Exhibit 2

15 Years is a Long Time: The Case For Change At Mack - Cali May 2019

Disclaimer 1 This presentation, the materials contained herein, and the views expressed herein (this “Presentation”) are for discussion and general informational purposes only . This Presentation does not have regard to the specific investment objective, financial situation, suitability, or the particular need of any specific person who may receive this presentation, and should not be taken as advice on the merits of any investment decision . In addition, this Presentation should not be deemed or construed to constitute an offer to sell or a solicitation of any offer to buy any security described herein in any jurisdiction to any person, nor should it be deemed as investment advice or a recommendation to purchase or sell any specific security . Nor should this Presentation be considered to be an offer to sell or the solicitation of an offer to buy any interests in any fund managed by Bow Street LLC or any of its affiliates ("Bow Street”) . Such an offer to sell or solicitation of an offer to buy interests may only be made pursuant to definitive subscription documents . The views expressed herein represent the current opinions as of the date hereof of Bow Street and are based on publicly available information regarding Mack - Cali Realty Corporation (“Mack - Cali” or the “Company”) . Certain financial information and data used herein have been derived or obtained from, without independent verification, public filings, including filings made by Mack - Cali with the Securities and Exchange Commission (“SEC”) and other sources . Bow Street shall not be responsible for or have any liability for any misinformation contained in any SEC or other regulatory filing, any third party report, or this Presentation . All amounts, market value information, and estimates included in this Presentation have been obtained from outside sources that Bow Street believes to be reliable or represent the best judgment of Bow Street as of the date of this Presentation . Bow Street is an independent company, and its opinions and projections within this Presentation are not those of Mack - Cali and have not been authorized, sponsored, or otherwise approved by Mack - Cali . The information contained within the body of this Presentation is supplemented by footnotes which identify Bow Street’s sources, assumptions, estimates, and calculations . This information contained herein should be reviewed in conjunction with the footnotes . In addition, the information contained herein reflects projections, market outlooks, assumptions, opinions and estimates made by Bow Street as of the date hereof that may constitute forward - looking statements . Such forward - looking statements are based on certain assumptions and involve certain risks and uncertainties, including risks and changes affecting industries generally and the Company specifically and are subject to change without notice at any time . Given the inherent uncertainty of projections and forward - looking statements, you should be aware that actual results may differ materially from the projections and other forward - looking statements contained herein due to reasons that may or may not be foreseeable . Therefore, Bow Street does not represent that any opinion or projection will be realized, and Bow Street offers no assurances as to the price of Company securities in the future . While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented, the information or views contained herein, nor concerning any forward - looking statements . Bow Street has an economic interest in the price movement of the securities discussed in this presentation, but Bow Street’s economic interest is subject to change at any time . Bow Street has not sought or obtained consent from any third party to use any statements or information indicated herein as having been obtained or derived from statements made or published by third parties, nor has it paid for any such statements . Any such statements or information should not be viewed as indicating the support of such third party for the views expressed herein . Bow Street does not endorse third - party estimates or research which are used in this presentation solely for illustrative purposes . All registered or unregistered service marks, trademarks and trade names referred to in this Presentation are the property of their respective owners, and Bow Street’s use herein does not imply an affiliation with, or endorsement by, the owners of these service marks, trademarks and trade names or the goods and services sold or offered by such owners . Bow Street, A . Akiva Katz, Howard Shainker, Alan R . Batkin, Frederic Cumenal, MaryAnne Gilmartin, and Nori Gerardo Lietz (collectively, the "Participants") have filed with the Securities and Exchange Commission (the "SEC") a definitive proxy statement and accompanying form of proxy to be used in connection with the solicitation of proxies from shareholders of Mack - Cali Realty Corporation (the "Company") . All shareholders of the Company are advised to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants, as they contain important information, including additional information related to the Participants . The definitive proxy statement and an accompanying proxy card is being furnished to some or all of the Company's shareholders and is, along with other relevant documents, available at no charge on the SEC website at http : //www . sec . gov/ or from the Participants' proxy solicitor, Innisfree M&A Incorporated . Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the definitive proxy statement on Schedule 14 A filed by Bow Street with the SEC on May 1 , 2019 . This document is available free of charge from the sources indicated above .

2 (1) Buffett, Warren. The Essays of Warren Buffett: Lessons for Corporate America , Selected, Arranged, and Introduced by Lawrence A. Cunningham (1998), available at http://csinvesting.org/wp - content/uploads/2015/05/Essays - of - Warren - Buffett - _ - Lessons - for - Corporate - America_Cunningham.pdf . “Unfortunately, "long - term" gives directors a lot of wiggle room. If they lack either integrity or the ability to think independently, directors can do great violence to shareholders while still claiming to be acting in their long - term interest” - Warren Buffett (1)

3 (1) Green Street Research report 4/13/1998 (2) Unadjusted stock price as of 3/15/2019 (3) Blomberg transcript: Mack - Cali Q1 2018 earnings call 5/3/2018 “The [Mack - Cali] deal…brought the valuable relationships and deal - making skills of Bill Mack to the REIT” - Analyst Research Note from April 13 th , 1998 (1) describing benefits of Current Chairman William Mack joining Mack - Cali’s Board of Directors; CLI Stock Price: $38.88/share (~80% higher than current levels (2) ) “…and there's another question on the table, which [I] always ask at each board meeting is, should Mack - Cali exist …” - Michael DeMarco, CEO of Mack - Cali – May 3 rd , 2018 (3)

Table of Contents 1) Executive Summary 2) 15 Years of Underperformance: The Legacy of Mack - Cali’s Current Board 3) Governance: Entrenched Board, Myriad Conflicts 4) Situation Today: Trapped In Current Structure (Hope is Not a Strategy) 5) Six Fallacies: the Board’s Side of the Story 6) A New Day at Mack - Cali: Independent Leadership, Structural Change 4

Executive Summary 5

The Case For Long - Overdue Structural Change at Mack - Cali 6 Despite a wide - spread real estate boom, Mack - Cali’s Board has destroyed shareholder value for decades – detailed review of strategic alternatives is required to unlock shareholder value After decades of underperformance, mismanagement, and weak governance, we believe structural change is required to unlock value at Mack - Cali; current Board incapable of effecting this change • Mack - Cali (“CLI” or “Company”) has underperformed its peers on a total return basis for decades, with bottom quartile shareholder returns over 3, 5, 7, 10, 15, and 20 year periods (1) • The Board of Directors responsible for this underperformance largely remains in place. Defying best - practice governance standards, the majority of Mack Cali’s current directors have served on its board for over 15 years • Despite attractive assets, years of missteps by the Board and management have left the Company in an intractable state – over - levered and under - occupied, lacking a credible path to sustainable shareholder value creation • Bow Street is nominating 4 highly capable, independent Directors to ensure that all alternatives for value creation are explored vigorously by the Board • We believe Mack - Cali’s value can never be realized in its current structure; a robust, transparent strategic review overseen by an independent Board of Directors is essential to the Company’s future (1) Using peers primarily identified in Mack - Cali’s proxy statements; performance data taken as of 3/15/2019 (last unaffected tradin g date prior to public announcement of Bow Street’s intent to nominate Directors). Note: all share performance metrics calculated as of 3/15/2019 in presentation

Bow Street: Who We Are and Why We Are Here 7 We believe the current Board has failed Mack - Cali shareholders; new Board leadership essential to determining the right strategic path forward Bow Street LLC owns ~4.5% of Mack - Cali’s outstanding shares • Bow Street LLC is a New - York based investment manager founded in 2011 that partners with institutional investors and family offices globally to invest opportunistically across idiosyncratic markets and situations – This proxy filing is our first such submission since our firm’s founding; we are not activists – We own assets in both the public and private markets, and have extensive real estate experience • Endeavoring to work constructively with management to address the Company’s issues, in February of 2019, Bow Street - along with DWREI - formulated a proposal to acquire approximately half of Mack - Cali’s assets in a corporate transaction we believed was worth up to $27 - 29 per CLI Share • We believe Mack - Cali should evaluate all strategic alternatives to maximize value, including a sale to the highest bidder in a robust and transparent process

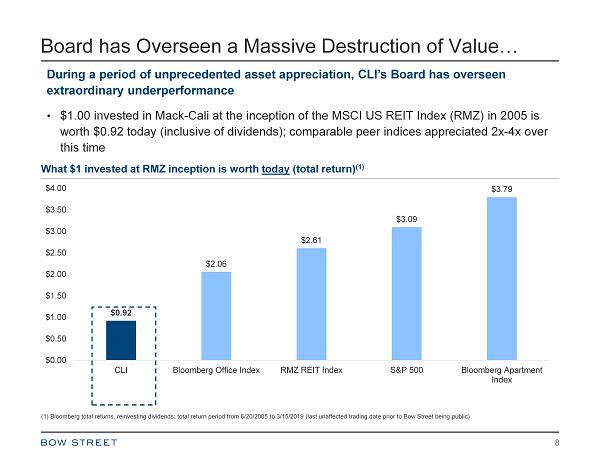

Board has Overseen a Massive Destruction of Value… 8 During a period of unprecedented asset appreciation, CLI’s Board has overseen extraordinary underperformance • $1.00 invested in Mack - Cali at the inception of the MSCI US REIT Index (RMZ) in 2005 is worth $0.92 today (inclusive of dividends); comparable peer indices appreciated 2x - 4x over this time $0.92 $2.06 $2.61 $3.09 $3.79 $0.00 $0.50 $1.00 $1.50 $2.00 $2.50 $3.00 $3.50 $4.00 CLI Bloomberg Office Index RMZ REIT Index S&P 500 Bloomberg Apartment Index What $1 invested at RMZ inception is worth today (total return) (1) (1) Bloomberg total returns, reinvesting dividends; total return period from 6/20/2005 to 3/15/2019 (last unaffected trading dat e prior to Bow Street being public)

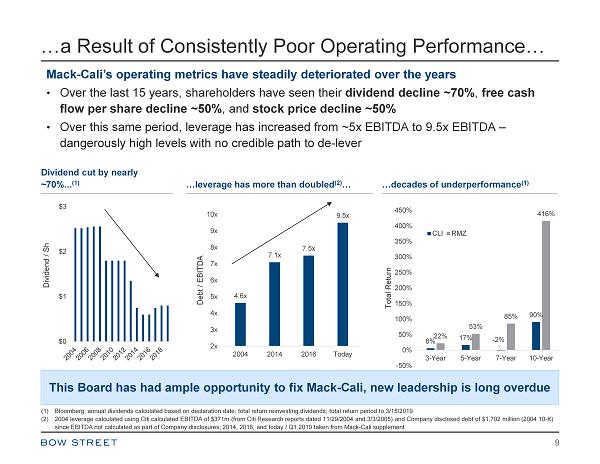

…a Result of Consistently Poor Operating Performance… 9 Mack - Cali’s operating metrics have steadily deteriorated over the years • Over the last 15 years, shareholders have seen their dividend decline ~70% , free cash flow per share decline ~50% , and stock price decline ~50% • Over this same period, leverage has increased from ~5x EBITDA to 9.5x EBITDA – dangerously high levels with no credible path to de - lever …decades of underperformance (1) This Board has had ample opportunity to fix Mack - Cali, new leadership is long overdue $0 $1 $2 $3 Dividend / Sh …leverage has more than doubled (2) … Dividend cut by nearly ~70%... (1) 4.6x 7.1x 7.5x 9.5x 2x 3x 4x 5x 6x 7x 8x 9x 10x 2004 2014 2016 Today Debt / EBITDA 6% 17% - 2% 90% 22% 53% 85% 416% -50% 0% 50% 100% 150% 200% 250% 300% 350% 400% 450% 3-Year 5-Year 7-Year 10-Year Total Return CLI RMZ (1) Bloomberg; annual dividends calculated based on declaration date; total return reinvesting dividends; total return period to 3/1 5/2019 (2) 2004 leverage calculated using Citi calculated EBITDA of $371m (from Citi Research reports dated 11/29/2004 and 3/3/2005) and Co mpany disclosed debt of $1,702 million (2004 10 - K) since EBITDA not calculated as part of Company disclosures; 2014, 2016, and today / Q1 2019 taken from Mack - Cali supplement

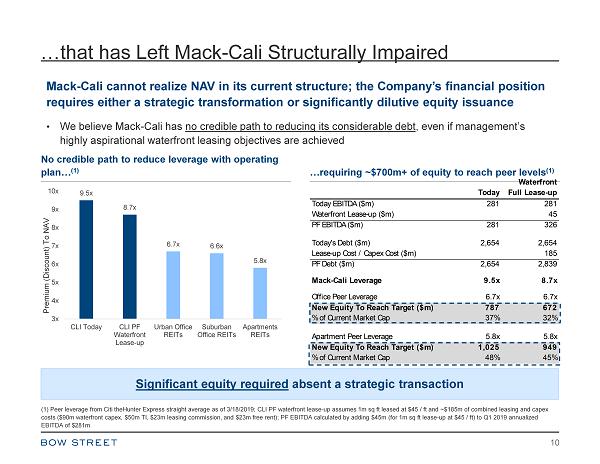

…that has Left Mack - Cali Structurally Impaired 10 Mack - Cali cannot realize NAV in its current structure; the Company’s financial position requires either a strategic transformation or significantly dilutive equity issuance • We believe Mack - Cali has no credible path to reducing its considerable debt , even if management’s highly aspirational waterfront leasing objectives are achieved Significant equity required absent a strategic transaction No credible path to reduce leverage with operating plan… (1) …requiring ~$700m+ of equity to reach peer levels (1) 9.5x 8.7x 6.7x 6.6x 5.8x 3x 4x 5x 6x 7x 8x 9x 10x CLI Today CLI PF Waterfront Lease-up Urban Office REITs Suburban Office REITs Apartments REITs Premium (Discount) To NAV (1) Peer leverage from Citi theHunter Express straight average as of 3/18/2019; CLI PF waterfront lease - up assumes 1m sq ft leased at $45 / ft and ~$185m of combined leasing and capex costs ($90m waterfront capex, $50m TI, $23m leasing commission, and $23m free rent); PF EBITDA calculated by adding $45m (for 1m sq ft lease - up at $45 / ft) to Q1 2019 annualized EBITDA of $281m Today Waterfront Full Lease-up Today EBITDA ($m) 281 281 Waterfront Lease-up ($m) 45 PF EBITDA ($m) 281 326 Today's Debt ($m) 2,654 2,654 Lease-up Cost / Capex Cost ($m) 185 PF Debt ($m) 2,654 2,839 Mack-Cali Leverage 9.5x 8.7x Office Peer Leverage 6.7x 6.7x New Equity To Reach Target ($m) 787 672 % of Current Market Cap 37% 32% Apartment Peer Leverage 5.8x 5.8x New Equity To Reach Target ($m) 1,025 949 % of Current Market Cap 48% 45%

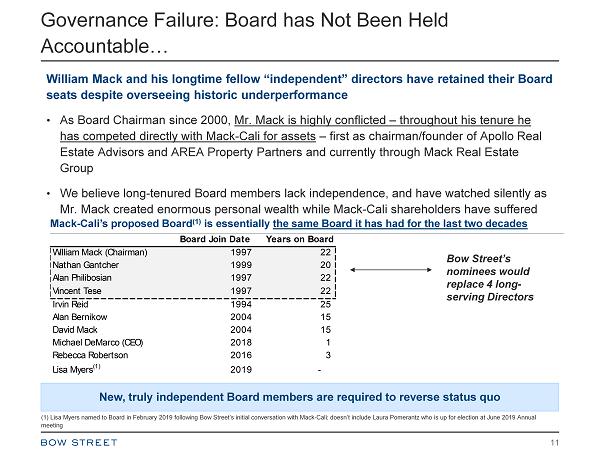

Governance Failure: Board has Not Been Held Accountable… 11 William Mack and his longtime fellow “independent” directors have retained their Board seats despite overseeing historic underperformance • As Board Chairman since 2000, Mr. Mack is highly conflicted – throughout his tenure he has competed directly with Mack - Cali for assets – first as chairman/founder of Apollo Real Estate Advisors and AREA Property Partners and currently through Mack Real Estate Group • We believe long - tenured Board members lack independence, and have watched silently as Mr. Mack created enormous personal wealth while Mack - Cali shareholders have suffered Mack - Cali’s proposed Board (1) is essentially the same Board it has had for the last two decades New, truly independent Board members are required to reverse status quo Bow Street’s nominees would replace 4 long - serving Directors (1) Lisa Myers named to Board in February 2019 following Bow Street’s initial conversation with Mack - Cali; doesn’t include Laura Pomerantz who is up for election at June 2019 Annual meeting Board Join Date Years on Board William Mack (Chairman) 1997 22 Nathan Gantcher 1999 20 Alan Philibosian 1997 22 Vincent Tese 1997 22 Irvin Reid 1994 25 Alan Bernikow 2004 15 David Mack 2004 15 Michael DeMarco (CEO) 2018 1 Rebecca Robertson 2016 3 Lisa Myers (1) 2019 -

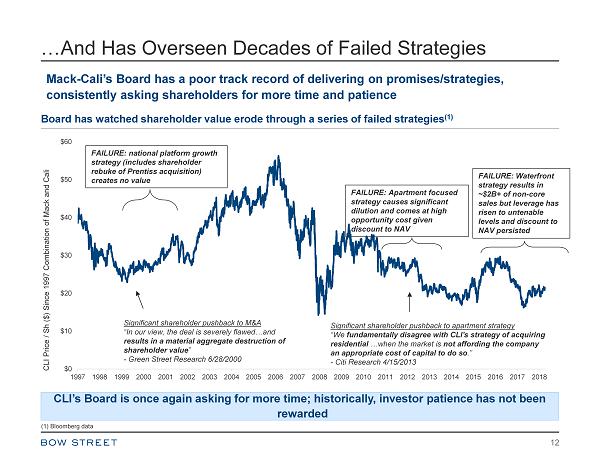

…And Has Overseen Decades of Failed Strategies 12 (1) Bloomberg data $0 $10 $20 $30 $40 $50 $60 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 CLI Price / Sh ($) Since 1997 Combination of Mack and Cali Board has watched shareholder value erode through a series of failed strategies (1) FAILURE: national platform growth strategy (includes shareholder rebuke of Prentiss acquisition) creates no value FAILURE: Apartment focused strategy causes significant dilution and comes at high opportunity cost given discount to NAV FAILURE: Waterfront strategy results in ~$2B+ of non - core sales but leverage has risen to untenable levels and discount to NAV persisted Significant shareholder pushback to apartment strategy “We fundamentally disagree with CLI's strategy of acquiring residential …when the market is not affording the company an appropriate cost of capital to do so .” - Citi Research 4/15/2013 Significant shareholder pushback to M&A “In our view, the deal is severely flawed…and results in a material aggregate destruction of shareholder value ” - Green Street Research 6/28/2000 Mack - Cali’s Board has a poor track record of delivering on promises/strategies, consistently asking shareholders for more time and patience CLI’s Board is once again asking for more time; historically, investor patience has not been rewarded

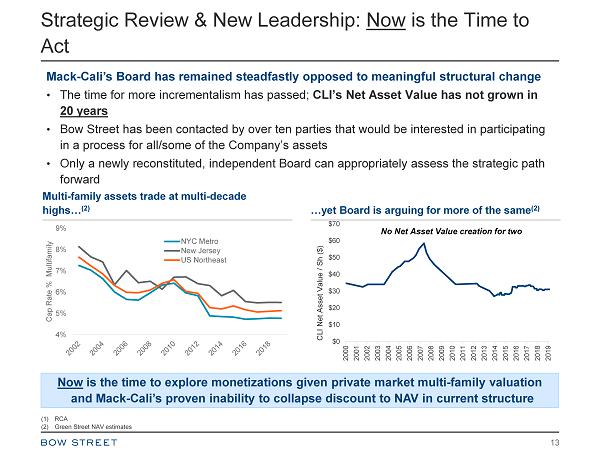

Strategic Review & New Leadership: Now is the Time to Act 13 Mack - Cali’s Board has remained steadfastly opposed to meaningful structural change • The time for more incrementalism has passed; CLI’s Net Asset Value has not grown in 20 years • Bow Street has been contacted by over ten parties that would be interested in participating in a process for all/some of the Company’s assets • Only a newly reconstituted, independent Board can appropriately assess the strategic path forward Now is the time to explore monetizations given private market multi - family valuation and Mack - Cali’s proven inability to collapse discount to NAV in current structure Multi - family assets trade at multi - decade highs… (2) 4% 5% 6% 7% 8% 9% Cap Rate % Multifamily NYC Metro New Jersey US Northeast (1) RCA (2) Green Street NAV estimates $0 $10 $20 $30 $40 $50 $60 $70 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 CLI Net Asset Value / Sh ($) No Net Asset Value creation for two …yet Board is arguing for more of the same (2)

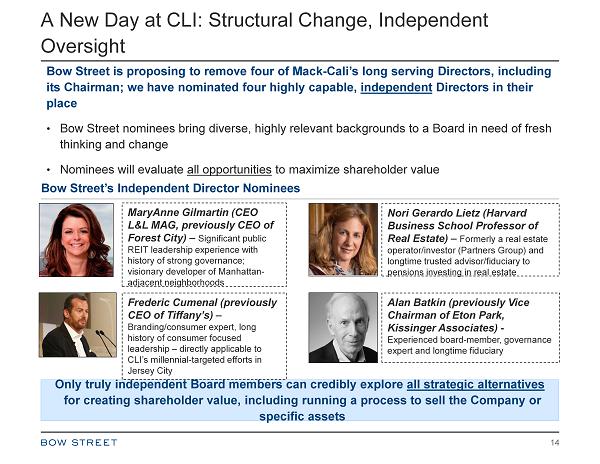

A New Day at CLI: Structural Change, Independent Oversight 14 Bow Street is proposing to remove four of Mack - Cali’s long serving Directors, including its Chairman; we have nominated four highly capable, independent Directors in their place • Bow Street nominees bring diverse, highly relevant backgrounds to a Board in need of fresh thinking and change • Nominees will evaluate all opportunities to maximize shareholder value Bow Street’s Independent Director Nominees Only truly independent Board members can credibly explore all strategic alternatives for creating shareholder value, including running a process to sell the Company or specific assets Alan Batkin (previously Vice Chairman of Eton Park, Kissinger Associates) - Experienced board - member, governance expert and longtime fiduciary MaryAnne Gilmartin (CEO L&L MAG, previously CEO of Forest City) – Significant public REIT leadership experience with history of strong governance; visionary developer of Manhattan - adjacent neighborhoods Nori Gerardo Lietz (Harvard Business School Professor of Real Estate) – Formerly a real estate operator/investor (Partners Group) and longtime trusted advisor/fiduciary to pensions investing in real estate Frederic Cumenal (previously CEO of Tiffany’s) – Branding/consumer expert, long history of consumer focused leadership – directly applicable to CLI’s millennial - targeted efforts in Jersey City

15 15 Years of Underperformance: The Legacy of Mack - Cali’s Current Board

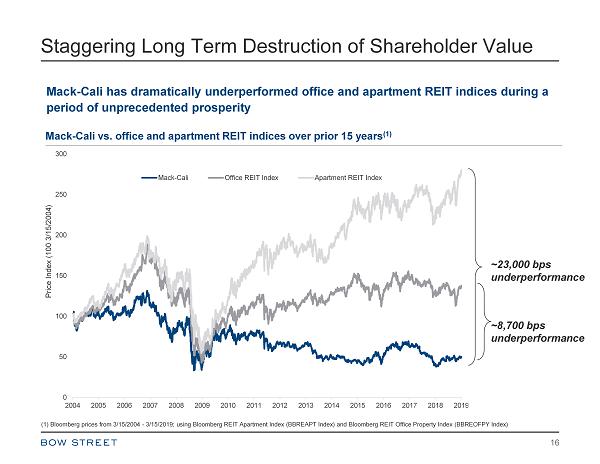

Staggering Long Term Destruction of Shareholder Value 16 Mack - Cali vs. office and apartment REIT indices over prior 15 years (1) 0 50 100 150 200 250 300 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Price Index (100 3/15/2004) Mack-Cali Office REIT Index Apartment REIT Index (1) Bloomberg prices from 3/15/2004 - 3/15/2019; using Bloomberg REIT Apartment Index (BBREAPT Index) and Bloomberg REIT Office Property Index (BBREOFPY Index) Mack - Cali has dramatically underperformed office and apartment REIT indices during a period of unprecedented prosperity ~8,700 bps underperformance ~23,000 bps underperformance

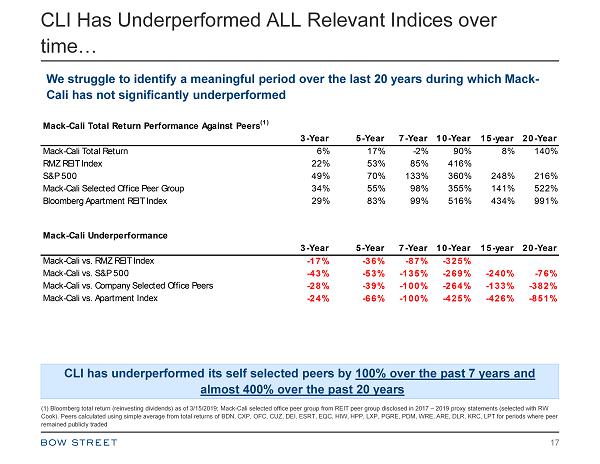

CLI Has Underperformed ALL Relevant Indices over time… 17 We struggle to identify a meaningful period over the last 20 years during which Mack - Cali has not significantly underperformed CLI has underperformed its self selected peers by 100% over the past 7 years and almost 400% over the past 20 years Mack-Cali Total Return Performance Against Peers (1) 3-Year 5-Year 7-Year 10-Year 15-year 20-Year Mack-Cali Total Return 6% 17% -2% 90% 8% 140% RMZ REIT Index 22% 53% 85% 416% S&P 500 49% 70% 133% 360% 248% 216% Mack-Cali Selected Office Peer Group 34% 55% 98% 355% 141% 522% Bloomberg Apartment REIT Index 29% 83% 99% 516% 434% 991% Mack-Cali Underperformance 3-Year 5-Year 7-Year 10-Year 15-year 20-Year Mack-Cali vs. RMZ REIT Index -17% -36% -87% -325% Mack-Cali vs. S&P 500 -43% -53% -135% -269% -240% -76% Mack-Cali vs. Company Selected Office Peers -28% -39% -100% -264% -133% -382% Mack-Cali vs. Apartment Index -24% -66% -100% -425% -426% -851% (1) Bloomberg total return (reinvesting dividends) as of 3/15/2019; Mack - Cali selected office peer group from REIT peer group di sclosed in 2017 – 2019 proxy statements (selected with RW Cook). Peers calculated using simple average from total returns of BDN, CXP, OFC, CUZ, DEI, ESRT, EQC, HIW, HPP, LXP, PGRE, P DM, WRE, ARE, DLR, KRC, LPT for periods where peer remained publicly traded

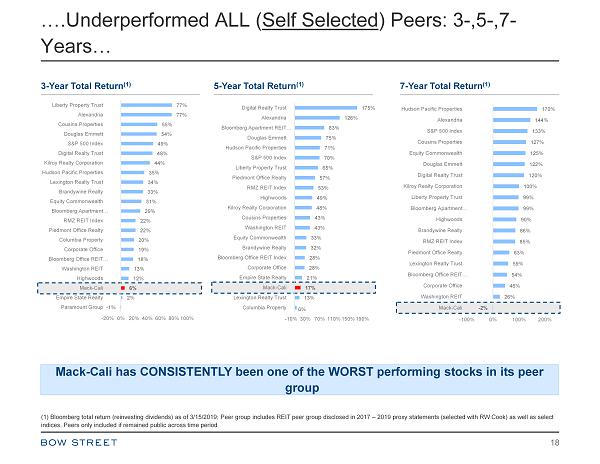

….Underperformed ALL ( Self Selected ) Peers: 3 - ,5 - ,7 - Years… 18 - 1% 2% 6% 12% 13% 18% 19% 20% 22% 22% 29% 31% 33% 34% 35% 44% 48% 49% 54% 55% 77% 77% -20% 0% 20% 40% 60% 80% 100% Paramount Group Empire State Realty Mack-Cali Highwoods Washington REIT Bloomberg Office REIT… Corporate Office Columbia Property Piedmont Office Realty RMZ REIT Index Bloomberg Apartment… Equity Commonwealth Brandywine Realty Lexington Realty Trust Hudson Pacific Properties Kilroy Realty Corporation Digital Realty Trust S&P 500 Index Douglas Emmett Cousins Properties Alexandria Liberty Property Trust 3 - Year Total Return (1) 6% 13% 17% 21% 28% 28% 32% 33% 43% 43% 48% 49% 53% 57% 65% 70% 71% 75% 83% 126% 175% -10% 30% 70% 110% 150% 190% Columbia Property Lexington Realty Trust Mack-Cali Empire State Realty Corporate Office Bloomberg Office REIT Index Brandywine Realty Equity Commonwealth Washington REIT Cousins Properties Kilroy Realty Corporation Highwoods RMZ REIT Index Piedmont Office Realty Liberty Property Trust S&P 500 Index Hudson Pacific Properties Douglas Emmett Bloomberg Apartment REIT… Alexandria Digital Realty Trust 5 - Year Total Return (1) - 2% 26% 46% 54% 59% 63% 85% 86% 90% 99% 99% 100% 120% 122% 125% 127% 133% 144% 170% -100% 0% 100% 200% Mack-Cali Washington REIT Corporate Office Bloomberg Office REIT… Lexington Realty Trust Piedmont Office Realty RMZ REIT Index Brandywine Realty Highwoods Bloomberg Apartment… Liberty Property Trust Kilroy Realty Corporation Digital Realty Trust Douglas Emmett Equity Commonwealth Cousins Properties S&P 500 Index Alexandria Hudson Pacific Properties 7 - Year Total Return (1) (1) Bloomberg total return (reinvesting dividends) as of 3/15/2019; Peer group includes REIT peer group disclosed in 2017 – 2019 proxy statements (selected with RW Cook) as well as select indices. Peers only included if remained public across time period Mack - Cali has CONSISTENTLY been one of the WORST performing stocks in its peer group

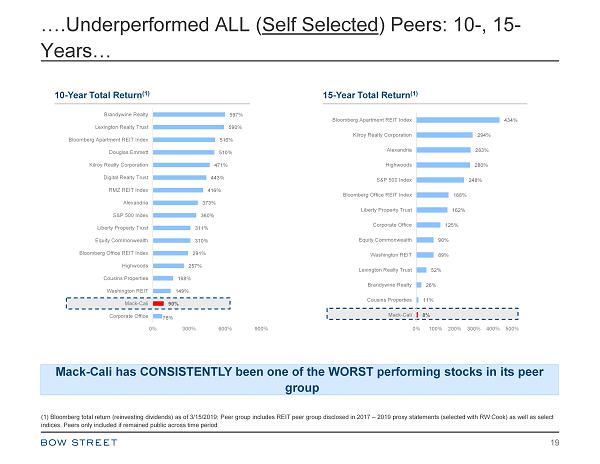

….Underperformed ALL ( Self Selected ) Peers: 10 - , 15 - Years… 19 10 - Year Total Return (1) 8% 11% 26% 52% 89% 90% 125% 162% 168% 248% 280% 283% 294% 434% 0% 100% 200% 300% 400% 500% Mack-Cali Cousins Properties Brandywine Realty Lexington Realty Trust Washington REIT Equity Commonwealth Corporate Office Liberty Property Trust Bloomberg Office REIT Index S&P 500 Index Highwoods Alexandria Kilroy Realty Corporation Bloomberg Apartment REIT Index 15 - Year Total Return (1) 78% 90% 149% 168% 257% 291% 310% 311% 360% 373% 416% 443% 471% 510% 516% 590% 597% 0% 300% 600% 900% Corporate Office Mack-Cali Washington REIT Cousins Properties Highwoods Bloomberg Office REIT Index Equity Commonwealth Liberty Property Trust S&P 500 Index Alexandria RMZ REIT Index Digital Realty Trust Kilroy Realty Corporation Douglas Emmett Bloomberg Apartment REIT Index Lexington Realty Trust Brandywine Realty (1) Bloomberg total return (reinvesting dividends) as of 3/15/2019; Peer group includes REIT peer group disclosed in 2017 – 2019 proxy statements (selected with RW Cook) as well as select indices. Peers only included if remained public across time period Mack - Cali has CONSISTENTLY been one of the WORST performing stocks in its peer group

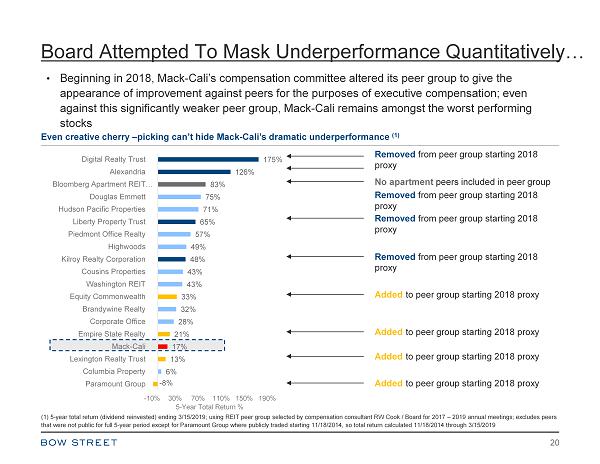

Board Attempted To Mask Underperformance Quantitatively… 20 • Beginning in 2018, Mack - Cali’s compensation committee altered its peer group to give the appearance of improvement against peers for the purposes of executive compensation; even against this significantly weaker peer group, Mack - Cali remains amongst the worst performing stocks Even creative cherry – picking can’t hide Mack - Cali’s dramatic underperformance (1) Removed from peer group starting 2018 proxy Added to peer group starting 2018 proxy No apartment peers included in peer group (1) 5 - year total return (dividend reinvested) ending 3/15/2019; using REIT peer group selected by compensation consultant RW Coo k / Board for 2017 – 2019 annual meetings; excludes peers that were not public for full 5 - year period except for Paramount Group where publicly traded starting 11/18/2014, so total retur n calculated 11/18/2014 through 3/15/2019 Removed from peer group starting 2018 proxy - 8% 6% 13% 17% 21% 28% 32% 33% 43% 43% 48% 49% 57% 65% 71% 75% 83% 126% 175% -10% 30% 70% 110% 150% 190% Paramount Group Columbia Property Lexington Realty Trust Mack-Cali Empire State Realty Corporate Office Brandywine Realty Equity Commonwealth Washington REIT Cousins Properties Kilroy Realty Corporation Highwoods Piedmont Office Realty Liberty Property Trust Hudson Pacific Properties Douglas Emmett Bloomberg Apartment REIT… Alexandria Digital Realty Trust 5 - Year Total Return % Removed from peer group starting 2018 proxy Removed from peer group starting 2018 proxy Added to peer group starting 2018 proxy Added to peer group starting 2018 proxy Added to peer group starting 2018 proxy

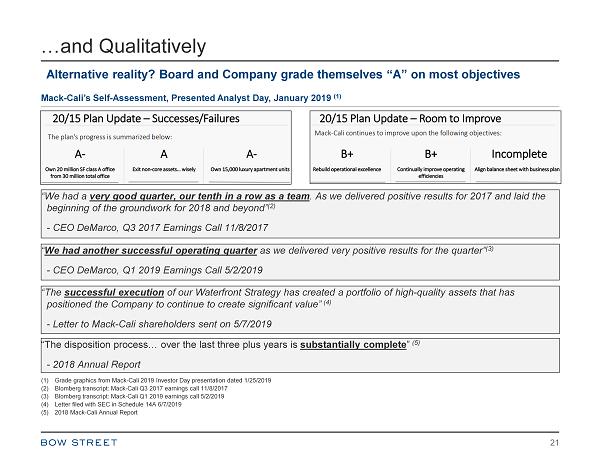

…and Qualitatively 21 Mack - Cali’s Self - Assessment, Presented Analyst Day, January 2019 (1) Alternative reality? Board and Company grade themselves “A” on most objectives “We had a very good quarter, our tenth in a row as a team . As we delivered positive results for 2017 and laid the beginning of the groundwork for 2018 and beyond” (2) - CEO DeMarco, Q3 2017 Earnings Call 11/8/2017 (1) Grade graphics from Mack - Cali 2019 Investor Day presentation dated 1/25/2019 (2) Blomberg transcript: Mack - Cali Q3 2017 earnings call 11/8/2017 (3) Blomberg transcript: Mack - Cali Q1 2019 earnings call 5/2/2019 (4) Letter filed with SEC in Schedule 14A 6/7/2019 (5) 2018 Mack - Cali Annual Report “ We had another successful operating quarter as we delivered very positive results for the quarter” (3) - CEO DeMarco, Q1 2019 Earnings Call 5/2/2019 “The successful execution of our Waterfront Strategy has created a portfolio of high - quality assets that has positioned the Company to continue to create significant value” (4) - Letter to Mack - Cali shareholders sent on 5/7/2019 “The disposition process… over the last three plus years is substantially complete ” (5) - 2018 Annual Report

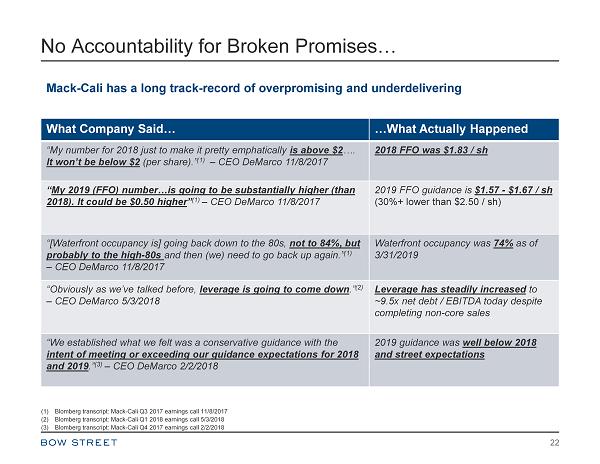

No Accountability for Broken Promises… 22 Mack - Cali has a long track - record of overpromising and underdelivering What Company Said… …What Actually Happened “My number for 2018 just to make it pretty emphatically is above $2 …. It won’t be below $2 (per share) .” (1) – CEO DeMarco 11/8/2017 2018 FFO was $1.83 / sh “ My 2019 (FFO) number…is going to be substantially higher (than 2018). It could be $0.50 higher ” (1) – CEO DeMarco 11/8/2017 2019 FFO guidance is $1.57 - $1.67 / sh (30%+ lower than $2.50 / sh ) “[Waterfront occupancy is] going back down to the 80s, not to 84%, but probably to the high - 80s and then (we) need to go back up again.” (1) – CEO DeMarco 11/8/2017 Waterfront occupancy was 74% as of 3/31/2019 “Obviously as we’ve talked before, leverage is going to come down .” (2) – CEO DeMarco 5/3/2018 Leverage has steadily increased to ~9.5x net debt / EBITDA today despite completing non - core sales “We established what we felt was a conservative guidance with the intent of meeting or exceeding our guidance expectations for 2018 and 2019 .” (3) – CEO DeMarco 2/2/2018 2019 guidance was well below 2018 and street expectations (1) Blomberg transcript: Mack - Cali Q3 2017 earnings call 11/8/2017 (2) Blomberg transcript: Mack - Cali Q1 2018 earnings call 5/3/2018 (3) Blomberg transcript: Mack - Cali Q4 2017 earnings call 2/2/2018

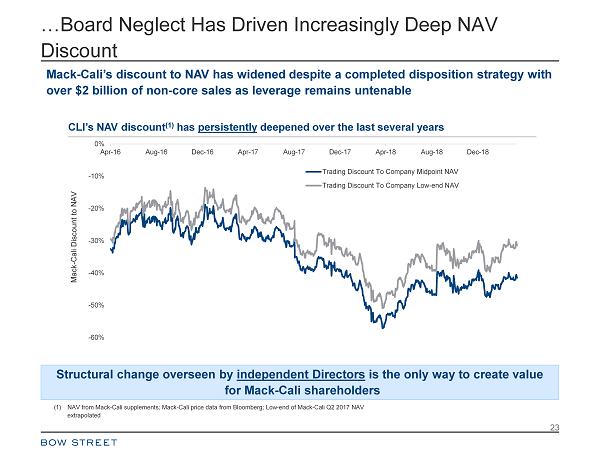

…Board Neglect Has Driven Increasingly Deep NAV Discount 23 CLI’s NAV discount (1) has persistently deepened over the last several years -60% -50% -40% -30% -20% -10% 0% Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17 Apr-18 Aug-18 Dec-18 Mack - Cali Discount to NAV Trading Discount To Company Midpoint NAV Trading Discount To Company Low-end NAV Mack - Cali’s discount to NAV has widened despite a completed disposition strategy with over $2 billion of non - core sales as leverage remains untenable Structural change overseen by independent Directors is the only way to create value for Mack - Cali shareholders (1) NAV from Mack - Cali supplements; Mack - Cali price data from Bloomberg; Low - end of Mack - Cali Q2 2017 NAV extrapolated

24 Governance: Entrenched Board, Myriad Conflicts

25 (1) Green Street Research report 10/17/2005 “CLI’s poor corporate governance… all but ensures the company will not be a target unless Chairman Bill Mack wants it to be” - Analyst Research Note from October 17, 2005 (14 Years Ago) CLI Stock Price: $41.12/share (~100% higher than current levels)

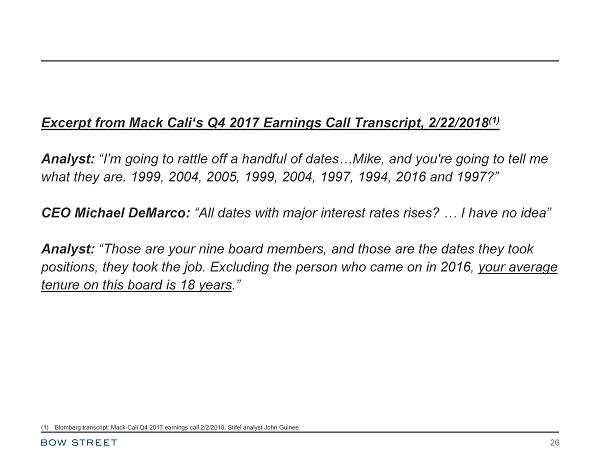

26 Excerpt from Mack Cali‘s Q4 2017 Earnings Call Transcript, 2/22/2018 (1) Analyst: “I’m going to rattle off a handful of dates…Mike, and you're going to tell me what they are. 1999, 2004, 2005, 1999, 2004, 1997, 1994, 2016 and 1997?” CEO Michael DeMarco: “All dates with major interest rates rises? … I have no idea” Analyst: “Those are your nine board members, and those are the dates they took positions, they took the job. Excluding the person who came on in 2016, your average tenure on this board is 18 years .” (1) Blomberg transcript: Mack - Cali Q4 2017 earnings call 2/2/2018; Stifel analyst John Guinee

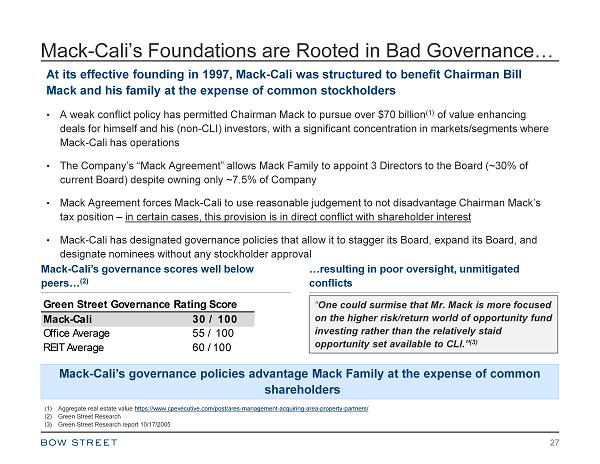

Mack - Cali’s Foundations are Rooted in Bad Governance… 27 At its effective founding in 1997, Mack - Cali was structured to benefit Chairman Bill Mack and his family at the expense of common stockholders • A weak conflict policy has permitted Chairman Mack to pursue over $70 billion (1) of value enhancing deals for himself and his (non - CLI) investors, with a significant concentration in markets/segments where Mack - Cali has operations • The Company’s “Mack Agreement” allows Mack Family to appoint 3 Directors to the Board (~30% of current Board) despite owning only ~7.5% of Company • Mack Agreement forces Mack - Cali to use reasonable judgement to not disadvantage Chairman Mack’s tax position – in certain cases, this provision is in direct conflict with shareholder interest • Mack - Cali has designated governance policies that allow it to stagger its Board, expand its Board, and designate nominees without any stockholder approval Mack - Cali’s governance policies advantage Mack Family at the expense of common shareholders Mack - Cali’s governance scores well below peers… (2) Green Street Governance Rating Score Mack-Cali 30 / 100 Office Average 55 / 100 REIT Average 60 /100 “ One could surmise that Mr. Mack is more focused on the higher risk/return world of opportunity fund investing rather than the relatively staid opportunity set available to CLI.” (3) (1) Aggregate real estate value https://www.cpexecutive.com/post/ares - management - acquiring - area - property - partners/ (2) Green Street Research (3) Green Street Research report 10/17/2005 …resulting in poor oversight, unmitigated conflicts

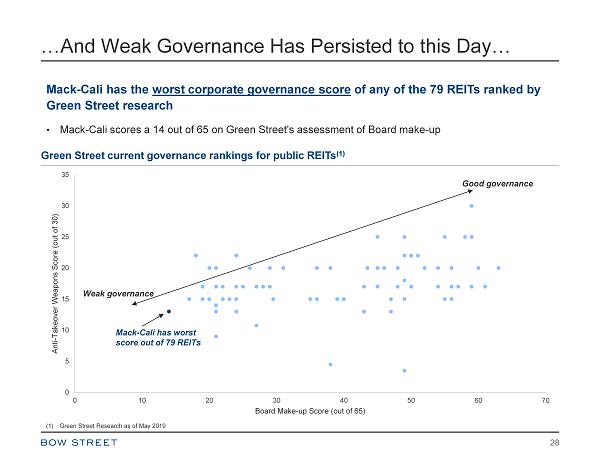

…And Weak Governance Has Persisted to this Day… 28 Mack - Cali has the worst corporate governance score of any of the 79 REITs ranked by Green Street research • Mack - Cali scores a 14 out of 65 on Green Street's assessment of Board make - up Green Street current governance rankings for public REITs (1) (1) Green Street Research as of May 2019 0 5 10 15 20 25 30 35 0 10 20 30 40 50 60 70 Anti - Takeover Weapons Score (out of 30) Board Make - up Score (out of 65) Mack - Cali has worst score out of 79 REITs Weak governance Good governance

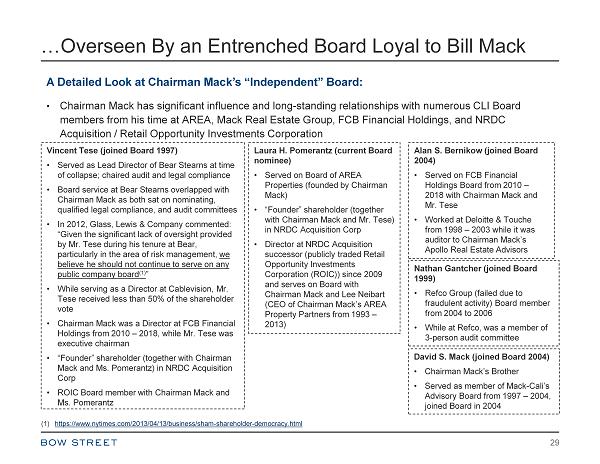

…Overseen By an Entrenched Board Loyal to Bill Mack 29 A Detailed Look at Chairman Mack’s “Independent” Board: • Chairman Mack has significant influence and long - standing relationships with numerous CLI Board members from his time at AREA, Mack Real Estate Group, FCB Financial Holdings, and NRDC Acquisition / Retail Opportunity Investments Corporation David S. Mack (joined Board 2004) • Chairman Mack’s Brother • Served as member of Mack - Cali’s Advisory Board from 1997 – 2004, joined Board in 2004 Vincent Tese (joined Board 1997) • Served as Lead Director of Bear Stearns at time of collapse; chaired audit and legal compliance • Board service at Bear Stearns overlapped with Chairman Mack as both sat on nominating, qualified legal compliance, and audit committees • In 2012, Glass, Lewis & Company commented: “Given the significant lack of oversight provided by Mr. Tese during his tenure at Bear, particularly in the area of risk management, we believe he should not continue to serve on any public company board (1) ” • While serving as a Director at Cablevision, Mr. Tese received less than 50% of the shareholder vote • Chairman Mack was a Director at FCB Financial Holdings from 2010 – 2018, while Mr. Tese was executive chairman • “Founder” shareholder (together with Chairman Mack and Ms. Pomerantz) in NRDC Acquisition Corp • ROIC Board member with Chairman Mack and Ms. Pomerantz Alan S. Bernikow (joined Board 2004) • Served on FCB Financial Holdings Board from 2010 – 2018 with Chairman Mack and Mr. Tese • Worked at Deloitte & Touche from 1998 – 2003 while it was auditor to Chairman Mack’s Apollo Real Estate Advisors Laura H. Pomerantz (current Board nominee) • Served on Board of AREA Properties (founded by Chairman Mack) • “Founder” shareholder (together with Chairman Mack and Mr. Tese ) in NRDC Acquisition Corp • Director at NRDC Acquisition successor (publicly traded Retail Opportunity Investments Corporation (ROIC)) since 2009 and serves on Board with Chairman Mack and Lee Neibart (CEO of Chairman Mack’s AREA Property Partners from 1993 – 2013) (1) https://www.nytimes.com/2013/04/13/business/sham - shareholder - democracy.html Nathan Gantcher (joined Board 1999) • Refco Group (failed due to fraudulent activity) Board member from 2004 to 2006 • While at Refco , was a member of 3 - person audit committee

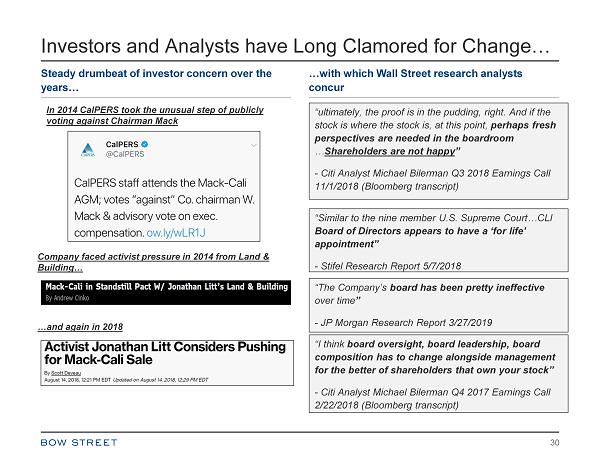

Investors and Analysts have Long Clamored for Change… 30 …with which Wall Street research analysts concur Steady drumbeat of investor concern over the years… “ultimately, the proof is in the pudding, right. And if the stock is where the stock is, at this point, perhaps fresh perspectives are needed in the boardroom … Shareholders are not happy ” - Citi Analyst Michael Bilerman Q3 2018 Earnings Call 11/1/2018 (Bloomberg transcript) “Similar to the nine member U.S. Supreme Court…CLI Board of Directors appears to have a ‘for life’ appointment” - Stifel Research Report 5/7/2018 “The Company’s board has been pretty ineffective over time ” - JP Morgan Research Report 3/27/2019 “I think board oversight, board leadership, board composition has to change alongside management for the better of shareholders that own your stock” - Citi Analyst Michael Bilerman Q4 2017 Earnings Call 2/22/2018 (Bloomberg transcript) In 2014 CalPERS took the unusual step of publicly voting against Chairman Mack Company faced activist pressure in 2014 from Land & Building… …and again in 2018

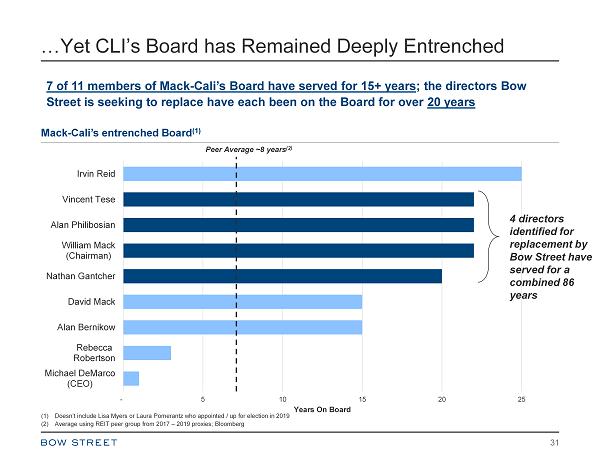

…Yet CLI’s Board has Remained Deeply Entrenched 31 - 5 10 15 20 25 Michael DeMarco (CEO) Rebecca Robertson Alan Bernikow David Mack Nathan Gantcher William Mack (Chairman) Alan Philibosian Vincent Tese Irvin Reid Years On Board 4 directors identified for replacement by Bow Street have served for a combined 86 years Mack - Cali’s entrenched Board (1) 7 of 11 members of Mack - Cali’s Board have served for 15+ years ; the directors Bow Street is seeking to replace have each been on the Board for over 20 years Peer Average ~8 years (2) (1) Doesn’t include Lisa Myers or Laura Pomerantz who appointed / up for election in 2019 (2) Average using REIT peer group from 2017 – 2019 proxies; Bloomberg

Status Quo Has Been Preserved by Weak Governance… 32 • Stockholders can’t act outside of annual meeting - Unanimous written consent is required to act in lieu of a stockholder meeting, thus severely limiting shareholders’ ability to effect change • Bar for director removal is unusually high, driving lack of accountability - directors of the Company may only be removed for cause - campaign against directors outside of the annual meeting practically impossible • Board has retained rights to act unilaterally, protecting itself from “uncooperative” shareholders • Mack - Cali has not opted out of the Maryland Unsolicited Takeover Act (" MUTA "), essentially allowing the Board to classify itself without shareholder approval • Per the Company’s articles of restatement, the Company has opted into MGCL § 3 - 804(c), giving the Board sole and exclusive power to fill director vacancies (including those created by expanding the size of the Board) • Perhaps most importantly: the Board has the sole and exclusive power to increase the size of the Board – this means that even if new board members are elected by shareholders, the Board can unilaterally act to dilute the stockholders’ presence in the boardroom at any time The Mack Family and the Board have been protected by Mack - Cali’s shareholder - unfriendly governance Weak governance at Mack - Cali has impeded urgently needed change over the years

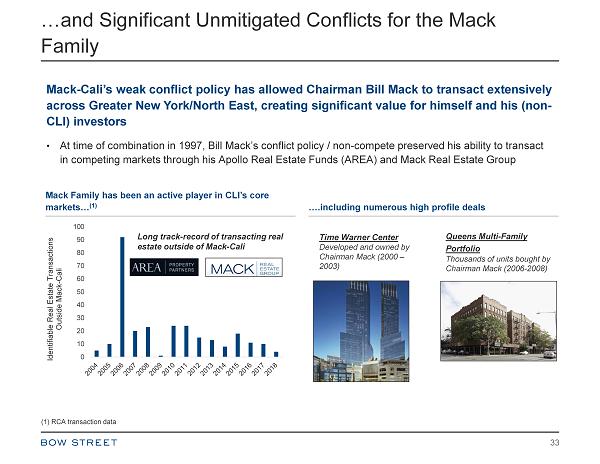

…and Significant Unmitigated Conflicts for the Mack Family 33 Mack - Cali’s weak conflict policy has allowed Chairman Bill Mack to transact extensively across Greater New York/North East, creating significant value for himself and his (non - CLI) investors • At time of combination in 1997, Bill Mack’s conflict policy / non - compete preserved his ability to transact in competing markets through his Apollo Real Estate Funds (AREA) and Mack Real Estate Group Mack Family has been an active player in CLI’s core markets… (1) 0 10 20 30 40 50 60 70 80 90 100 Identifiable Real Estate Transactions Outside Mack - Cali Time Warner Center Developed and owned by Chairman Mack (2000 – 2003) Queens Multi - Family Portfolio Thousands of units bought by Chairman Mack (2006 - 2008) Long track - record of transacting real estate outside of Mack - Cali (1) RCA transaction data ….including numerous high profile deals

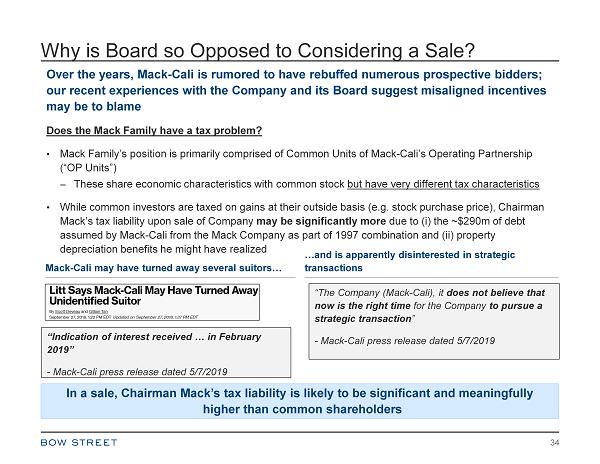

Why is Board so Opposed to Considering a Sale ? 34 In a sale, Chairman Mack’s tax liability is likely to be significant and meaningfully higher than common shareholders Over the years, Mack - Cali is rumored to have rebuffed numerous prospective bidders; our recent experiences with the Company and its Board suggest misaligned incentives may be to blame Does the Mack Family have a tax problem? • Mack Family’s position is primarily comprised of Common Units of Mack - Cali’s Operating Partnership (“OP Units”) – These share economic characteristics with common stock but have very different tax characteristics • While common investors are taxed on gains at their outside basis (e.g. stock purchase price), Chairman Mack’s tax liability upon sale of Company may be significantly more due to ( i ) the ~$290m of debt assumed by Mack - Cali from the Mack Company as part of 1997 combination and (ii) property depreciation benefits he might have realized “Indication of interest received … in February 2019” - Mack - Cali press release dated 5/7/2019 Mack - Cali may have turned away several suitors… …and is apparently disinterested in strategic transactions “The Company (Mack - Cali), it does not believe that now is the right time for the Company to pursue a strategic transaction ” - Mack - Cali press release dated 5/7/2019

Situation Today: Trapped In Current Structure (Hope is Not a Strategy) 35

36 “Anyone who thinks that I could have just sold assets to pay down debt doesn't realize when you sell at 7 caps or 6.5 caps and you pay down debt, you don't actually work down your net debt - to - EBITDA. The only way you can do that is by selling either land or selling Roseland or raising equity , which are the three options we have in front of us” - Michael DeMarco, CEO of Mack - Cali – November 8 th , 2017 (1) (1) Blomberg transcript: Mack - Cali Q3 2017 earnings call 11/8/2017

Absent Structural Change, CLI’s Value Will Continue To Erode 37 Mack - Cali is trapped in its current structure ; absent immediate change we believe value erosion will persist • Mack - Cali’s disparate assets do not belong together, resulting in lowest common denominator valuation – Bundling development rich multifamily assets and high - vacancy, highly indebted office assets has left CLI trading at a significant discount to NAV in public markets; Mack - Cali’s portfolio must be split - up or sold to realize value • Mack - Cali is significantly over - levered, with no credible path to reduce debt – At over 9x Debt / EBITDA , CLI’s leverage exceeds that of almost all its peers. Despite perpetual management promises of debt reduction, we believe there is no credible path to reducing leverage absent significant shareholder dilution • Mack - Cali is cash - flow constrained: dividend at risk, commercial portfolio is capital starved – Mack - Cali does not cover its dividend from current cash flows; significant incremental capital expenditures/TI/leasing commissions required to improve CLI’s struggling office portfolio • Mack - Cali has been forced to cede value in its best business to third - parties – Capital required for high growth, high value multi - family business has historically been sourced via expensive, dilutive joint - ventures with partners such as Rockpoint Group. Currently, Mack - Cali is planning to continue this strategy, further diluting shareholders and increasing third party ownership of its multi - family business, effectively creating obstacles to a sale of the Company Robust independent Board oversight required to ensure structural change occurs

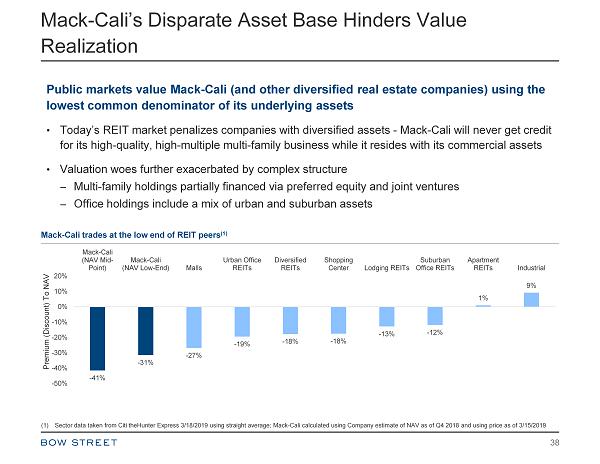

Mack - Cali’s Disparate Asset Base Hinders Value Realization 38 Public markets value Mack - Cali (and other diversified real estate companies) using the lowest common denominator of its underlying assets • Today’s REIT market penalizes companies with diversified assets - Mack - Cali will never get credit for its high - quality, high - multiple multi - family business while it resides with its commercial assets • Valuation woes further exacerbated by complex structure – Multi - family holdings partially financed via preferred equity and joint ventures – Office holdings include a mix of urban and suburban assets - 41% - 31% - 27% - 19% - 18% - 18% - 13% - 12% 1% 9% -50% -40% -30% -20% -10% 0% 10% 20% Mack-Cali (NAV Mid- Point) Mack-Cali (NAV Low-End) Malls Urban Office REITs Diversified REITs Shopping Center Lodging REITs Suburban Office REITs Apartment REITs Industrial Premium (Discount) To NAV Mack - Cali trades at the low end of REIT peers (1) (1) Sector data taken from Citi theHunter Express 3/18/2019 using straight average; Mack - Cali calculated using Company estimate of NAV as of Q4 2018 and using price as o f 3/15/2019

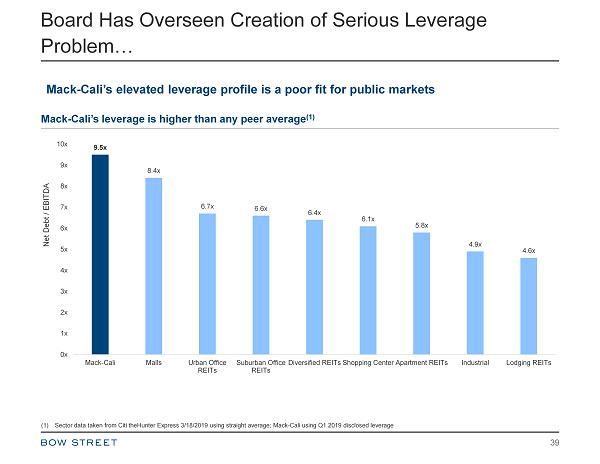

Board Has Overseen Creation of Serious Leverage Problem… 39 Mack - Cali’s elevated leverage profile is a poor fit for public markets Mack - Cali’s leverage is higher than any peer average (1) 9.5x 8.4x 6.7x 6.6x 6.4x 6.1x 5.8x 4.9x 4.6x 0x 1x 2x 3x 4x 5x 6x 7x 8x 9x 10x Mack-Cali Malls Urban Office REITs Suburban Office REITs Diversified REITs Shopping Center Apartment REITs Industrial Lodging REITs Net Debt / EBITDA (1) Sector data taken from Citi theHunter Express 3/18/2019 using straight average; Mack - Cali using Q1 2019 disclosed leverage

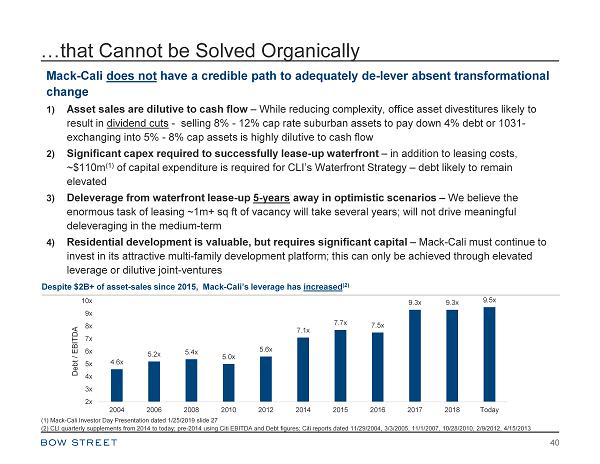

…that Cannot be Solved Organically 40 Mack - Cali does not have a credible path to adequately de - lever absent transformational change 1) Asset sales are dilutive to cash flow – While reducing complexity, office asset divestitures likely to result in dividend cuts - selling 8% - 12% cap rate suburban assets to pay down 4% debt or 1031 - exchanging into 5% - 8% cap assets is highly dilutive to cash flow 2) Significant capex required to successfully lease - up waterfront – in addition to leasing costs, ~$110m (1) of capital expenditure is required for CLI’s Waterfront Strategy – debt likely to remain elevated 3) Deleverage from waterfront lease - up 5 - years away in optimistic scenarios – We believe the enormous task of leasing ~1m+ sq ft of vacancy will take several years; will not drive meaningful deleveraging in the medium - term 4) Residential development is valuable, but requires significant capital – Mack - Cali must continue to invest in its attractive multi - family development platform; this can only be achieved through elevated leverage or dilutive joint - ventures Despite $2B+ of asset - sales since 2015, Mack - Cali’s leverage has increased (2) (1) Mack - Cali Investor Day Presentation dated 1/25/2019 slide 27 (2) CLI quarterly supplements from 2014 to today; pre - 2014 using Citi EBITDA and Debt figures; Citi reports dated 11/29/2004, 3/ 3/2005, 11/1/2007, 10/28/2010, 2/9/2012, 4/15/2013 4.6x 5.2x 5.4x 5.0x 5.6x 7.1x 7.7x 7.5x 9.3x 9.3x 9.5x 2x 3x 4x 5x 6x 7x 8x 9x 10x 2004 2006 2008 2010 2012 2014 2015 2016 2017 2018 Today Debt / EBITDA

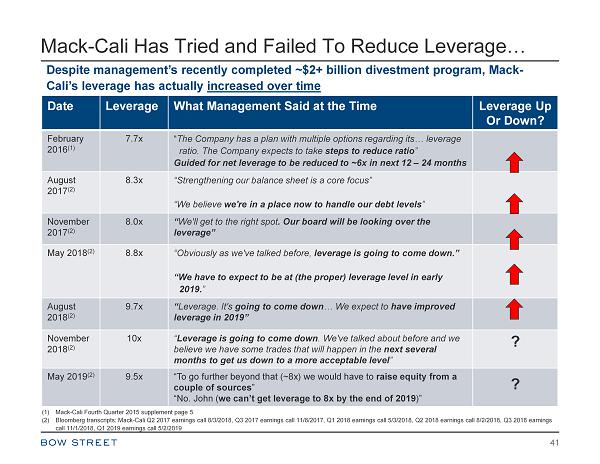

Mack - Cali Has Tried and Failed To Reduce Leverage… 41 Despite management’s recently completed ~$2+ billion divestment program, Mack - Cali’s leverage has actually increased over time Date Leverage What Management Said at the Time Leverage Up Or Down? February 2016 (1) 7.7x “ The Company has a plan with multiple options regarding its… leverage ratio. The Company expects to take steps to reduce ratio ” Guided for net leverage to be reduced to ~6x in next 12 – 24 months August 2017 (2) 8.3x “Strengthening our balance sheet is a core focus” “We believe we're in a place now to handle our debt levels ” November 2017 (2) 8.0x “ We'll get to the right spot . Our board will be looking over the leverage” May 2018 (2) 8.8x “Obviously as we've talked before, leverage is going to come down.” “We have to expect to be at (the proper) leverage level in early 2019. ” August 2018 (2) 9.7x “ Leverage. It's going to come down … We expect to have improved leverage in 2019” November 2018 (2) 10x “ Leverage is going to come down . We've talked about before and we believe we have some trades that will happen in the next several months to get us down to a more acceptable level ” May 2019 (2) 9.5x “To go further beyond that (~8x) we would have to raise equity from a couple of sources ” “No. John ( we can’t get leverage to 8x by the end of 2019 )” ? ? (1) Mack - Cali Fourth Quarter 2015 supplement page 5 (2) Bloomberg transcripts: Mack - Cali Q2 2017 earnings call 8/3/2018, Q3 2017 earnings call 11/8/2017, Q1 2018 earnings call 5/3/2018 , Q2 2018 earnings call 8/2/2018, Q3 2018 earnings call 11/1/2018, Q1 2019 earnings call 5/2/2019

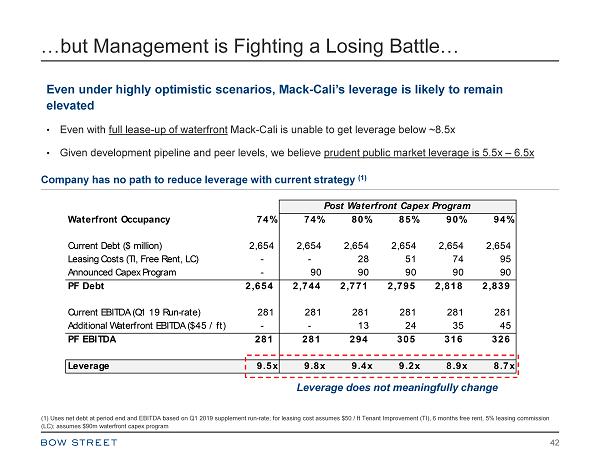

…but Management is Fighting a Losing Battle… 42 Even under highly optimistic scenarios, Mack - Cali’s leverage is likely to remain elevated • Even with full lease - up of waterfront Mack - Cali is unable to get leverage below ~8.5x • Given development pipeline and peer levels, we believe prudent public market leverage is 5.5x – 6.5x (1) Uses net debt at period end and EBITDA based on Q1 2019 supplement run - rate; for leasing cost assumes $50 / ft Tenant Improv ement (TI), 6 months free rent, 5% leasing commission (LC); assumes $90m waterfront capex program Waterfront Occupancy 74% 74% 80% 85% 90% 94% Current Debt ($ million) 2,654 2,654 2,654 2,654 2,654 2,654 Leasing Costs (TI, Free Rent, LC) - - 28 51 74 95 Announced Capex Program - 90 90 90 90 90 PF Debt 2,654 2,744 2,771 2,795 2,818 2,839 Current EBITDA (Q1 19 Run-rate) 281 281 281 281 281 281 Additional Waterfront EBITDA ($45 / ft) - - 13 24 35 45 PF EBITDA 281 281 294 305 316 326 Leverage 9.5x 9.8x 9.4x 9.2x 8.9x 8.7x Post Waterfront Capex Program Company has no path to reduce leverage with current strategy (1) Leverage does not meaningfully change

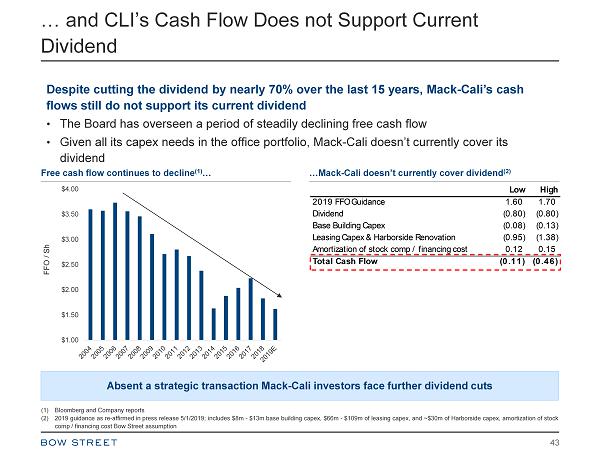

$1.00 $1.50 $2.00 $2.50 $3.00 $3.50 $4.00 FFO / Sh … and CLI’s Cash Flow Does not Support Current Dividend 43 Despite cutting the dividend by nearly 70% over the last 15 years, Mack - Cali’s cash flows still do not support its current dividend • The Board has overseen a period of steadily declining free cash flow • Given all its capex needs in the office portfolio, Mack - Cali doesn’t currently cover its dividend …Mack - Cali doesn’t currently cover dividend (2) Free cash flow continues to decline (1) … Low High 2019 FFO Guidance 1.60 1.70 Dividend (0.80) (0.80) Base Building Capex (0.08) (0.13) Leasing Capex & Harborside Renovation (0.95) (1.38) Amortization of stock comp / financing cost 0.12 0.15 Total Cash Flow (0.11) (0.46) Absent a strategic transaction Mack - Cali investors face further dividend cuts (1) Bloomberg and Company reports (2) 2019 guidance as re - affirmed in press release 5/1/2019; includes $8m - $13m base building capex, $66m - $109m of leasing capex, and ~$30m of Harborside capex, amortization of stock comp / financing cost Bow Street assumption

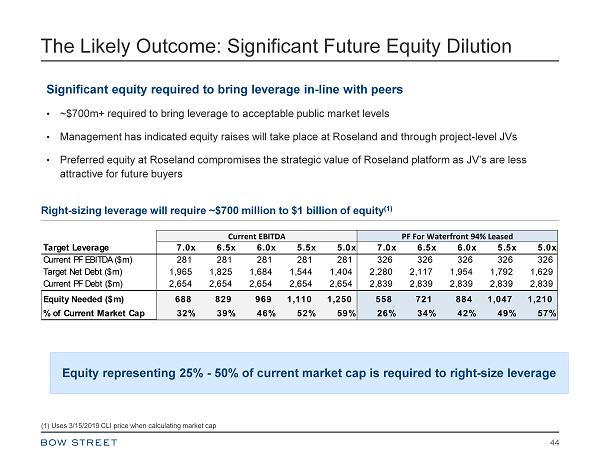

The Likely Outcome: Significant Future Equity Dilution 44 Significant equity required to bring leverage in - line with peers • ~$700m+ required to bring leverage to acceptable public market levels • Management has indicated equity raises will take place at Roseland and through project - level JVs • Preferred equity at Roseland compromises the strategic value of Roseland platform as JV’s are less attractive for future buyers Right - sizing leverage will require ~$700 million to $1 billion of equity (1) Equity representing 25% - 50% of current market cap is required to right - size leverage (1) Uses 3/15/2019 CLI price when calculating market cap Target Leverage 7.0x 6.5x 6.0x 5.5x 5.0x 7.0x 6.5x 6.0x 5.5x 5.0x Current PF EBITDA ($m) 281 281 281 281 281 326 326 326 326 326 Target Net Debt ($m) 1,965 1,825 1,684 1,544 1,404 2,280 2,117 1,954 1,792 1,629 Current PF Debt ($m) 2,654 2,654 2,654 2,654 2,654 2,839 2,839 2,839 2,839 2,839 Equity Needed ($m) 688 829 969 1,110 1,250 558 721 884 1,047 1,210 % of Current Market Cap 32% 39% 46% 52% 59% 26% 34% 42% 49% 57% Current EBITDA PF For Waterfront 94% Leased

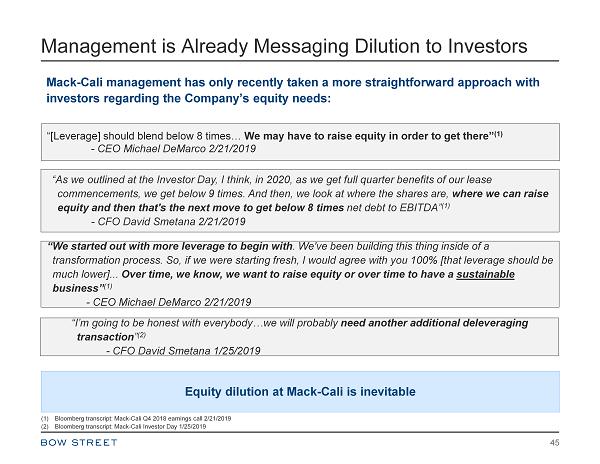

Management is Already Messaging Dilution to Investors 45 Mack - Cali management has only recently taken a more straightforward approach with investors regarding the Company’s equity needs: “[Leverage] should blend below 8 times… We may have to raise equity in order to get there” (1) - CEO Michael DeMarco 2/21/2019 “As we outlined at the Investor Day, I think, in 2020, as we get full quarter benefits of our lease commencements, we get below 9 times. And then, we look at where the shares are, where we can raise equity and then that's the next move to get below 8 times net debt to EBITDA” (1) - CFO David Smetana 2/21/2019 “We started out with more leverage to begin with . We've been building this thing inside of a transformation process. So, if we were starting fresh, I would agree with you 100% [that leverage should be much lower]... Over time, we know, we want to raise equity or over time to have a sustainable business” (1) - CEO Michael DeMarco 2/21/2019 Equity dilution at Mack - Cali is inevitable (1) Bloomberg transcript: Mack - Cali Q4 2018 earnings call 2/21/2019 (2) Bloomberg transcript: Mack - Cali Investor Day 1/25/2019 “I’m going to be honest with everybody…we will probably need another additional deleveraging transaction ” (2) - CFO David Smetana 1/25/2019

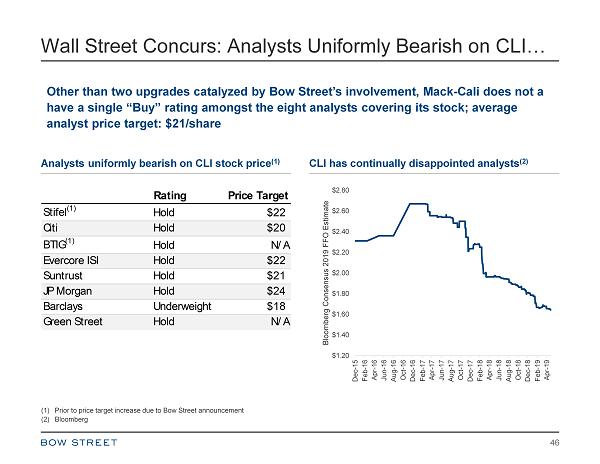

Wall Street Concurs: Analysts Uniformly Bearish on CLI… 46 Other than two upgrades catalyzed by Bow Street’s involvement, Mack - Cali does not a have a single “Buy” rating amongst the eight analysts covering its stock; average analyst price target: $21/share (1) Prior to price target increase due to Bow Street announcement (2) Bloomberg $1.20 $1.40 $1.60 $1.80 $2.00 $2.20 $2.40 $2.60 $2.80 Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16 Feb-17 Apr-17 Jun-17 Aug-17 Oct-17 Dec-17 Feb-18 Apr-18 Jun-18 Aug-18 Oct-18 Dec-18 Feb-19 Apr-19 Bloomberg Consensus 2019 FFO Estimate Analysts uniformly bearish on CLI stock price (1) CLI has continually disappointed analysts (2) Rating Price Target Stifel (1) Hold $22 Citi Hold $20 BTIG (1) Hold N/A Evercore ISI Hold $22 Suntrust Hold $21 JP Morgan Hold $24 Barclays Underweight $18 Green Street Hold N/A

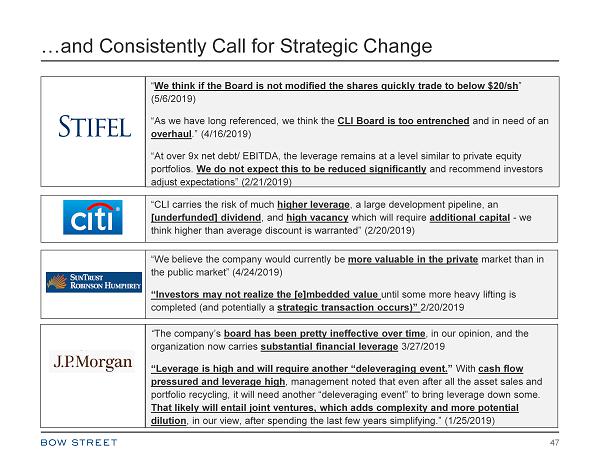

…and Consistently Call for Strategic Change 47 “ We think if the Board is not modified the shares quickly trade to below $20/ sh ” (5/6/2019) “As we have long referenced, we think the CLI Board is too entrenched and in need of an overhaul .” (4/16/2019) “At over 9x net debt/ EBITDA, the leverage remains at a level similar to private equity portfolios. We do not expect this to be reduced significantly and recommend investors adjust expectations” (2/21/2019) “CLI carries the risk of much higher leverage , a large development pipeline, an [underfunded] dividend , and high vacancy which will require additional capital - we think higher than average discount is warranted” (2/20/2019) “We believe the company would currently be more valuable in the private market than in the public market” (4/24/2019) “Investors may not realize the [e] mbedded value until some more heavy lifting is completed (and potentially a strategic transaction occurs)” 2/20/2019 “ The company’s board has been pretty ineffective over time , in our opinion, and the organization now carries substantial financial leverage 3/27/2019 “Leverage is high and will require another “deleveraging event. ” With cash flow pressured and leverage high , management noted that even after all the asset sales and portfolio recycling, it will need another “deleveraging event” to bring leverage down some. That likely will entail joint ventures, which adds complexity and more potential dilution , in our view, after spending the last few years simplifying.” (1/25/2019)

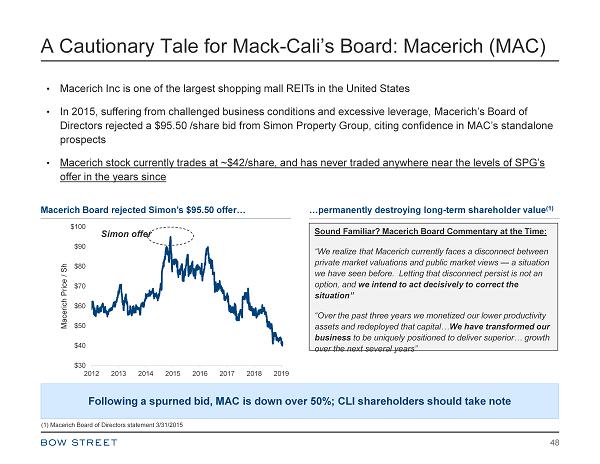

A Cautionary Tale for Mack - Cali’s Board: Macerich (MAC) 48 • Macerich Inc is one of the largest shopping mall REITs in the United States • In 2015, suffering from challenged business conditions and excessive leverage, Macerich’s Board of Directors rejected a $95.50 /share bid from Simon Property Group, citing confidence in MAC’s standalone prospects • Macerich stock currently trades at ~$42/share, and has never traded anywhere near the levels of SPG’s offer in the years since $30 $40 $50 $60 $70 $80 $90 $100 2012 2013 2014 2015 2016 2017 2018 2019 Macerich Price / Sh Macerich Board rejected Simon’s $95.50 offer… Simon offer Following a spurned bid, MAC is down over 50%; CLI shareholders should take note …permanently destroying long - term shareholder value (1) Sound Familiar? Macerich Board Commentary at the Time: “We realize that Macerich currently faces a disconnect between private market valuations and public market views — a situation we have seen before. Letting that disconnect persist is not an option, and we intend to act decisively to correct the situation” “Over the past three years we monetized our lower productivity assets and redeployed that capital… We have transformed our business to be uniquely positioned to deliver superior… growth over the next several years” (1) Macerich Board of Directors statement 3/31/2015

Six Fallacies: the Board’s Side of the Story 49

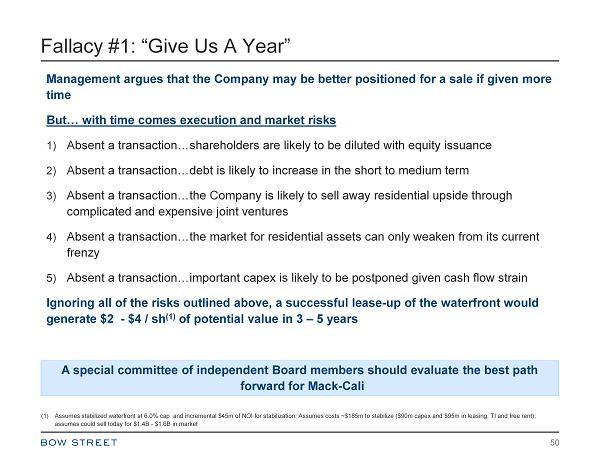

Fallacy #1: “Give Us A Year” 50 Management argues that the Company may be better positioned for a sale if given more time But… with time comes execution and market risks 1) Absent a transaction…shareholders are likely to be diluted with equity issuance 2) Absent a transaction…debt is likely to increase in the short to medium term 3) Absent a transaction…the Company is likely to sell away residential upside through complicated and expensive joint ventures 4) Absent a transaction…the market for residential assets can only weaken from its current frenzy 5) Absent a transaction…important capex is likely to be postponed given cash flow strain Ignoring all of the risks outlined above, a successful lease - up of the waterfront would generate $2 - $4 / sh (1) of potential value in 3 – 5 years A special committee of independent Board members should evaluate the best path forward for Mack - Cali (1) Assumes stabilized waterfront at 6.0% cap and incremental $45m of NOI for stabilization; Assumes costs ~$185m to stabilize ( $90 m capex and $95m in leasing, TI and free rent); assumes could sell today for $1.4B - $1.6B in market

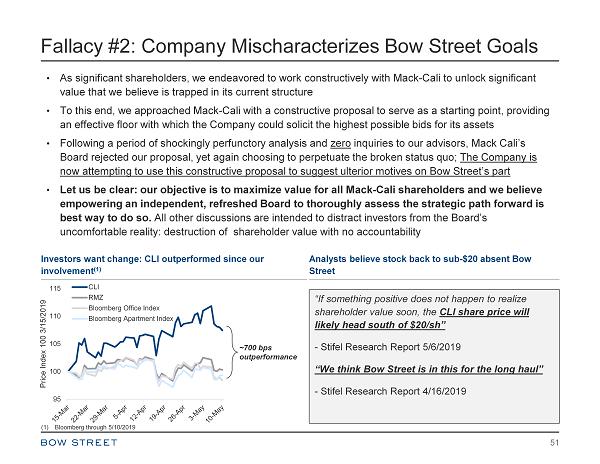

Fallacy #2: Company Mischaracterizes Bow Street Goals 51 • As significant shareholders, we endeavored to work constructively with Mack - Cali to unlock significant value that we believe is trapped in its current structure • To this end, we approached Mack - Cali with a constructive proposal to serve as a starting point, providing an effective floor with which the Company could solicit the highest possible bids for its assets • Following a period of shockingly perfunctory analysis and zero inquiries to our advisors, Mack Cali’s Board rejected our proposal, yet again choosing to perpetuate the broken status quo; The Company is now attempting to use this constructive proposal to suggest ulterior motives on Bow Street’s part • Let us be clear: our objective is to maximize value for all Mack - Cali shareholders and we believe empowering an independent, refreshed Board to thoroughly assess the strategic path forward is best way to do so. All other discussions are intended to distract investors from the Board’s uncomfortable reality: destruction of shareholder value with no accountability Analysts believe stock back to sub - $20 absent Bow Street Investors want change: CLI outperformed since our involvement (1) 95 100 105 110 115 Price Index 100 3/15/2019 CLI RMZ Bloomberg Office Index Bloomberg Apartment Index ~700 bps outperformance “If something positive does not happen to realize shareholder value soon, the CLI share price will likely head south of $20/ sh ” - Stifel Research Report 5/6/2019 “We think Bow Street is in this for the long haul” - Stifel Research Report 4/16/2019 (1) Bloomberg through 5/10/2019

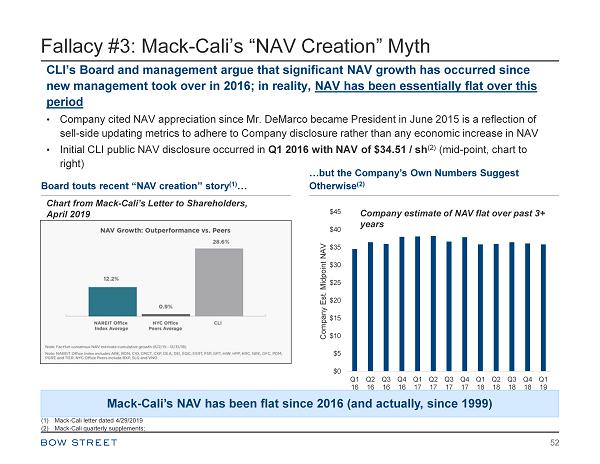

Fallacy #3: Mack - Cali’s “NAV Creation” Myth 52 CLI’s Board and management argue that significant NAV growth has occurred since new management took over in 2016; in reality, NAV has been essentially flat over this period • Company cited NAV appreciation since Mr. DeMarco became President in June 2015 is a reflection of sell - side updating metrics to adhere to Company disclosure rather than any economic increase in NAV • Initial CLI public NAV disclosure occurred in Q1 2016 with NAV of $34.51 / sh (2) (mid - point, chart to right) Board touts recent “NAV creation” story (1) … …but the Company’s Own Numbers Suggest Otherwise (2) $0 $5 $10 $15 $20 $25 $30 $35 $40 $45 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Company Est. Midpoint NAV Company estimate of NAV flat over past 3+ years Chart from Mack - Cali’s Letter to Shareholders, April 2019 Mack - Cali’s NAV has been flat since 2016 (and actually, since 1999) (1) Mack - Cali letter dated 4/29/2019 (2) Mack - Cali quarterly supplements;

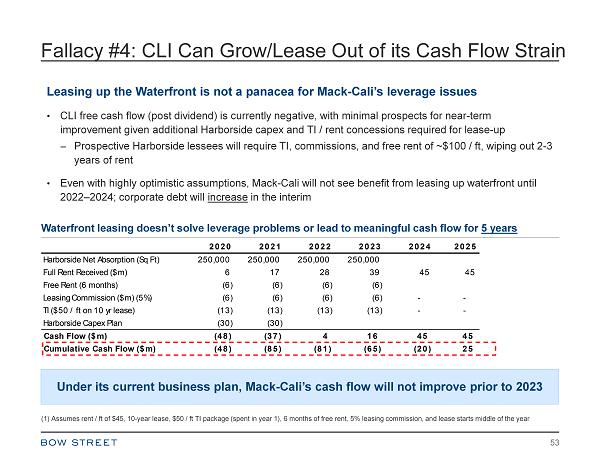

Fallacy #4: CLI Can Grow/Lease Out of its Cash Flow Strain 53 (1) Assumes rent / ft of $45, 10 - year lease, $50 / ft TI package (spent in year 1), 6 months of free rent, 5% leasing commission , and lease starts middle of the year Leasing up the Waterfront is not a panacea for Mack - Cali’s leverage issues • CLI free cash flow (post dividend) is currently negative, with minimal prospects for near - term improvement given additional Harborside capex and TI / rent concessions required for lease - up – Prospective Harborside lessees will require TI, commissions, and free rent of ~$100 / ft, wiping out 2 - 3 years of rent • Even with highly optimistic assumptions, Mack - Cali will not see benefit from leasing up waterfront until 2022 – 2024; corporate debt will increase in the interim Under its current business plan, Mack - Cali’s cash flow will not improve prior to 2023 Waterfront leasing doesn’t solve leverage problems or lead to meaningful cash flow for 5 years 2020 2021 2022 2023 2024 2025 Harborside Net Absorption (Sq Ft) 250,000 250,000 250,000 250,000 Full Rent Received ($m) 6 17 28 39 45 45 Free Rent (6 months) (6) (6) (6) (6) Leasing Commission ($m) (5%) (6) (6) (6) (6) - - TI ($50 / ft on 10 yr lease) (13) (13) (13) (13) - - Harborside Capex Plan (30) (30) Cash Flow ($m) (48) (37) 4 16 45 45 Cumulative Cash Flow ($m) (48) (85) (81) (65) (20) 25

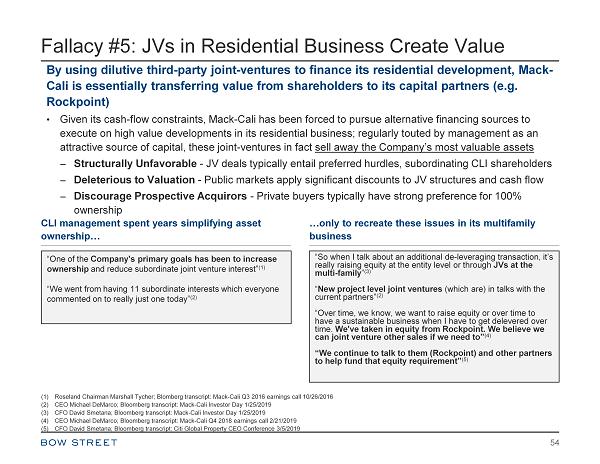

Fallacy #5: JVs in Residential Business Create Value 54 By using dilutive third - party joint - ventures to finance its residential development, Mack - Cali is essentially transferring value from shareholders to its capital partners (e.g. Rockpoint ) • Given its cash - flow constraints, Mack - Cali has been forced to pursue alternative financing sources to execute on high value developments in its residential business; regularly touted by management as an attractive source of capital, these joint - ventures in fact sell away the Company’s most valuable assets – Structurally Unfavorable - JV deals typically entail preferred hurdles, subordinating CLI shareholders – Deleterious to Valuation - Public markets apply significant discounts to JV structures and cash flow – Discourage Prospective Acquirors - Private buyers typically have strong preference for 100% ownership “One of the Company's primary goals has been to increase ownership and reduce subordinate joint venture interest” (1) “We went from having 11 subordinate interests which everyone commented on to really just one today” (2) “So when I talk about an additional de - leveraging transaction, it’s really raising equity at the entity level or through JVs at the multi - family ” (3) “ New project level joint ventures (which are) in talks with the current partners” (2) “Over time, we know, we want to raise equity or over time to have a sustainable business when I have to get delevered over time. We've taken in equity from Rockpoint. We believe we can joint venture other sales if we need to” (4) “We continue to talk to them (Rockpoint) and other partners to help fund that equity requirement” (5) CLI management spent years simplifying asset ownership… …only to recreate these issues in its multifamily business (1) Roseland Chairman Marshall Tycher ; Blomberg transcript: Mack - Cali Q3 2016 earnings call 10/26/2016 (2) CEO Michael DeMarco; Bloomberg transcript: Mack - Cali Investor Day 1/25/2019 (3) CFO David Smetana; Bloomberg transcript: Mack - Cali Investor Day 1/25/2019 (4) CEO Michael DeMarco; Bloomberg transcript: Mack - Cali Q4 2018 earnings call 2/21/2019 (5) CFO David Smetana; Bloomberg transcript: Citi Global Property CEO Conference 3/5/2019

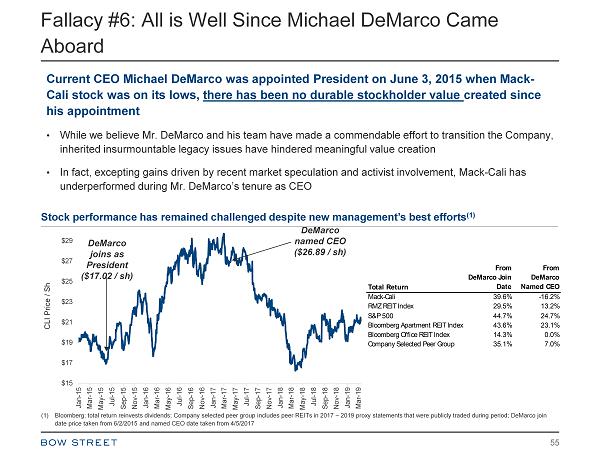

Fallacy #6: All is Well Since Michael DeMarco Came Aboard 55 Current CEO Michael DeMarco was appointed President on June 3, 2015 when Mack - Cali stock was on its lows, there has been no durable stockholder value created since his appointment • While we believe Mr. DeMarco and his team have made a commendable effort to transition the Company, inherited insurmountable legacy issues have hindered meaningful value creation • In fact, excepting gains driven by recent market speculation and activist involvement, Mack - Cali has underperformed during Mr. DeMarco’s tenure as CEO $15 $17 $19 $21 $23 $25 $27 $29 Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17 Sep-17 Nov-17 Jan-18 Mar-18 May-18 Jul-18 Sep-18 Nov-18 Jan-19 Mar-19 CLI Price / Sh DeMarco joins as President ($17.02 / sh ) DeMarco named CEO ($26.89 / sh ) Stock performance has remained challenged despite new management’s best efforts (1) Total Return From DeMarco Join Date From DeMarco Named CEO Mack-Cali 39.6% -16.2% RMZ REIT Index 29.5% 13.2% S&P 500 44.7% 24.7% Bloomberg Apartment REIT Index 43.6% 23.1% Bloomberg Office REIT Index 14.3% 0.0% Company Selected Peer Group 35.1% 7.0% (1) Bloomberg; total return reinvests dividends; Company selected peer group includes peer REITs in 2017 – 2019 proxy statements tha t were publicly traded during period; DeMarco join date price taken from 6/2/2015 and named CEO date taken from 4/5/2017

A New Day at Mack - Cali: the Path Forward 56

Now is the Time For New Board Leadership 57 The 4 Directors Bow Street seeks to replace have combined tenure of over 80 years • Mack - Cali’s long serving Board has overseen massive destruction of shareholder value over the last 15 years; 7 of 11 directors from this period remain on the Board (including two members of the Mack family) • Deep entrenchment and loyalty to Chairman William Mack has left the Board lacking the independence required to make the difficult decisions Mack Cali faces at this time • The four directors Bow Street has nominated are accomplished business leaders from different fields and practices; each will bring a unique, truly independent perspective, and all will be fierce advocates for all CLI shareholders • We have chosen each of these directors to fill specific needs within CLI’s current Board. Their relevant expertise includes board governance, shareholder governance, real estate operations and investment, Manhattan - adjacent real estate development, consumer branding/marketing, and public company executive experience • We have endeavored to add diversity to the Board with respect to gender, age and most importantly – independence A new day at Mack - Cali must begin at the very top – new oversight is needed to assure the Company’s future

Bow Street Open to Settlement, Not “Window Dressing” 58 On May 13 th , 2019 Bow Street initiated what we believed to be a constructive dialogue with Mack - Cali’s Chairman; he abruptly terminated these discussions on May 17, 2019 • Over two days of discussions Bow Street and Mack - Cali agreed to the following: – The es tablishment of a Strategic Review Committee of the Board, comprised of two Bow Street nominees and two Mack - Cali incumbent directors, with a mandate to review the Company’s strategic direction and explore the value to be realized from a sale of the Company or any of its assets. • These discussions were abruptly terminated by Mr. Mack, apparently over our inclusion of following terms, all of which we believe to be favorable for shareholders: a) Bow Street and Mack - Cali agreeing in advance to the directors comprising Strategic Committee; b) Enabling the Strategic Review Committee to engage an investment bank instead of a valuation firm, which we believe would be better positioned to determine the value expected to be received in a strategic transaction and compare it to the Company’s stand - alone prospects c) In the event that Mack - Cali receives any unsolicited proposals, providing the Special Review Committee with a mandate to review such proposals • Unfortunately, this Board’s true interest is in “window dressing” – an illusory process that perpetuates the status quo - rather than a legitimate value - creative outcome for shareholders Bow Street would support a settlement which establishes a Strategic Review Committee with the independence and mandate to determine the best path forward for Mack - Cali and its shareholders

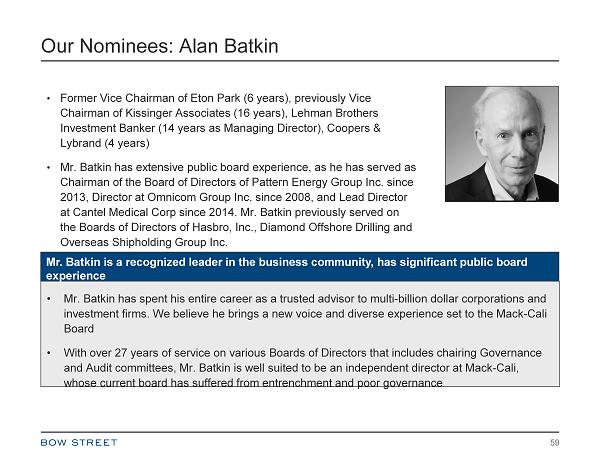

Our Nominees: Alan Batkin 59 • Former Vice Chairman of Eton Park (6 years), previously Vice Chairman of Kissinger Associates (16 years), Lehman Brothers Investment Banker (14 years as Managing Director), Coopers & Lybrand (4 years) • Mr. Batkin has extensive public board experience, as he has served as Chairman of the Board of Directors of Pattern Energy Group Inc. since 2013, Director at Omnicom Group Inc. since 2008, and Lead Director at Cantel Medical Corp since 2014. Mr. Batkin previously served on the Boards of Directors of Hasbro, Inc., Diamond Offshore Drilling and Overseas Shipholding Group Inc. • Mr. Batkin has spent his entire career as a trusted advisor to multi - billion dollar corporations and investment firms. We believe he brings a new voice and diverse experience set to the Mack - Cali Board • With over 27 years of service on various Boards of Directors that includes chairing Governance and Audit committees, Mr. Batkin is well suited to be an independent director at Mack - Cali, whose current board has suffered from entrenchment and poor governance Mr. Batkin is a recognized leader in the business community, has significant public board experience

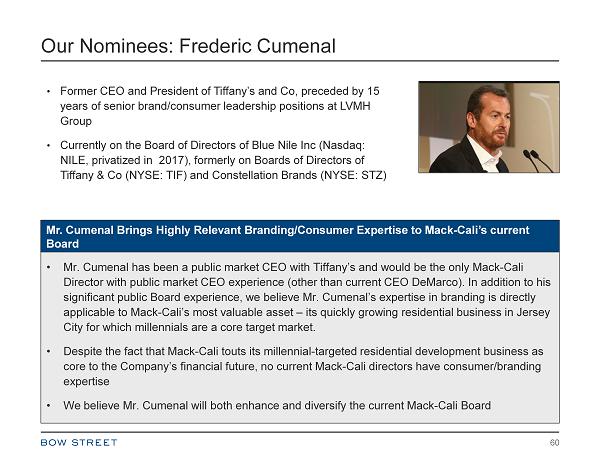

Our Nominees: Frederic Cumenal 60 • Former CEO and President of Tiffany’s and Co, preceded by 15 years of senior brand/consumer leadership positions at LVMH Group • Currently on the Board of Directors of Blue Nile Inc (Nasdaq: NILE, privatized in 2017), formerly on Boards of Directors of Tiffany & Co (NYSE: TIF) and Constellation Brands (NYSE: STZ) • Mr. Cumenal has been a public market CEO with Tiffany’s and would be the only Mack - Cali Director with public market CEO experience (other than current CEO DeMarco). In addition to his significant public Board experience, we believe Mr. Cumenal’s expertise in branding is directly applicable to Mack - Cali’s most valuable asset – its quickly growing residential business in Jersey City for which millennials are a core target market. • Despite the fact that Mack - Cali touts its millennial - targeted residential development business as core to the Company’s financial future, no current Mack - Cali directors have consumer/branding expertise • We believe Mr. Cumenal will both enhance and diversify the current Mack - Cali Board Mr. Cumenal Brings Highly Relevant Branding/Consumer Expertise to Mack - Cali’s current Board

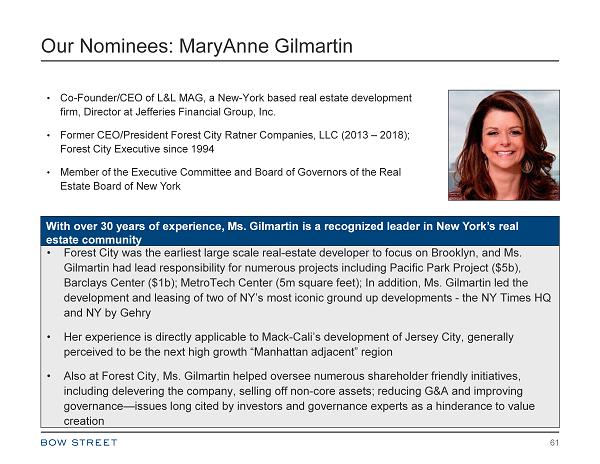

Our Nominees: MaryAnne Gilmartin 61 • Co - Founder/CEO of L&L MAG, a New - York based real estate development firm, Director at Jefferies Financial Group, Inc. • Former CEO/President Forest City Ratner Companies, LLC (2013 – 2018); Forest City Executive since 1994 • Member of the Executive Committee and Board of Governors of the Real Estate Board of New York • Forest City was the earliest large scale real - estate developer to focus on Brooklyn, and Ms. Gilmartin had lead responsibility for numerous projects including Pacific Park Project ($5b), Barclays Center ($1b); MetroTech Center (5m square feet); In addition, Ms. Gilmartin led the development and leasing of two of NY’s most iconic ground up developments - the NY Times HQ and NY by Gehry • Her experience is directly applicable to Mack - Cali’s development of Jersey City, generally perceived to be the next high growth “Manhattan adjacent” region • Also at Forest City, Ms. Gilmartin helped oversee numerous shareholder friendly initiatives, including delevering the company, selling off non - core assets; reducing G&A and improving governance — issues long cited by investors and governance experts as a hinderance to value creation With over 30 years of experience, Ms. Gilmartin is a recognized leader in New York’s real estate community

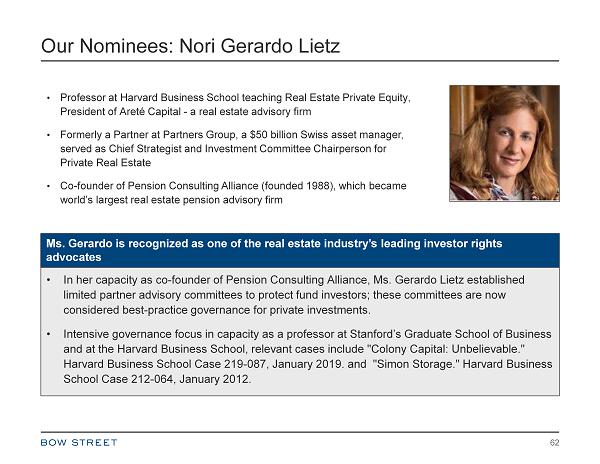

Our Nominees: Nori Gerardo Lietz 62 • Professor at Harvard Business School teaching Real Estate Private Equity, President of Areté Capital - a real estate advisory firm • Formerly a Partner at Partners Group, a $50 billion Swiss asset manager, served as Chief Strategist and Investment Committee Chairperson for Private Real Estate • Co - founder of Pension Consulting Alliance (founded 1988), which became world’s largest real estate pension advisory firm • In her capacity as co - founder of Pension Consulting Alliance, Ms. Gerardo Lietz established limited partner advisory committees to protect fund investors; these committees are now considered best - practice governance for private investments. • Intensive governance focus in capacity as a professor at Stanford’s Graduate School of Business and at the Harvard Business School, relevant cases include "Colony Capital: Unbelievable." Harvard Business School Case 219 - 087, January 2019. and "Simon Storage." Harvard Business School Case 212 - 064, January 2012. Ms. Gerardo is recognized as one of the real estate industry’s leading investor rights advocates

Shareholders Have a Clear Choice to Make 63 • Newly constituted independent Board of Directors, mandated to create value for all shareholders • Focus on meaningful solutions that address the Company’s structural issues – its leverage and cash flow needs • A commitment to explore all strategic alternatives to maximize shareholder value including a potential sale of the Company and its assets • Another 15 years of continued underperformance and value destruction • Weak governance and unmitigated conflicts • Prospective dilutive equity issuance and/or dividend cut • More “window dressing” – illusory solutions with limited/no impact Bow Street urges shareholders to protect their investment and vote the GOLD proxy card FOR its four, highly - qualified nominees who bring diverse, relevant backgrounds to a Board in need of change. A New Day At Mack - Cali The Status Quo