it deems appropriate. Past performance is not indicative of future results.